EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Trending

-

Advancing Canada’s defence innovation

09 Apr 2026 -

Canadian Insurance Outlook 2026: navigating uncertainty, unlocking opportunity

13 Mar 2026 Financial services -

From bottleneck to accelerator: the strategic role of digital identity controls for industrials and energy companies

18 Feb 2026 Energy and resources

Discover cash management's digital evolution, emphasizing client needs and operational efficiency for modern banking success.

In brief:

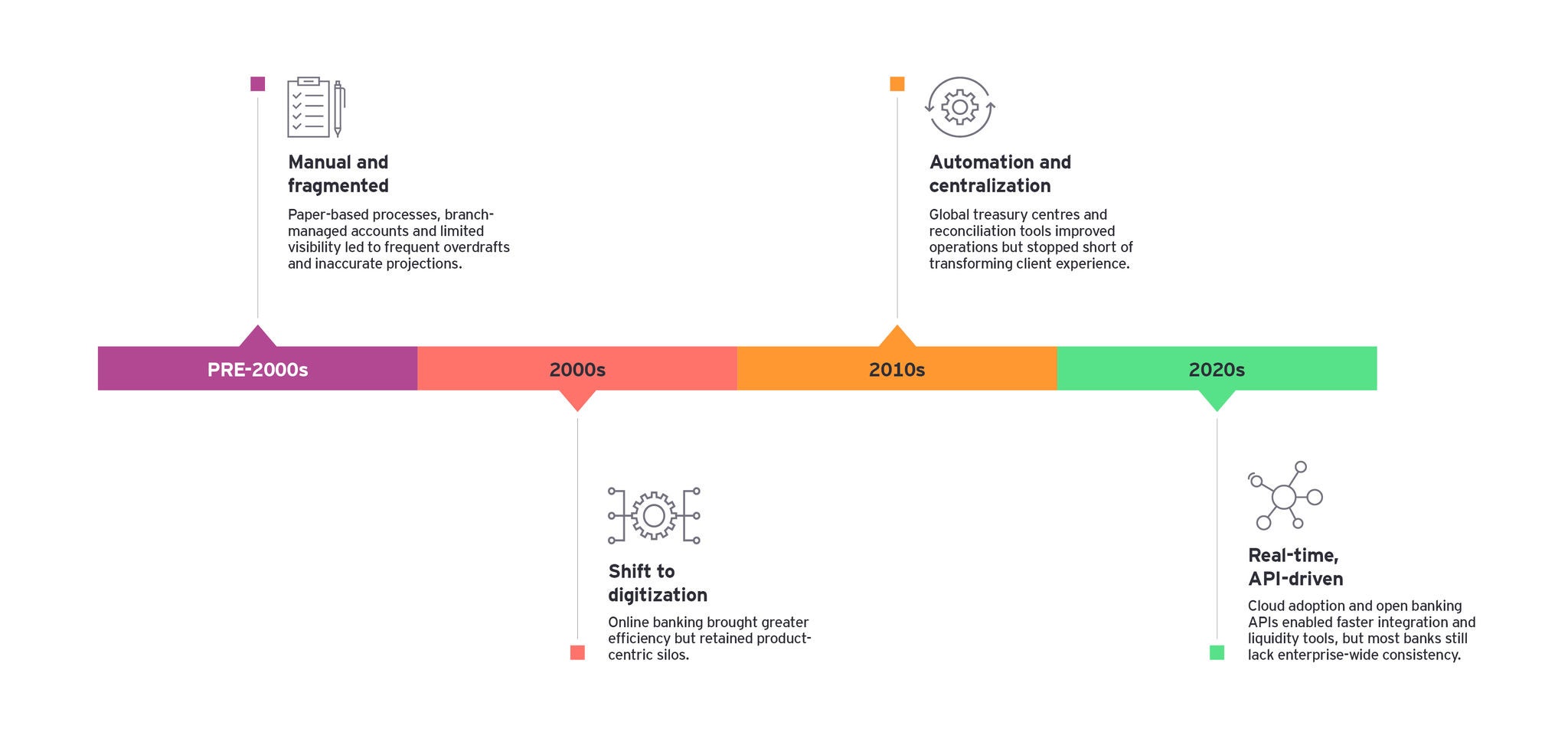

- Cash management has evolved over the past two decades from manual, paper-based processes to digitized platforms and global treasury models.

