EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Trending

-

Advancing Canada’s defence innovation

09 Apr 2026 -

Canadian Insurance Outlook 2026: navigating uncertainty, unlocking opportunity

13 Mar 2026 Financial services -

From bottleneck to accelerator: the strategic role of digital identity controls for industrials and energy companies

18 Feb 2026 Energy and resources

Tax Alert 2024 No. 64, 17 December 2024

On 13 December 2024, the federal government announced in a news release that the 2024 Fall Economic Statement (FES) would include various proposed enhancements to the scientific research and experimental development (SR&ED) tax incentive program. On 16 December 2024, the FES confirmed the proposals included in the news release and announced further clarifications with respect to certain measures. The proposals are intended to generally come into force for taxation years beginning on or after

16 December 2024.1

Background

In the 2024 FES, the government introduced enhanced fiscal measures to support SR&ED, with the objective of increasing research and development (R&D) investments by small and medium-sized Canadian enterprises with high-growth potential.

Currently, the SR&ED tax incentive program offers a limited 15% non-refundable tax credit on eligible SR&ED expenditures for most corporations, excluding Canadian-controlled private corporations (CCPCs). For CCPCs, the program provides a fully refundable enhanced tax credit at a rate of 35% on up to $3 million of qualifying SR&ED expenditures annually, with this expenditure limit subject to a gradual phase-out for taxable capital employed in Canada ranging from $10 million to $50 million.

Key highlights

The FES confirmed the following proposed enhancements, which follow from consultations launched by the Department of Finance earlier this year:

- Increased expenditure limit – Increase, from $3 million to $4.5 million, in the annual expenditure limit on which CCPCs are entitled to earn a 35% SR&ED investment tax credit (ITC).

- Increased phase-out thresholds – Increase, from $10 million and $50 million, to $15 million and $75 million, respectively, in the prior-year taxable capital phase-out thresholds for purposes of determining the annual expenditure limit. In addition, CCPCs will have the option to have their annual expenditure limit determined based on gross revenue instead of taxable capital, as proposed for Canadian public corporations (see below).

- Extending refundability – Extension of the 35% refundable SR&ED ITC to eligible Canadian public corporations, up to the increased $4.5 million annual expenditure limit. However, unlike for CCPCs, the $15 million and $75 million phase-out thresholds for determining the annual expenditure limit will be based on a public corporation’s average gross revenues over the prior three years instead of its taxable capital for the preceding year. In addition, also unlike for CCPCs, qualifying expenditures in excess of an eligible Canadian public corporation’s annual expenditure limit will not be eligible for a partially refundable SR&ED ITC.

- Reinstating capital expenditures – Reinstatement of the pre-2014 eligibility of capital expenditures (for property acquired after 15 December 2024, or lease costs first becoming payable after that date) to both the SR&ED income deduction and the SR&ED investment tax credit. Qualifying CCPCs eligible to earn a 35% SR&ED ITC will be entitled to partial refundability of the credit at a rate of 40% on their capital expenditures.

For purposes of the above enhancements, an eligible Canadian public corporation is a corporation that, throughout the taxation year is resident in Canada; has a class of shares listed on a designated stock exchange or, if not, has elected, or been designated to be a public corporation; and is not controlled directly or indirectly in any manner whatever by one or more nonresident persons. Canadian-resident corporations all or substantially all owned by one or more eligible Canadian public corporations will also be eligible.

The FES further indicates that the proposed changes represent the first of further reforms related to the SR&ED tax incentive program and promoting innovation that the government intends to advance and that more details on the program and updates to qualified expenses will be announced in Budget 2025.

