EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Trending

-

Advancing Canada’s defence innovation

09 Apr 2026 -

Canadian Insurance Outlook 2026: navigating uncertainty, unlocking opportunity

13 Mar 2026 Financial services -

From bottleneck to accelerator: the strategic role of digital identity controls for industrials and energy companies

18 Feb 2026 Energy and resources

Co-authors : Oksana Chikina - Partner, Climate Change and Sustainability Services

Debbie Baxter - Senior Advisor, Transaction Real Estate

In brief

- Public sector organizations are expected to optimize costs and derive greater value and efficiency from their corporate real property portfolios.

- Taking a holistic approach at both the portfolio and individual building levels helps governments optimize footprint, reduce operating costs and achieve ESG targets. It also increases employee engagement and positively impacts many other interconnected government policy priorities.

How are challenges converging for corporate real property in Canada?

Managing large real property portfolios demands specific capabilities as well as rigorous and continuous oversight.

Historically, in the private sector, operational inefficiencies in buildings or portfolios were absorbed by a growing market, a shortage of general real property shortage and relatively newly built assets, which did not require high deferred maintenance and reconstruction costs.

Corporate real property portfolio management inefficiencies started to be recognized in the past 10 to 15 years, and have become even more acute in the last three years. We see this emphasized in the post-COVID impact of higher vacancy levels, growing budget constraints due to a slower economy, and evolving pressure to set and deliver on environmental, social and governance (ESG) goals.

Since corporate real property was not historically a strategic priority for most companies, teams that oversaw real property portfolios were usually formed as a supporting, reactive function. They tended to lack the required capabilities, bandwidth capacity and experience to reassess efficiencies and alignment of current ownership or lease structures to the business strategy. Reliable and consistent building operations data needed to make well-informed strategic decisions was also in short supply.

This lack of insights to make real property decisions is especially pronounced in the public sector. Here, organizations typically own most of their assets and have not revisited portfolios for decades. They are often critically less funded and less inclined to adopt risk from innovative real property practices.

This tension is compounded by aging infrastructure and continuous budget constraints. For example, many government-owned buildings are heritage assets and are nearly a century old. They require renovation and high-cost retrofits of outdated heating and electrical systems. That’s in addition to the increasing costs associated with deferred maintenance from labour shortages and supply chain constraints.

What’s more: real property is not immune to the broader trends reshaping all Canadian industries. Calgary and Montréal, for example, are aiming to become carbon neutral by 2050, while Vancouver and Toronto have more stringent ambitions to become net zero by the same date.

These objectives are challenged by the high cost of retrofitting existing buildings with green technologies. Regulations — such as New York City’s Local Law 97 — are beginning to impose strict carbon emission limits on buildings.

This leaves many public sector properties facing compliance challenges and potential fines. For example, Vancouver is the first Canadian municipality to impose an emissions limit for large, existing commercial buildings, with hefty fines coming into effect in 2026.1

We have seen that leading organizations across Canada’s public sector are realizing that real property management should transform. The tone is set from the top, with the federal government reviewing real property portfolios with the goal of finding surplus properties that are well suited to transform into affordable housing units.

But more work must be done on all fronts: from strategic reviews to operational data reliability. Segregated property management systems in many — if not most — government buildings are generating unreliable and inconsistent data, which makes it difficult to track and optimize operational costs.

EY teams recommend taking a holistic approach that links two crucial steps at the portfolio and then individual building level which, if executed properly and together, can help save up to 15% to 20% of real property operations cost, and free up additional funds from portfolio restructuring.

What does this include?

- Carry out an objective maturity assessment evaluating both the portfolio and real property function.

- Make the most of emerging technologies to improve operational efficiency.

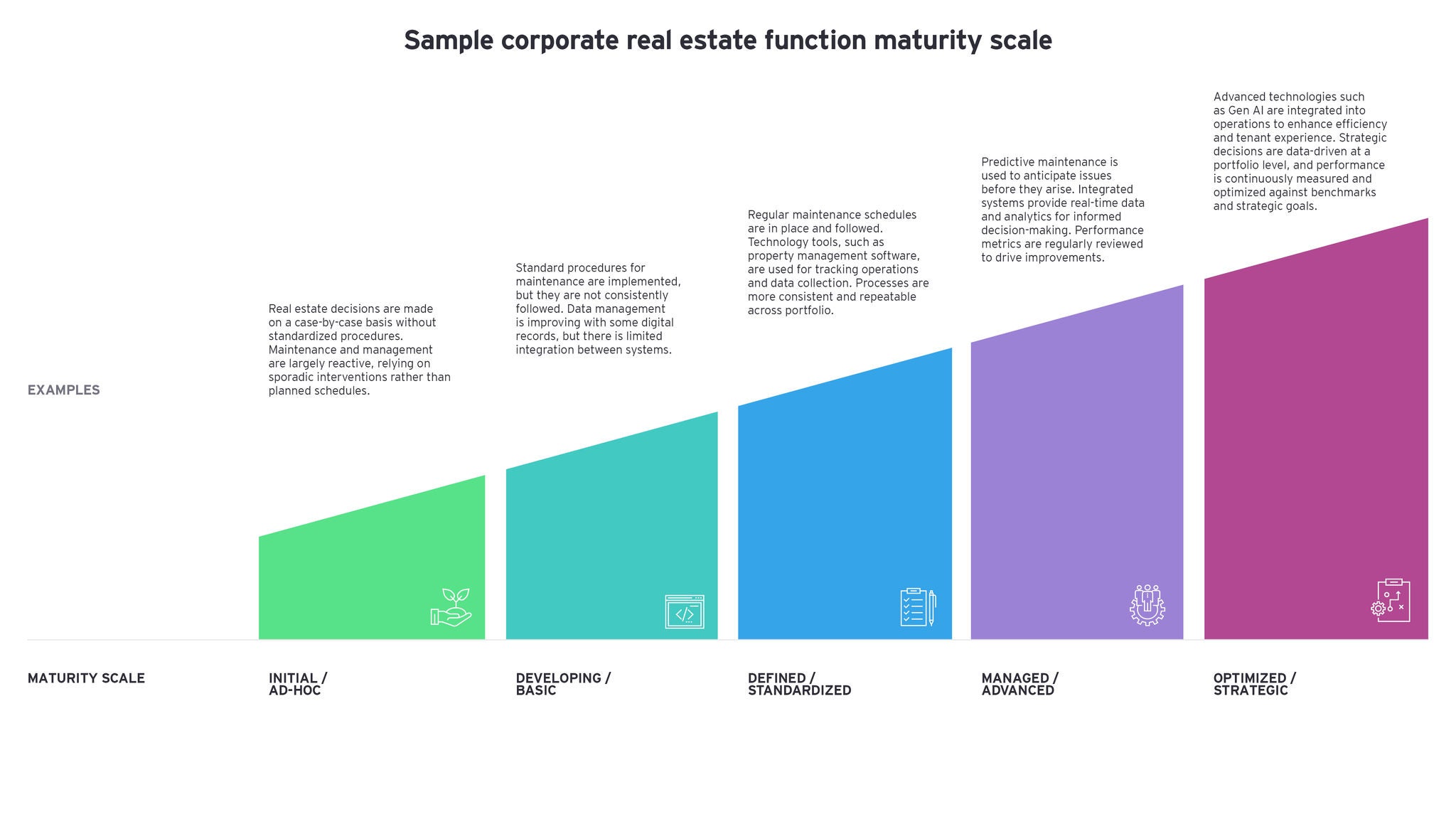

Step 1: Carry out an objective maturity assessment evaluating both the portfolio and real property function

Assessing the current maturity stage of your real property requires an unbiased view of both the operating real property function, including efficiency and capability maturity, and real property inventory as well as its correlation with organizational needs, requirements and historical KPIs.

You need both perspectives to properly inform an effective real property strategy. In the market, we see this work best when both analyses run concurrently, informing each other. This helps avoid a situation in which the real property function is not well equipped to support the strategy.

