EY se refiere a la organización global, y puede referirse a una o más, de las firmas miembro de Ernst & Young Global Limited, cada una de las cuales es una entidad legal independiente. Ernst & Young Global Limited, una compañía británica limitada por garantía, no brinda servicios a los clientes.

Búsquedas recientes

On April 24th, 2023, the Chilean government introduced a new set of amendments to the Mining Royalty bill (Bulletin N° 12093-08), complementing those presented on the previous week (which are summarized in our Tax Alert), in line with some of the announcements that the government had already made to the market.

The main points are:

- Reduction of the maximum potential tax burden from 48% to 47%, and 45.5% for smaller producers

When the government presented the amendments on April 17th, it introduced a maximum limit to the combined taxation of the mining royalty, corporate tax, and final taxes for the owners of companies, of 48% applied to the RIOMA (Adjusted Mining Operating Income) before taxes. However, it was announced from the beginning that there could be room for its reduction.

Indeed, the amendments reduced the limit in question from 48% to 47%, while for producers of less than 80,000 metric tons of fine copper per year, the limit is set to 45.5%.

Thus, when the sum of the corporate tax, mining royalty, and final tax that owners would pay (assuming they distribute 100% of the profits) exceeds 47% (or 45.5%, if applicable) of the operational profitability -defined as the RIOMA before taxes- then the royalty will be adjusted so as not to exceed 48%.

The final tax, under the assumption of 100% distribution, is calculated considering a tax burden of 35% on the taxable net income, including the corporate tax.

Additionally, the amendments add that in case the taxpayer had been subject to the ad-valorem component of the royalty, this must be added to the RIOMA for the purposes of calculating the limit to the maximum potential tax burden.

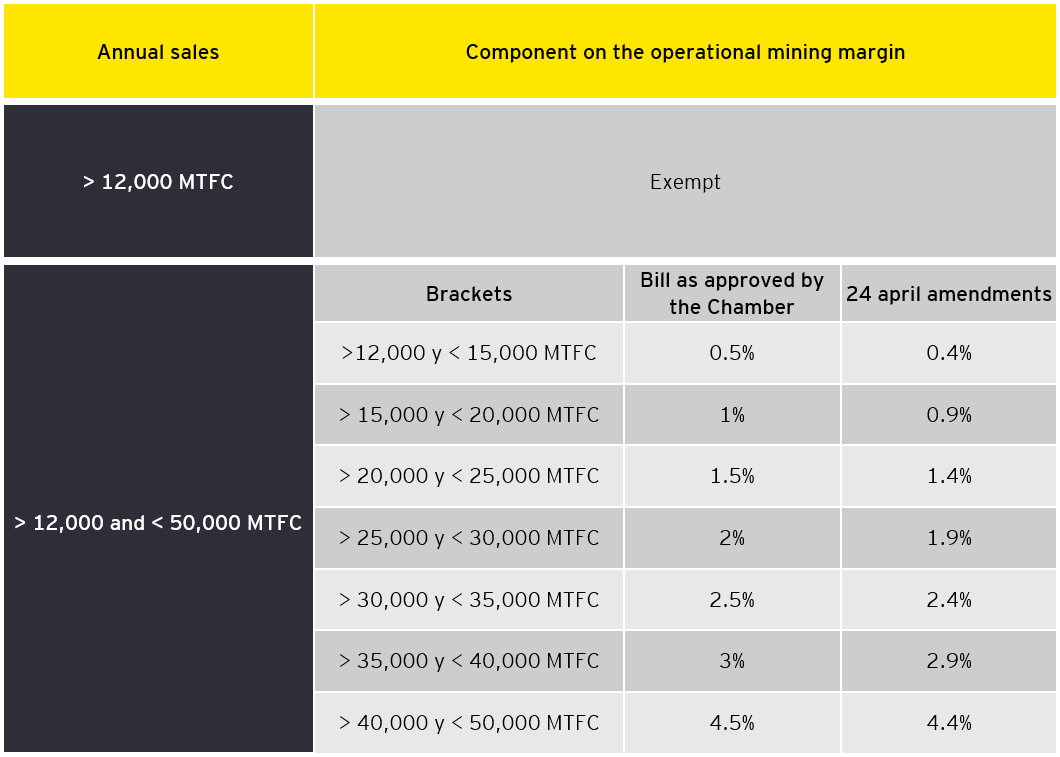

2. Reduction of the marginal rates of the operational component applicable to mining operators whose annual sales range between 12,000 and 50,000 metric tons of fine copper (MTFC).

The amendments slightly lower the rates applicable to this segment, as can be seen from the following table: