EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Trending

-

Advancing Canada’s defence innovation

09 Apr 2026 -

Canadian Insurance Outlook 2026: navigating uncertainty, unlocking opportunity

13 Mar 2026 Financial services -

From bottleneck to accelerator: the strategic role of digital identity controls for industrials and energy companies

18 Feb 2026 Energy and resources

Tax Alert 2022 No. 31, 17 May 2022

The 2021 federal budget proposed an investment tax credit for businesses that incur eligible expenditures related to carbon capture, utilization and storage (CCUS) as part of the federal government’s overall plan to achieve net-zero emissions by 2050.

On 7 June 2021, the Department of Finance launched consultations with stakeholders. EY participated in the consultation period, which closed on 2 December 2021.

Budget 20221 announced an updated version of the credit. The credit would be refundable and available to businesses that incur eligible expenses starting 1 January 2022. Draft legislation has not yet been released.

1 Refer to EY Tax Alert 2022 Issue No. 23

The following is a summary of the draft proposals.

If legislation implementing these measures is passed as proposed, it will apply to eligible expenses incurred after 2021 and before 2041.

The proposed CCUS tax credit

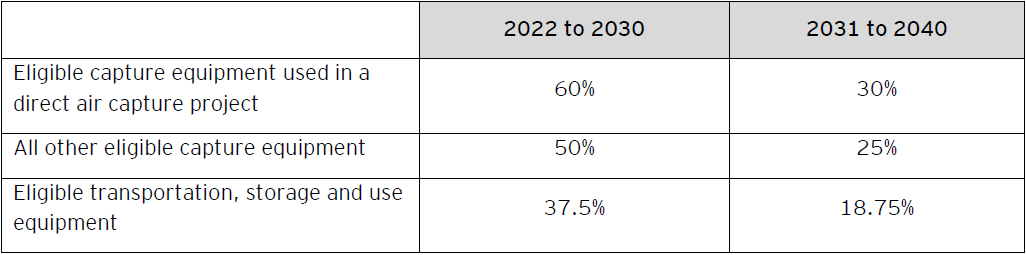

It is proposed that the investment tax credit would be available in respect of the cost of purchasing and installing eligible equipment used on eligible CCUS projects where the captured CO2 is used for an eligible use (see below). The following rates would apply to eligible expenses incurred after 2021 through 2040:

Tax credit rates

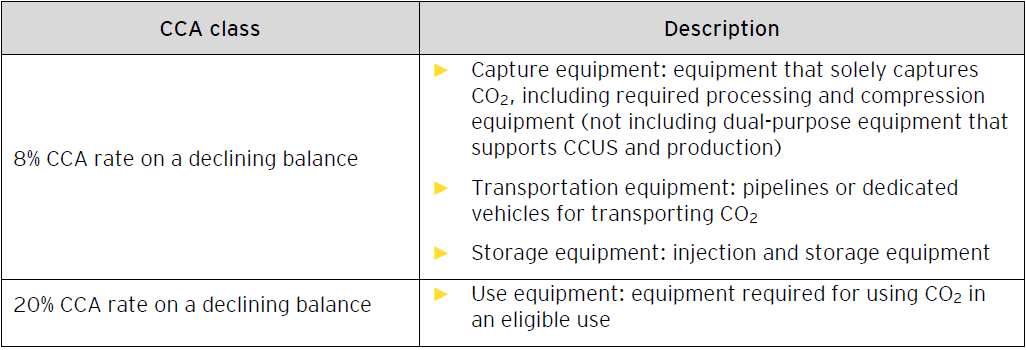

Eligible equipment

Eligible equipment is equipment used solely to capture, transport, store or use CO2 as part of an eligible CCUS project. It will be included in two new capital cost allowance (CCA) classes as described below:

These classes would be eligible for the enhanced first-year depreciation under the Accelerated Investment Incentive and would include the cost of:

- Converting existing equipment for use in a CCUS project or refurbishing eligible equipment;

- Equipment for monitoring and tracking C02; and

- Buildings or other structures that solely support a CCUS project.

Ineligible expenditures include:

- Equipment that is required for hydrogen production, natural gas processing and acid gas injection;

- Equipment that does not support CCUS;

- Feasibility studies and front-end engineering design studies related to a CCUS project; and

- Operating expenses.

The CCUS tax credit can be claimed in respect of the tax year in which the expenses are incurred, regardless of when the equipment becomes available for use. The CCUS tax credit would not be available on equipment in respect of which a previous owner received the CCUS tax credit.

In addition, two new CCA classes are to be established for intangible exploration and development expenses associated with storing C02, depreciable at rates of 100% and 30% respectively.