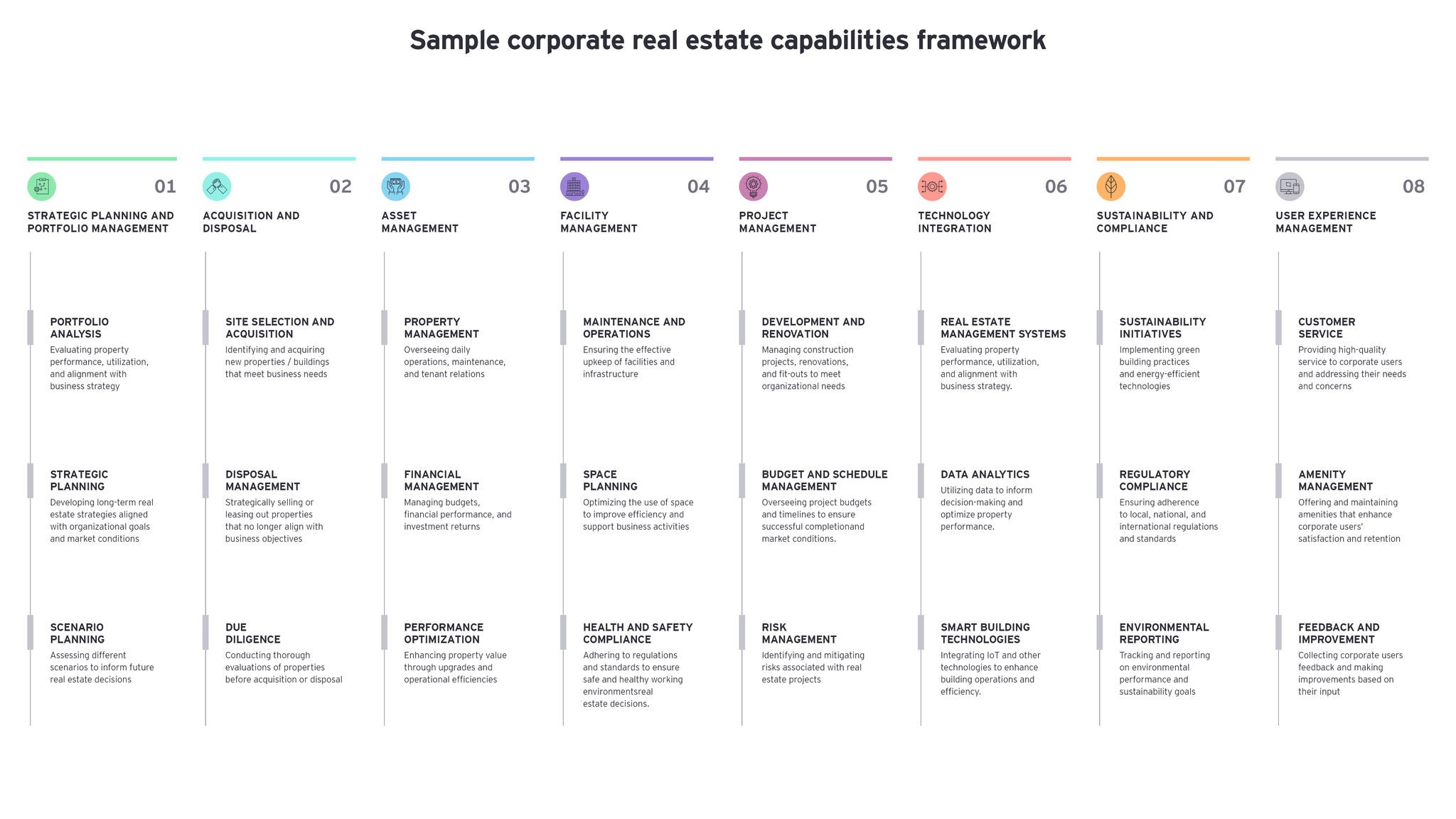

This is a complex task. But a systemic approach can help. We use the EY Real Property Function Capability Framework and Maturity Scale as a starting point to assess the current state. The best way to land on the desired future state is through collaborative workshops with cross-functional teams — not only real property operations, but other functions like technology, HR, accounting and others that interact with real property — where all participants collectively form their view on the desired target state maturity level.