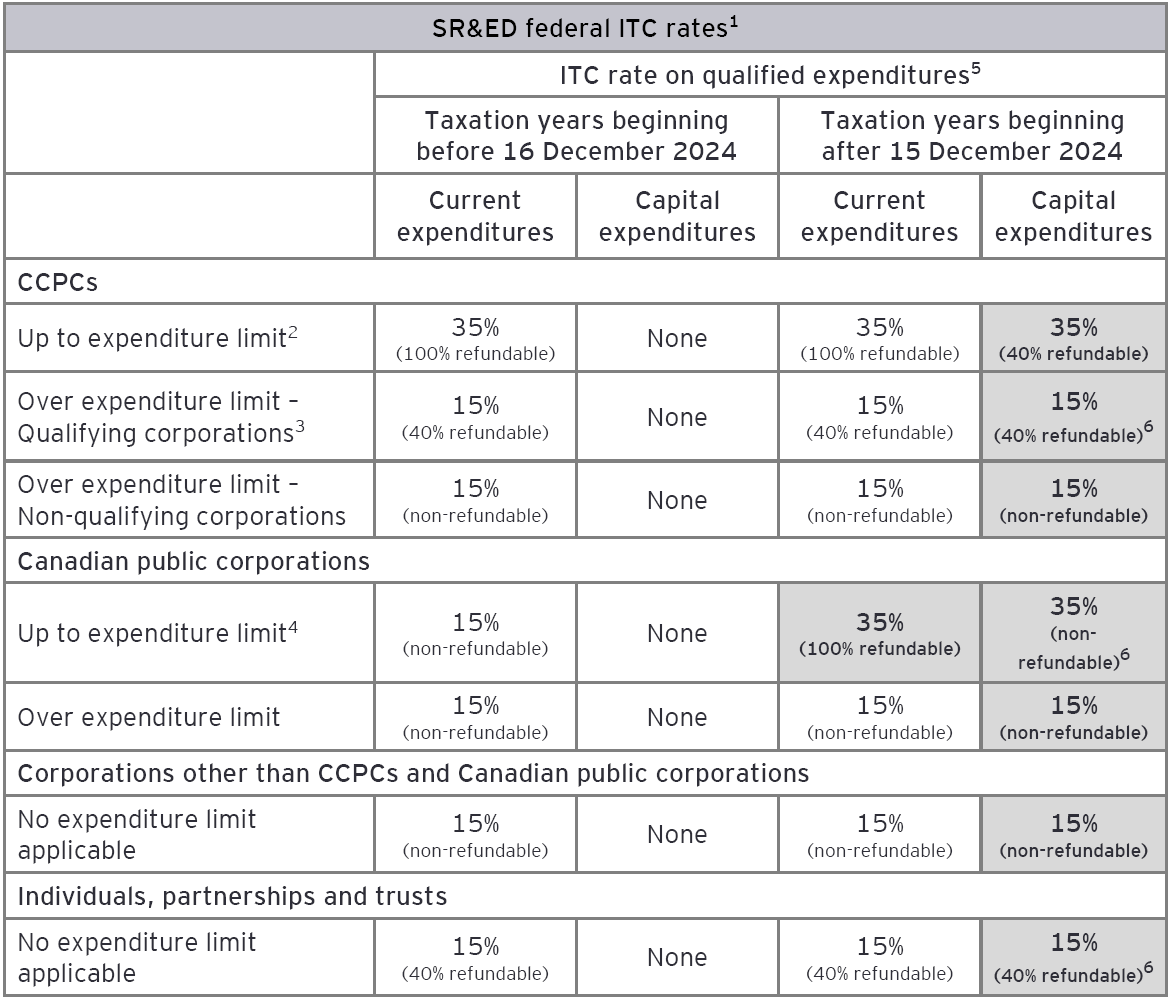

The proposed SR&ED ITC rates are summarized in the following table.

Endnotes:

1 ITCs may be used to offset Part I tax otherwise payable in a taxation year, may be carried back three years or forward 20 years to offset Part I tax, or, if applicable, may be refundable.

2 The expenditure limit is proposed to be increased from $3 million to $4.5 million. The expenditure limit is reduced when the taxable capital of the corporation (or associated group) for the preceding year exceeds a proposed $15 million threshold (previously $10 million), with a proposed phase-out limit of $75 million (previously $50 million). The expenditure limit must be shared among associated corporations. It is proposed that CCPCs will have the option to have their expenditure limit determined based on gross revenue instead of taxable capital employed in Canada, as proposed for Canadian public corporations (see below).

3 A corporation is a qualifying corporation if it is a CCPC in the taxation year and its taxable income for the previous year does not exceed its qualifying income limit for the taxation year. Where a corporation is associated with one or more corporations in the taxation year, the taxable income of all the associated corporations for the preceding year cannot exceed the qualifying income limit of the corporation for the taxation year. The qualifying income limit is $500,000 less any reduction where the taxable capital of the corporation (and of all its associated corporations) exceeds a proposed $15 million threshold (previously $10 million), with a proposed phase-out limit of $75 million (previously $50 million).

