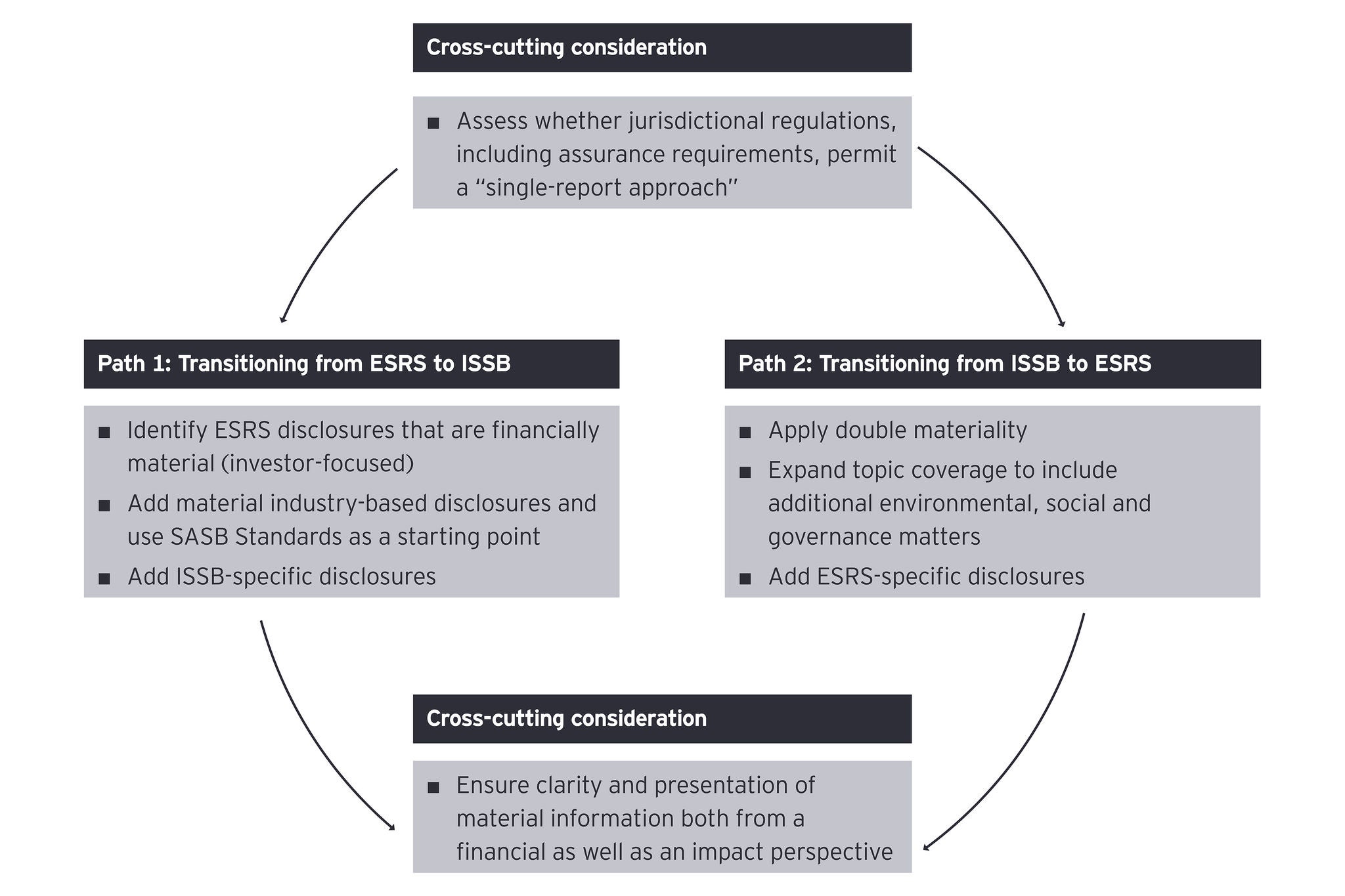

Multinational organizations that are subject to multiple sustainability reporting frameworks, such as IFRS Sustainability Disclosure Standards (ISSB Standards) and European Sustainability Reporting Standards (ESRS), face growing reporting complexity. The idea of “interoperability”, which refers to the compatibility between different sets of reporting standards, could enable a "single‑report" approach. Encouragingly, interoperability has improved with the draft revised ESRS1, but key differences persist, such as materiality, topical and industry-based standards, and reliefs. A single‑report approach that meets both ISSB standards and ESRS requirements is feasible if entities pivot their governance, financial planning and data reporting infrastructure to future-proof their sustainability reporting now. And it isn’t just about ISSB Standards and ESRS, multinationals may face multiple frameworks – either other frameworks, or countries that use ISSB Standards as a baseline and incorporate certain changes, such as those in the United Kingdom (UK), Japan or Australia, that they will be required to adhere to in the future. Obtaining assurance in combination with a single-report approach may bring additional challenges.

1. Why a single-report approach matters

As more jurisdictions adopt, or otherwise use, ISSB Standards or ESRS, multinationals could face overlapping requirements across jurisdictions as well as dual-listing considerations, which make a single-report approach a strategic choice. Additionally, multinationals may have other reasons for voluntarily applying ISSB Standards alongside ESRS, such as to foster comparability to investors outside the European Union (EU).

This is increasingly important, for example, where an ESRS reporting parent has ISSB reporting subsidiaries, or an ISSB reporting parent has EU-based subsidiaries, or a dual-listed group is subject to both regimes. Preparing for both sets of standards from the outset reduces duplicative efforts and reinforces the entity's market credibility.

A single-report approach has considerable potential to help companies:

- Reduce complexity and cost: streamlining sustainability reporting across standards reduces duplication, improves data quality and lowers the cost of ongoing compliance.

- Have stronger governance and insight: embedding sustainability in group-level governance and financial planning strengthens oversight of risks and opportunities and supports strategic decisions.

- Enhance regulatory resilience: a flexible foundation that can be adapted as requirements evolve across jurisdictions.

- Scale reporting capability: building internal capabilities around a unified, core reporting model helps consistent, scalable reporting as expectations rise.