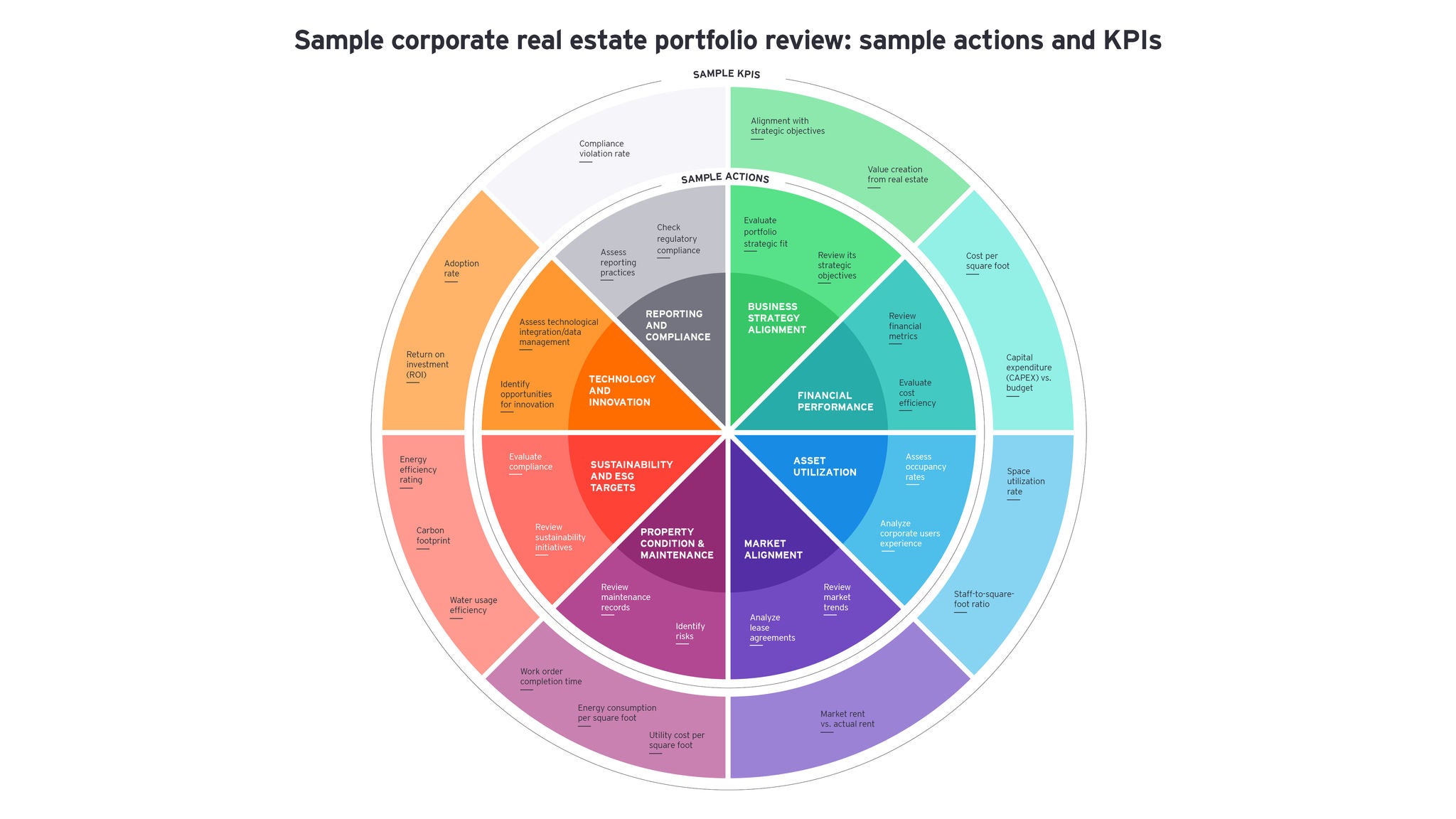

For the real property portfolio, leading practices suggest curating a KPI list that reflects key strategic organizational priorities and how they’re mirrored and supported by the real property. As a starting point you may want to tap into the list of KPIs that helps you assess your real property portfolio performance and strategic alignment.

A maturity assessment evaluating both the real property portfolio and the real property function can provide a robust framework organizations can use to identify gaps between current and target future state, optimize asset ownership and performance, and drive long-term strategic value.

By assessing these two critical areas, businesses can unlock several key benefits:

1. Aligned strategy and execution: Evaluating both the portfolio and the function aligns the organization's real property assets and its broader business objectives. This clarity allows for more effective decision-making and enables real property strategies to directly support corporate goals.

