EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

-

Streamline ESG reporting with EY’s ESG Compass. Explore ESG solutions, tools, dashboards, and fact sheets to enhance sustainability and compliance.

Read more

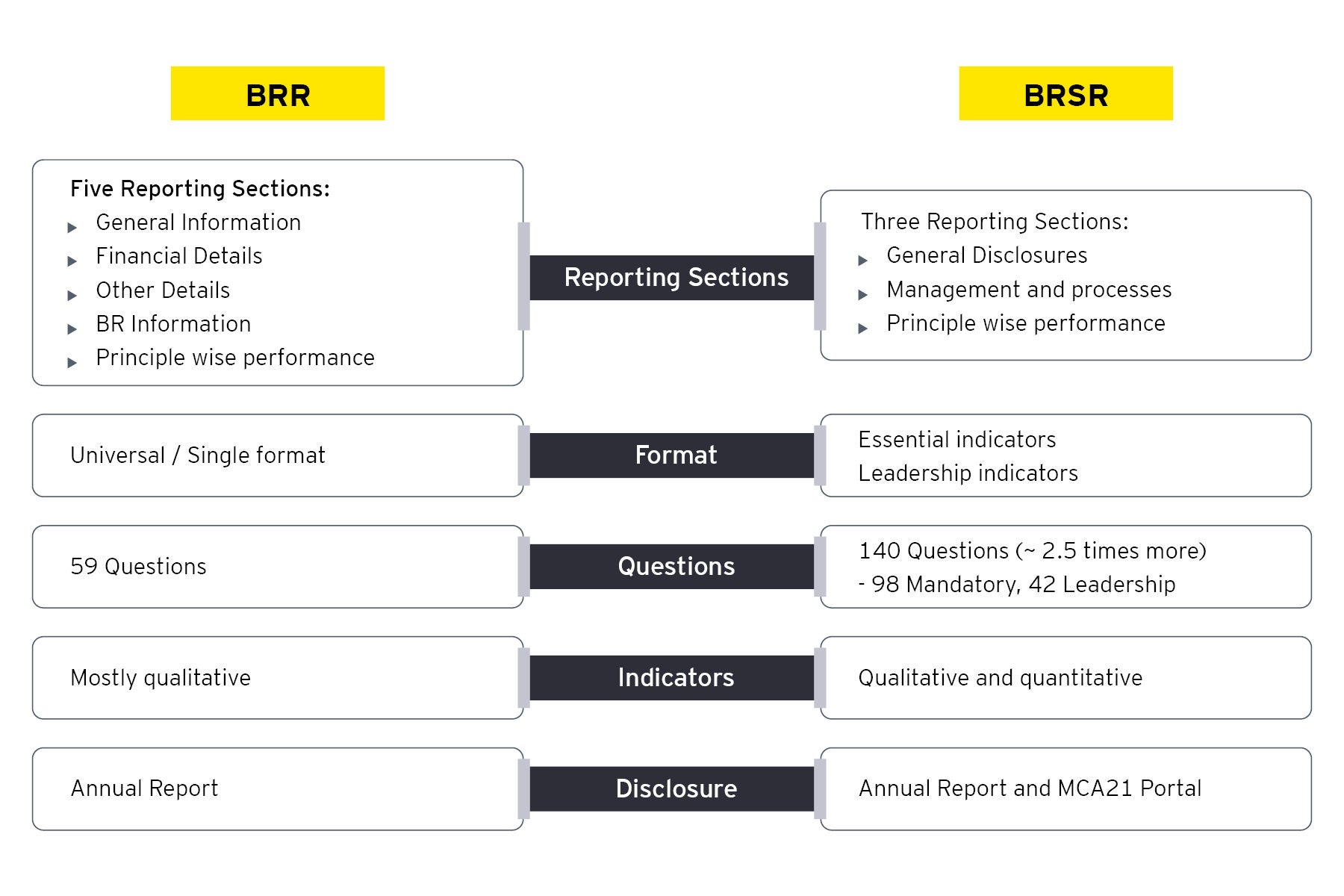

India has emerged as a conscious aspirant and shown promise and capability to take great initiative in paving the way in combating climate change and meeting the Sustainable Development Goals (SDGs) of the United Nations in many of its regulatory schemes internally such as introduction of the Business Responsibility and Sustainability Reporting (BRSR) by SEBI in 2021 and the sustainability reporting format is based on the nine principles of National Guidelines for Responsible Business Conduct (NGRBC) introduced by SEBI.

BRSR is not India’s first foray into ESG regulatory frameworks and disclosures. The original Business Responsibility Reporting (BRR) guidelines were framed by the Ministry of Corporate Affairs (MCA) in 2009. BRR served as a platform upon which a ESG reporting framework having much broader scope could be developed and it served as the launchpad for BRSR which took a decade to refine and broaden its horizons to meet the complex ESG disclosure requirements and meet the global quality requirements and standards that exist in today’s sustainable reporting landscape.