- Banks need to rethink their cash management structures to meet modern client demands.

- Banks should focus on modernizing their core offerings, segmenting by client needs, rewiring for scale and resilience, strategically managing data and embedding compliance from day one.

Over the past two decades, cash management has moved from paper- and branch-based operations to digitized platforms and global treasury models. Yet many institutions still operate on fragmented systems, outdated delivery models and reactive compliance approaches, all of which fall short of what today’s clients demand.

Commercial and corporate clients now expect real-time control, tailored services and seamless digital experiences. To respond, banks must go beyond system upgrades and fundamentally rethink how cash management is structured, delivered and monetized.

What’s next: key strategic calls to action

- Launch high-impact MVPs: Focus delivery on fast-to-market solutions like real-time liquidity dashboards, onboarding APIs or digital servicing tools that address clients’ immediate pain points.

- Design for reuse, not one-off: Prioritize foundational components — such as pricing engines, data models and compliance workflows — that can scale across markets and product lines.

- Tailor the offering, not just the interface: Move from generic platforms to modular, segment-specific solutions built around the needs of mid-market, multinational or verticalized clients.

- Shift compliance upstream: Integrate risk, legal and regulatory design into the product development lifecycle — reducing delivery delays and enhancing audit readiness.

- Restructure operating teams around delivery speed

- Break down traditional silos: Form cross-functional squads that bring together product, data, tech and risk with clear ownership and velocity targets.

How we got here: the evolution of cash management

EY’s experience shows that modern cash management isn’t just a technology upgrade, it’s a business strategy. Banks that win lead with client value, act with urgency and scale with precision.

Building the right foundation for cash management transformation

Before banks can unlock growth, they must modernize the foundation — rethinking how core offerings are delivered, how client needs are served and how internal capabilities scale with demand.

What clients expect today

Commercial and corporate clients are no longer satisfied with generic treasury tools. They demand outcomes — not just services — delivered with speed, precision and relevance.

- A CFO expects real-time dashboards, not next-day static reports.

- A tech client wants tiered pricing based on service usage and transaction volume.

- A global treasury team needs liquidity pooling across regions, not manual workarounds.

These needs require banks to shift from product-centric to outcome-led design.

From friction to foundation: where banks must focus first

To compete in today’s cash management landscape, banks can’t just digitize — they must modernize with intent. That starts by addressing three structural shifts:

- Outdated product platforms

- Misaligned segment strategies

- Inefficient operations.

Each shift poses real business risks — but opens the door to measurable impact when fixed right.

Drawing from our recent work with major Canadian and global financial institutions, we’ve gleaned insights across five key areas, providing executives with a perspective on the common challenges encountered during the implementation of large-scale cash management transformation programs.

1

Balance ambition with delivery realities. Speedy deployments help banks test, learn and generate revenue