2. Enhanced operational efficiency: A maturity assessment identifies inefficiencies in both the management of the portfolio and the function’s internal processes. By pinpointing areas for improvement, organizations can streamline operations, reduce costs and improve service delivery across the real property lifecycle.

3. Data-driven decision-making: Understanding the maturity of data collection and analytics capabilities in both the portfolio and the function enables organizations to glean insights for more informed, agile decision-making. This can result in better portfolio management, more accurate forecasting and improved responsiveness to policy changes.

4. ESG alignment and compliance: As sustainability and regulatory pressures increase, a maturity assessment helps organizations evaluate their real property function’s readiness to support environmental, social and governance (ESG) commitments, including the ability to meet existing obligations and their relevance in the current market environment. It highlights opportunities for retrofitting, energy efficiency improvements, and regulatory compliance.

5. Risk mitigation: A thorough maturity assessment can help organizations identify potential risks — whether from market volatility, regulatory shifts or operational inefficiencies. This proactive approach enables the development of mitigation strategies that protect the organization’s real property assets and financial performance.

6. Future-readiness: A comprehensive evaluation can equip organizations with the insights needed to futureproof their real property portfolio and function. Whether responding to market trends, technology advancements or evolving employee needs: the maturity assessment provides the roadmap to remain competitive and adaptable.

What’s the key takeaway?

A maturity assessment for both the real property portfolio and function not only provides actionable insights for operational improvement, it also positions organizations to strategically align real property with broader strategic priorities, enhance sustainability efforts and mitigate risks — ultimately driving long-term value and informing strategic decisions of asset dispositions or alternative use.

Step 2: Make the most of emerging technologies to improve operational efficiency

Once the corporate footprint strategy is sorted out and the footprint is optimized, the second opportunity for driving additional efficiencies lies at the individual asset level. The corporate real property market is going through a transformational change. Being pushed by evolving ESG standards and compliance requirements from one side, it’s also impacted by changing end users’ requirements for better spaces and extended amenities. That’s in addition to increasing public scrutiny around cost reduction.

Recent trends are reshaping expectations from real properties:

1. Employee and user experience requirements:

- Evolution of the workplace: This involves collaborative office spaces designed to support various working styles and hybrid work environments (e.g., the WeWork model).

- Premium amenities: These days there’s increasing demand for high-end amenities such as fitness centres, onsite childcare and gourmet dining to enhance employee satisfaction and attract top talent.

- Better wellbeing: Greater customization of lighting, temperature and occupancy improves tenant comfort and contributes to energy efficiency. EY teams talk a lot about our humans@centre philosophy. This comes down to the ability to empathize with your people by understanding their uniqueness through their lens, and then designing talent strategies, structures and policies with their specific needs in mind.

2. Operations efficiency requirements:

- Data-driven decision-making: Consistent and reliable data available in a real time and normalized across portfolios of assets and benchmarks empowers facility managers with a comprehensive view of building performance. Analytics further help identify inefficiencies, optimize energy usage and proactively address maintenance needs planning and resource allocation.

- Cost savings and sustainability: Adoption of intelligent property technologies allows for proactive facility management, which can lead to substantial savings. Furthermore, it aligns with ESG goals by reducing your organization’s environmental impact. As an example, intelligent building systems can dynamically adjust heating, ventilation and air conditioning (HVAC) based on occupancy, significantly reducing energy consumption.

- In-house teams vs. strategic third-party partnerships: There are two opposing trends in the market today:

- Mainstream: Outsourcing property management to professional facility management services firms to gain efficiencies at the portfolio level and optimize costs.

- Cutting edge: Corporate users aiming to achieve leading-class experiences in their buildings initially outsourced property management to third parties, but are now are bringing operations back in-house to enhance service quality, and further customization and control.

3. ESG

- Compliance: Growing concerns about greenwashing invite more attention to the performance of individual assets as contributors to corporate targets and goals.

- Climate resilience: In addition to specific disclosure requirements and progress against existing ESG ambitions and targets, a changing climate poses challenges for individual assets: increased duration and intensity of heatwaves, increased flood levels, and air quality issues driven by more frequent forest fires call for reassessment of climate resilience strategies at the individual asset level.

What do all these trends mean to corporate real property?

Property technology and reliable, consistent data availability are becoming a central pillar, enabling operational efficiency, better user experience and ESG compliance for the building. Extend that capability across an entire portfolio, and this amplifies facility managers’ ability to spot inefficiencies, optimize energy use and proactively address maintenance needs.

