EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Limited, each of which is a separate legal entity. Ernst & Young Limited is a Swiss company with registered seats in Switzerland providing services to clients in Switzerland.

How EY can help

-

Supporting companies to go public and evaluate strategic transactions.

Read more -

We can support you in building an effective and efficient finance function with a range of accounting, reporting and analytics services.

Read more -

Learn more about how our Assurance teams serve the public interest by promoting trust and confidence in business and the capital markets.

Read more

Sector performance

We continue to see the technology sector leading by proceeds (over $34 billion) and by count (202 IPOs), reflecting investor focus on scale, profitable growth paths and platform durability. Mobility ranked second by proceeds (~$19.0 billion), while advanced manufacturing was second by number of deals (185). Sponsors remained active: PE‑ and VC‑backed issuers accounted for 11% of IPOs and 36% of global placement volume.

Switzerland in 2025: quiet Q4, but a solid year

Switzerland recorded three classic IPOs on SIX (prior year: two) and several notable transactions across the year:

- SMG Swiss Marketplace Group listed on SIX on 19 September 2025, raising approximately CHF 903 million – one of Europe’s largest IPOs in 2025 and among the top 10 globally in Q3.

- Aebi Schmidt Group began trading as AEBI on NASDAQ in July 2025 following shareholder approval of its merger with Shyft Group.

- Amrize (a Holcim spin‑off) completed a dual listing on SIX and the NYSE on 23 June 2025.

- Bioversys AG went public on 7 February 2025 with proceeds of roughly CHF 80 million.

Although Q4 brought no new Swiss listings, issuer readiness and investor selectivity supported high‑quality outcomes when windows opened.

How we read the market

Across regions, differences in macro dynamics and policy backdrops shaped liquidity and valuation outcomes. The US benefited from deregulation tailwinds, rate‑cut expectations and strong cross‑border demand. China and Hong Kong rebounded on catch‑up effects and supportive measures. Europe faced structural and geopolitical headwinds, even as the pipeline remained well filled.

Outlook for 2026

With the tariff settlement with the United States and persistently low interest rates, Switzerland offers an attractive environment for new listings in 2026. Our guidance to prospective issuers remains consistent:

- Anchor the equity story in clear, defensible growth drivers and disciplined capital allocation.

- Demonstrate robust governance and disclosure that meet the expectations of selective global investors.

- Prepare early and calibrate timing to volatility and liquidity windows across listing venues.

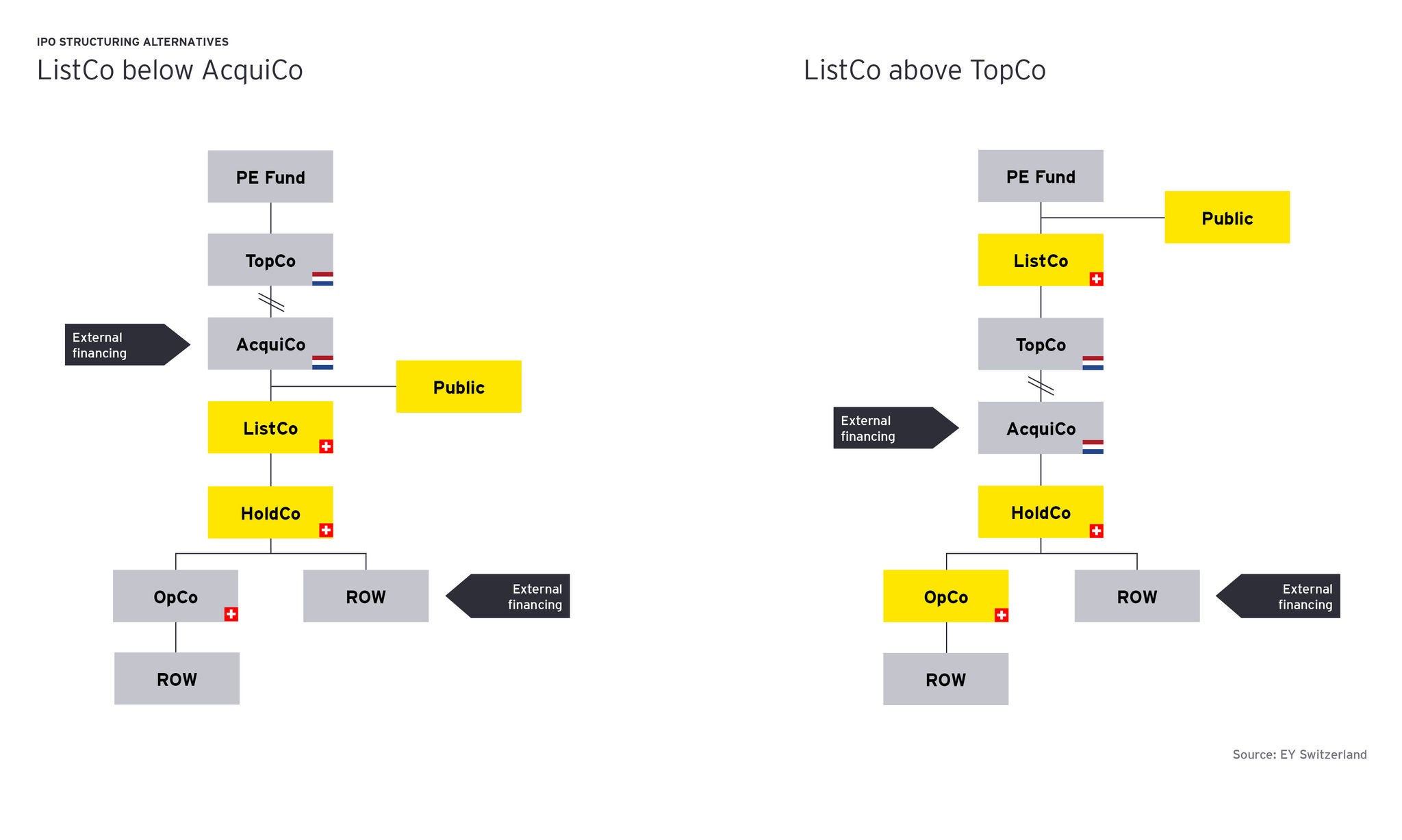

Going public is a significant milestone for any company, but it comes with a host of new responsibilities, particularly in terms of reporting requirements. Candidates need to ensure that they are well prepared and may benefit from external support in assessing readiness and developing a roadmap toward the target structure across eight key areas.