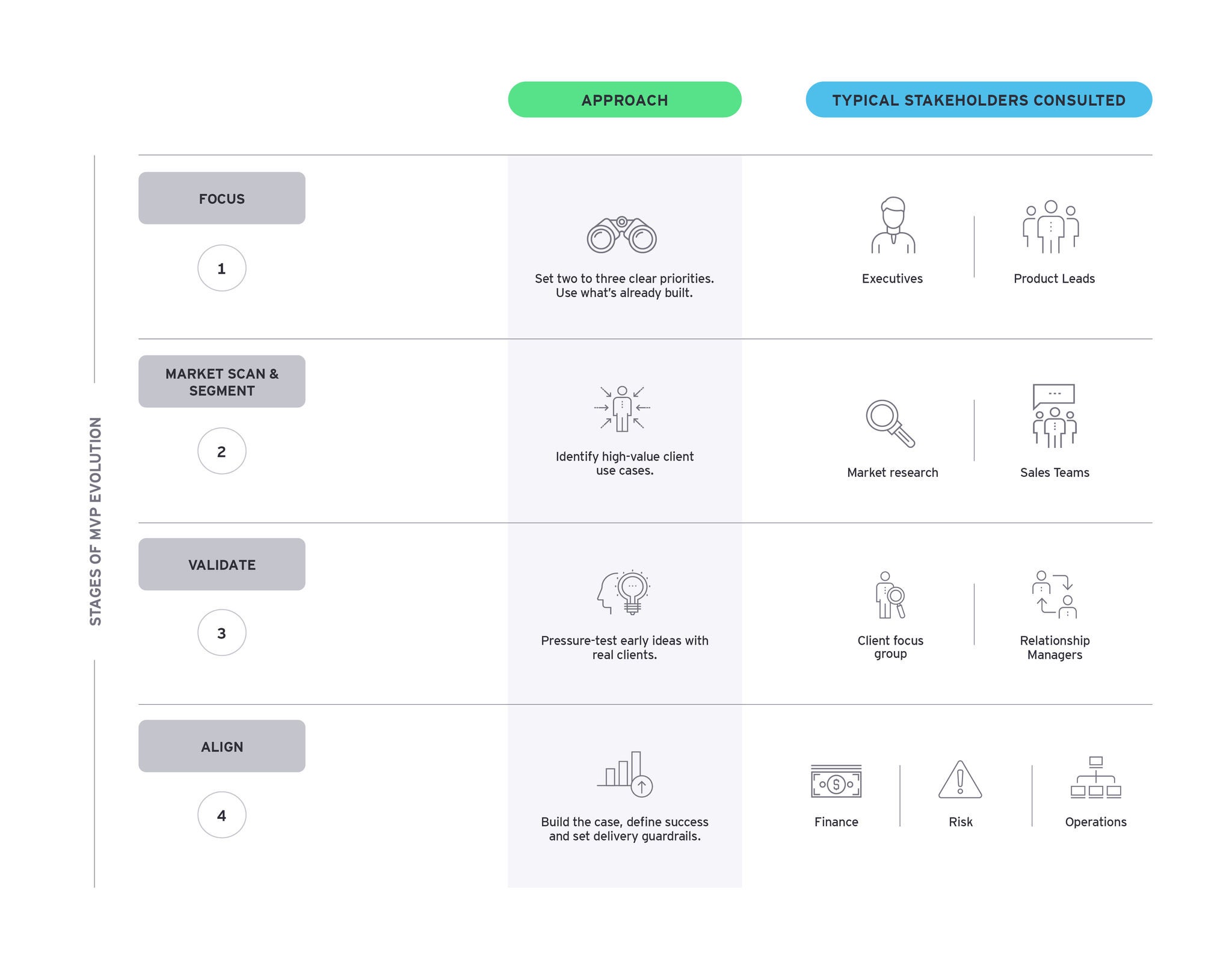

Successful transformations don’t begin with full-scale builds: they start with MVPs. Well-executed programs focus on a few high-impact features, reuse existing capabilities and go to market fast. This creates early momentum, unlocks client feedback and reduces delivery risk.

Leading banks use assets already in place — like pricing engines, liquidity dashboards or onboarding APIs. These are bundled into focused MVPs, such as a self-service portal for SMEs or automated cash sweeps for commercial clients. Early wins like these prove value and set the stage for broader rollout.

Too often, MVPs are built in isolation by product or tech teams without input from sales, service or clients. This typically leads to good technology that sometimes misses the market.

Example MVP development approach

Any change to an offering should be revalidated with the client and industry teams to check that it’s commercially viable.

Recommended actions:

- Identify core features for the MVP: Define the key outcomes and essential features that will deliver the value quickly without adding complexity.

- Establish a shared vision early: Define a clear program vision with product, commercial and operations teams to shape a common goal. Prioritize reusing existing capabilities to reduce build time and risk.

- Test fast, learn faster: Adopt a phased MVP. Launch quickly, gather feedback from real users and refine through iterative short cycles to ensure relevance and adoption.