4 The expenditure limit is proposed to be $4.5 million and is proposed to be reduced when the average gross revenue of the corporation (or members of a corporate group that prepares consolidated financial statements) over the three preceding years exceeds $15 million, with a phase-out limit of $75 million. The expenditure limit must be shared among members of a corporate group that prepares consolidated financial statements.

5 The rate at which the prescribed proxy amount is calculated is 55% — the prescribed proxy amount, which is used to calculate “notional” overhead expenditures in lieu of itemizing them, is included in the computation of qualified expenditures of taxpayers that elect to use the proxy method. In addition, 20% of the otherwise qualified expenditures made by a taxpayer for SR&ED performed for or on behalf of the taxpayer by an arm’s length person are disallowed. It is proposed that qualified expenditures will include eligible capital expenditures in respect of property acquired after 15 December 2024 or lease costs first becoming payable after that date (similar to pre-2014, qualified expenditures will include expenditures for share-use equipment).

6 We have assumed refundability will be the same for qualifying corporations and individuals, partnerships and trusts as under the pre-2014 rules.

Conclusion

Canadian companies generally have been investing less in R&D now than in the past. The need to increase investment in R&D makes the SR&ED program more important than ever.

On 15 April 2024, in response to a consultation launched by the Department of Finance on 31 January with respect to cost-neutral ways to modernize and improve the SR&ED program, a submission was made by EY Canada with various recommendations, including:

- Revising the program to make the ITC refundable for all companies to have the greatest impact on incenting more R&D investment in Canada;

- Reviewing the ITC rate of 15% for non-refundable claims to assess whether the rate is globally competitive; and

- Reconsidering the current requirement to be a CCPC to earn a 35% ITC, as well as the related $50 million taxable capital limit, in light of the current Canadian business environment.

The changes tabled in the FES on 16 December 2024 should help Canadian companies increase their investment in R&D and, in turn, help boost the percentage of GDP spent on R&D activities. The FES indicates that these proposed changes should provide support to innovative businesses estimated at $1.9 billion over six years, starting in 2024–25, with $370 million per year ongoing. It further states that a portion of this support will be sourced from existing Budget 2024 funding (i.e., $750 million over five years, starting in 2025–26, with $150 million per year ongoing).

It is our view that the changes proposed in the FES are consistent with the recommendations included in our submission to the Department of Finance.

Learn more

For further information or assistance in reviewing the proposed changes and how they may impact your business, please contact one of the following EY advisors.

Toronto

Susan Bishop

+ 1 416 943 3444 | susan.g.bishop@ca.ey.com

Dharmesh Gandhi

+1 416 932 5755 | dharmesh.gandhi@ca.ey.com

Matthew Pearson

+1 416 932 4176 | matthew.pearson@ca.ey.com

Martin McLaughlin

+1 416 932 5751 | martin.mclaughlin@ca.ey.com

Jason Zhu

+1 416 932 6204 | jason.zhu@ca.ey.com

Atlantic Canada

Brett Copeland

+1 902 421 6261 | brett.copeland@ca.ey.com

Quebec

Patrick D’Astous

+1 514 879 2831 | patrick.dastous@ca.ey.com

Nassim Bennacer Langlois

+1 514 879 8097 | nassim.bennacer@ca.ey.com

Prairies

Korey Conroy

+1 403 956 5778 | korey.conroy@ca.ey.com

Dean Anderson

+1 306 649 8354 | dean.anderson@ca.ey.com

British Columbia

Sean Verret

+1 604 891 8341 | sean.verret@ca.ey.com

Mo Mostafaei

+1 604 891 8208 | mo.mostafaei@ca.ey.com

Rod Hynes

+1 604 831 0327 | rod.s.hynes@ca.ey.com

__________________

- For more information on the other measures included in the FES, see EY Tax Alert 2024 Issue No. 63, Federal Fall Economic Statement 2024.

Download this tax alert

Budget information: For up-to-date information on the federal, provincial and territorial budgets, visit ey.com/ca/Budget.