Eligible project

An eligible CCUS project is a new project that:

- Captures C02 that would otherwise be released into the atmosphere or captures C02 directly from the ambient air;

- Prepares the captured C02 for compression;

- Compresses and transports the captured C02; and

- Stores or uses the captured C02.

Taxpayers may be involved in one or more of the activities that constitute a CCUS project. Note that in order to qualify as a direct air capture project (and be eligible for a higher tax credit rate), the project must capture C02 directly from the ambient air.

Furthermore, equipment will only be eligible if it is part of a CCUS project and is put in use in Canada.

CO2 must be captured in Canada but can be stored or used outside Canada.

In addition, CCUS projects would not be eligible where emission reductions are necessary in order to achieve compliance with the Reduction of Carbon Dioxide Emissions from Coal-fired Generation of Electricity Regulations and the Regulations Limiting Carbon Dioxide Emissions from Natural Gas-fired Generation of Electricity.

Eligible CO2 uses

The extent of the availability of the CCUS tax credit is dependant upon the end use of the CO2 being captured. Eligible uses will initially include dedicated geological storage and storage in concrete. Enhanced oil recovery will not be eligible.

Where eligible equipment is part of a project that plans to store CO2 through both eligible and ineligible uses, the CCUS tax credit would be reduced by the portion of CO2 allocated to ineligible uses over the life of the project, as set out in initial project plans.

Once the project begins operating, taxpayers will be required to track and account for the amount of CO2 being captured and the portions that end up going to eligible and ineligible uses. To the extent that the portion of CO2 going to an ineligible use exceeds what was set out in the initial project plans, taxpayers may be required to repay CCUS tax credit amounts that were previously paid.

Recovery of the CCUS tax

Once projects begin to capture CO2, they will be assessed at five-year intervals, to a maximum of 20 years, to determine if a recovery of the CCUS tax credit is warranted based on the total amount of CO2 going to an ineligible use over the five-year period being assessed. If the portion of CO2 going to an ineligible use is more than 5% higher than initially planned (i.e., the basis on which the CCUS tax credit was paid), then a recovery of the CCUS tax credit will be calculated. Specific design features of the recovery will be released at a later date.

Storage requirements

Geological storage

As regards qualifying dedicated geological storage, the CCUS tax credit will only be available to projects in jurisdictions where there are sufficient regulations to ensure that the CO2 is permanently stored as determined by Environment and Climate Change Canada. Initially, the CCUS tax credit will only be available to CCUS projects that store the CO2 in Saskatchewan or Alberta. All projects will be subject to relevant federal, provincial and territorial regulations.

Storage in concrete

For storage in concrete to be considered an eligible use, the process for using and storing CO2 in concrete must be approved by Environment and Climate Change Canada and demonstrate that at least 60% of the CO2 that is injected into the concrete is mineralized and locked into the concrete produced. The CCUS tax credit would be available in all jurisdictions so long as the process for storing the CO2 is approved.

Validation and verification

Projects would generally be required to undergo an initial project tax assessment if they expect to have eligible expenses of $100 million or greater over the life of the project (based on project plans) or if the project chooses to undergo an initial project tax assessment on a voluntary basis. The tax assessment would identify the expenses that are eligible for the CCUS tax credit, and the tax credit rate that is expected to apply, based on the initial project design. In addition to the project tax assessment and prior to claiming CCUS tax credit amounts, eligible expenses would need to be verified by Natural Resources Canada. It is intended that verification would occur as soon as possible after the end of the taxpayer’s tax year, and in advance of filing its tax return, in order for the refund to be processed upon filing. Administrative details of this process will be provided at a later date.

Public disclosure

In order to be eligible for the CCUS tax credit, CCUS projects that expect to have eligible expenses of $250 million or greater over the life of the project, based on project plans, would be required to contribute to public knowledge sharing in Canada. Details on this process and information to be shared will be provided at a later date.

Taxpayers will also be required to produce a climate-related financial disclosure report highlighting how their corporate governance, strategies, policies and practices will help manage climate-related risks and opportunities and contribute to achieving Canada’s commitments under the Paris Agreement and goal of net zero by 2050. Details on this process and information to be shared are also to be provided later.

Learn more

For more information, contact your EY or EY Law tax advisor, or one of the following professionals:

Calgary

Greg Boone

+1 403 206 5306 | greg.boone@ca.ey.com

Montreal

Krista Robinson

+1 514 879 2783 | krista.robinson@ca.ey.com

Download this tax alert

Budget information: For up-to-date information on the federal, provincial and territorial budgets, visit ey.com/ca/Budget.