2

Spend time to lay a sustainable foundation for transformation

Not every capability needs to be reimagined from day 1. The most effective programs identify a narrow set of changes that truly matter at launch — and defer the rest. This avoids unnecessary build, reduces delivery risk and accelerates outcomes.

In our experience, banks that prioritize critical features early reduce delivery risks and accelerate program timelines. Programs that skip this step typically struggle with unclear priorities, missed deadlines and bloated MVPs.

Recommended actions:

Put two key controls in place:

- Conduct a rapid impact assessment (2–3 weeks): Time-box a focused review before the MVP build begins. Work cross-functionally (product, ops, tech, risk) to isolate:

- What must change to support day 1 use cases.

- What can be deferred to post-launch without client impact.

- Use client journeys and system maps to trace dependencies.

- Example: A bank EY supported to launch a liquidity suite flagged onboarding flows and balance consolidation as day 1 critical — but deferred pricing flexibility and advanced analytics to Phase 2.

- Establish clear prioritization rules Define a simple, shared decision rule:

- Must do: If a rule isn’t included, launch can be blocked or the client experience breaks.

- Can wait: Valuable, but doesn’t stop day 1 operations

- Document this early and align all stakeholders — especially Risk, Finance and frontline teams.

- Example: A global bank EY helped with its cash management program tagged around 20% features from original scope as “business debt,” enabling it to launch three months earlier than planned.

3

A 360-client view is vital for managing complex hierarchies and segmentation in multinational corporate clients

Corporate and commercial clients often operate across several legal entities and business units, each with its own account role, ownership structure and regulatory requirements. These complexities directly affect operational client billings, regulatory reporting, and how products are priced and serviced.

We find that most banks rely on multiple systems spread across the organization to capture this information often

To enhance customer interactions and streamline operations, a unified cross-channel view is now essential. A complete view of the client across the full relationship is required to reduce friction in operations such as onboarding, billing or compliance.

Recommended actions:

- Define clear client segments and industry verticals: Establish a consistent segmentation framework based on client size, complexity and industry (e.g., commercial banking vs. corporate banking, health care vs. real estate). This allows for tailored product design, pricing and coverage models.

- Example: In our experience, banks that introduce segmentation in treasury, thereby enabling specialized product bundles, achieve stronger client retention and cross-sell performance.

- Equip Relationship Managers with a complete view: Provide front-line teams with a unified relationship view — including linked entities, product holdings and service history — to improve responsiveness and unlock cross-sell.

- Example: A commercial bank enabled Relationship Managers to access full relationship maps, surfacing increase in upsell opportunities across shared clients.

- Simplify client processes across the lifecycle: Redesign onboarding, servicing and reporting around the full client relationship — not isolated accounts — to reduce duplication and friction.

- Example: In our experience, banks that eliminated redundant document requests across linked subsidiaries reduced onboarding time.

4

Manage data as a strategic asset through clear ownership of data domains across business

Clear ownership, shared standards and smarter use of data unlock efficiency and reduce risk.

Within most banks, data is scattered across business lines, systems and geographies, with limited governance and inconsistent definitions. This makes it difficult to deliver consistent client experiences, support growth and meet regulatory expectations.

Data requirements also vary widely across functions. A simple data point like “account balance” can mean different things to lending, cash forecasting and treasury teams. Without shared definitions and ownership, banks end up duplicating work, building one-off fixes and accumulating technical debt.

Take KYC and AML, for example. These are often managed in separate teams. But when they’re shared, KYC data can help AML teams build smarter fraud rules. If a client’s geographic footprint is known at onboarding, that same data can be used to avoid false-positive flags during transaction monitoring across multiple jurisdictions.

Without this link, the bank treats each function in isolation, slowing service, increasing compliance cost and frustrating clients.

Recommended actions:

- Assign clear data ownership by domain: Establish business owners for key data domains (e.g., client, account, transaction) with responsibility for defining, stewarding and updating attributes.

- Example: A global bank EY worked with streamlined onboarding by assigning ownership of client onboarding data to the commercial operations team.

- Create a common language across functions: Standardize fields, enrichment logic and usage rules so the same data works across multiple business areas.

- Example: By aligning balance definitions across lending, forecasting and payments, a bank eliminated multiple duplicate reports and significantly reduced reconciliation time.

- Example: One global bank used KYC data from onboarding to improve AML rule precision for multi-country clients, significantly reducing false positives.

This isn’t just about fixing systems: it’s about making data work harder for the business. When data is owned, standardized and reused, it becomes an accelerator and not a blocker for transformation.

5

Evolving product base triggers new applicable regulations, requiring recalibration of the compliance operating model

As offerings evolve, compliance must keep pace so it doesn’t have to catch up later.

Each new cash management product — whether a real-time payment rail, virtual account or liquidity tool — brings new regulatory obligations. Without early alignment, banks risk launch delays, audit findings and client trust erosion.

We’ve seen institutions push innovative products to market, only to face roadblocks when known findings resurface or new requirements weren’t anticipated early enough.

Compliance must be embedded in the product lifecycle, not retrofitted after development.

For example, EY supported the rollout of a cross-border payment platform that required re-review of KYC and AML obligations across multiple jurisdictions. When these were assessed upfront, the bank avoided rework, launched months faster and reduced onboarding friction for clients with global footprints.

Recommended actions:

- Embed compliance from day 1: Involve Legal and Compliance teams in product design, using a predefined regulatory inventory to identify potential issues early.

- Example: A Tier 1 bank used EY’s Cash Management LRR Inventory to screen 15 regulations during the design phase of a new escrow product — avoiding rework post-launch.

- Modernize the compliance operating model: Strengthen coordination between compliance and product teams. Invest in shared tools, automated controls and governance forums that scale with innovation.

- Example: One bank embedded compliance checkpoints into agile delivery sprints, cutting issue resolution time by almost half.

- Prioritize known regulatory findings: Resolve high-risk audit items before launching new offerings — especially those tied to onboarding, reporting or client data.

- Example: EY supported a global bank that paused a liquidity rollout to close open findings from a prior KYC audit, enabling regulator signoff without impacting market reputation.

By treating compliance as an enabler and not a barrier, banks reduce regulatory risk, protect timelines and build trust with both clients and regulators.

Conclusion

As the cash management landscape transforms, five key insights emerge for institutions seeking to lead:

- The strategic opportunity is now: Cash management is no longer a back-office function. It’s a growth lever. Institutions that modernize now will unlock new revenue, deepen client relationships and build operational resilience in volatile markets.

- Client expectations have shifted — permanently: Clients want tailored, real-time and always-on capabilities — not generic products. Banks must deliver control, transparency and relevance across every segment they serve.

- Foundations must be rebuilt for scale: Success starts with replatforming core offerings — deposits, liquidity, payments, fraud, analytics — and delivering them through modular, cloud-native infrastructure with embedded controls and APIs.

- Change must be client-led and outcome oriented: Banks must move from launching products to solving problems:

- Design MVPs to meet urgent client needs in four to six months.

- Tailor offerings by industry or business tier.

- Streamline servicing through embedded, self-service experiences.

- Transformation requires a coordinated operating model: Speed, compliance and scale are only possible when product, tech, data and risk are aligned. Institutions must establish centralized data models, define clear client segments and embed regulatory readiness upfront.

The path forward is not to do everything — it’s to focus on the right things, faster.

Our experience shows that cash management transformation is not just about modernization — it’s about precision, relevance and speed to value. Institutions that lead will redefine how they serve clients and how they grow.

Summary

Over the last two decades, cash management has transitioned from manual processes to advanced digital platforms. Banks must adapt their structures to align with modern client expectations for real-time, tailored services. Key strategies include launching impactful MVPs, designing reusable components, and prioritizing compliance from development stages. Additionally, banks should focus on understanding client needs through segmentation and streamlining operations by breaking down silos. A unified data approach is essential to enhance operational efficiency and compliance. Successful transformation hinges on building resilient frameworks centred on client value, operational speed, and regulatory alignment to drive growth and enhance client relationships.