Intelligent building systems also provide a wealth of data to fuel trend analysis, performance benchmarking, scenario modelling, proactive planning and better resource allocation. All of this can help you make informed decisions, save on costs and reinforce sustainability.

But not every public sector organization is assessing opportunities for new technology adoption right now. Typically, there are three major barriers slowing down the decision:

- Lack of clarity on the real property portfolio’s current state and key KPIs (see above: Step 1: Carry out an objective maturity assessment evaluating both the portfolio and real property function).

- Bias that adopting new technology is very costly. It really depends on the technology and solution. For example, EY teams work with KODE Labs and their proven ROI-driven smart building platform. This enables the ability to integrate and visualize all available systems and data, to help with the understanding of the portfolio’s current state while also helping identify the gap to the desired state. This method has proven to be a cost-effective approach that uses the experience and skillsets of both organizations to deliver truly unique and quantifiable, value driven results.

- Fear that the organization will not follow the change. This is the most underestimated barrier. It’s important to ensure that once an organization adopts new technology, it’s supported by adequate processes and a functional operating model from day one (see above: Step 1: Carry out an objective maturity assessment evaluating both the portfolio and real property function). However, even once those are all set, change management becomes key in further driving the change and requires constant effort and focus from the respective teams.

“Employing a process and a platform that normalizes data across all systems and software is essential for achieving return on investment across an entire portfolio's technology and system stack. Many of the world's largest and most innovative organizations are our clients, and all have achieved ROI in under 12 months, unlocking additional savings to fund other valuable solutions," says Edi Demaj, Co-Founder of KODE Labs.

Whether it’s energy, operational, reporting, labour efficiencies or overall experience improvement for the people who occupy these portfolios, the EY organization and KODE Labs collaboration has proven to deliver results across all these areas. Once an organization wants to increase the value of its building operations, facility management and data quality, it should tailor the tech approach to specific operational goals and portfolio KPIs.

To get there, organizations should keep the following considerations in mind:

1. Clearly align organizational goals and service scope. That means evaluating the current state of your real property footprint and operational KPIs to identify improvement opportunities. From there, you’re ready to benchmark the organization against peers and leading practices. All of this can be used to develop a current-state operational overview that highlights quick wins and defines strategic goals.

2. Design an approach to implement and scale change. This action plan is where the rubber starts to meet the road. It’s all about putting guardrails for success in place. That includes identifying implementation support teams, as well as how you’ll customize analytical outputs, track progress and report.

3. Establish governance controls and proactively manage risks. You cannot implement technology without understanding the potential risks. Real property organizations must review the potential impacts to facility management processes, staffing levels and capabilities before setting technology to work. That means developing a service delivery framework.

4. Finalize a delivery framework and implement the tech solution. Using technology in innovative ways can represent a real step change for many organizations. That’s why change management is such an important determinant of overall success. With a delivery framework finalized, you’ll want to establish a change management plan, including ownership through a Project Management Office. This will enable you to analyze pilot reports, share feedback, adapt in real time and move your people through the change both strategically and empathetically. That kind of measurement and assessment doesn’t stop when you flip the switch on new technology. You’ll also require a means of keeping track of, managing and reporting on change post-implementation.

What’s the key takeaway?

Proper adoption of fit-for-purpose property technology is the key driver to improve portfolio operations efficiency, meet ESG requirements and elevate experiences for employees and other property users. Although some stakeholders perceive this to be an expensive and lengthy process, the benefits far outweigh the hurdles. EY teams have found use cases show some tech solutions are generating ROI in less than 12 months, with operational cost reductions reaching as high as 15% to 20% depending on portfolio size.

How EY teams can help

Strategic Capital Allocation And Portfolio Planning Brochure

Operating Model review

Summary

Across the government and public sector, real property portfolios provide unique opportunities to derive strategic value. This holds even more potential in light of the complex challenges the sector, industry and world are facing. From the need to address climate change to the urgent requirement for more affordable housing and an uncertain socioeconomic landscape: there’s a lot to consider. Carrying out an objective maturity assessment of real property portfolios and teams – and making the most of emerging tech to improve operational efficiency – can help governments transform this challenging time into new opportunities.