EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

16th Finance Commission’s recommendations have reshaped India’s fiscal transfer system.

- Overview of FC16 and its impact on India’s fiscal transfer architecture

- How FC16 alters the balance of vertical fiscal transfers

- Effect of ending RNGs on vertical and horizontal fiscal balance

- Losing and gaining states under the FC16’s new tax devolution

- Finance Commission’s recommendations on rationalizing state subsidies

- FC16’s role in recentralization and future challenges for states

In brief

- The 16th Finance Commission (FC16) report was released on 1 February 2026.

- FC16’s FY27–31 fiscal imbalance projections seem optimistic as they assume higher nominal growth and do not incorporate GST 2.0‑related revenue losses.

- Discontinuation of revenue need grants (RNGs) marks a departure from the approach of previous FCs.

- The newly introduced contribution criterion under FC16 tax devolution framework reduces the share of large poorer states and several northeastern and hilly states.

Introduction

The FC16 report can be analyzed in terms of five key issues: 1) vertical and 2) horizontal dimensions of fiscal transfers, 3) discontinuation of Article 275 grants, 4) FC16 projections and 5) FC16 roadmap for fiscal consolidation. This article covers the first three subjects. The latter two are proposed to be taken up next month.

Vertical transfers: Implications for GoI and states

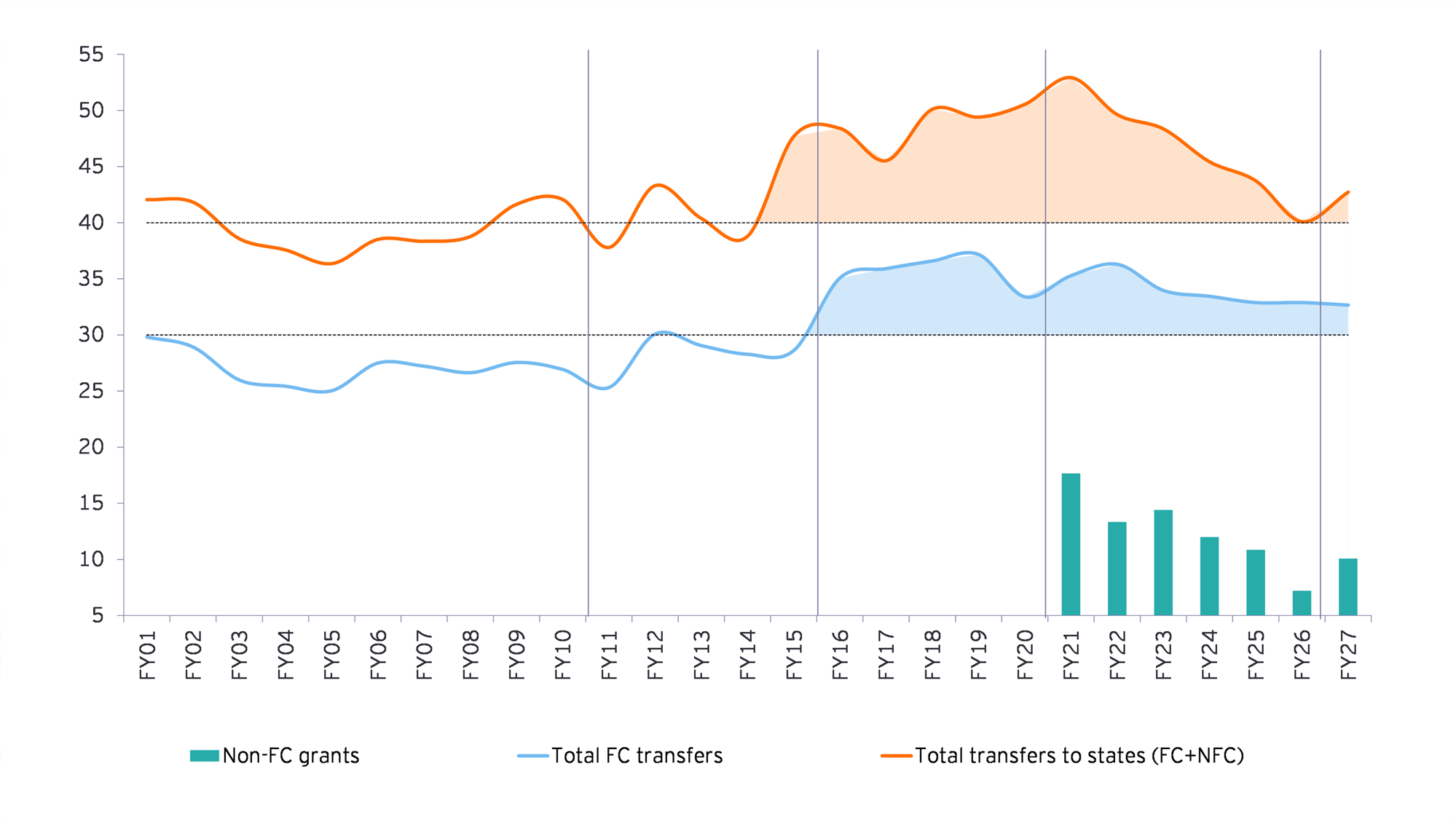

The vertical dimension of fiscal transfers concerns the aggregate flow of resources from the GoI to the states. A major rebalancing occurred with FC14 (FY16-20), which raised the states’ share in the divisible pool of central taxes from 32% to 42%. FC14 also recommended substantive RNGs under Article 275 for many states, commonly referred to as revenue deficit grants (RDG). These recommendations substantially increased the post transfer share of states in combined GoI-state revenue receipts from an average of 62.6% during the FC11, FC12 and FC13 periods to 67.4% during FC14 and FC15 periods.

Since FY16, the first year of the FC14 period, however, a series of incremental policy changes have steadily diluted this shift. These include 1) rising reliance of the GoI on cesses and surcharges that are not shareable with states, 2) reduction in the GoI’s funding share for centrally sponsored schemes, and 3) the non acceptance of sector and state specific grants recommended by FC15. Consequently, the states’ share in total transfers relative to the GoI’s pre transfer revenue receipts fell from its peak of 50.5% in FY20 (FC14 award period) to 40.1% in FY26 (RE) (Chart 1).

Chart 1: Total transfers as % of GoI’s pre-transfer revenue receipts

Source: Source: IPFS, Union Budget, CGA, EY Estimates

FC16 reinforces this trend by 4) discontinuing RNGs, 5) not recommending sector and state specific grants, and 6) reducing grants to local governments and for disaster management (relative to GDP). In addition, the GoI reduced its own share in the funding of VB-G-RAM G employment scheme. In effect, the GoI regained an increasing share of combined revenues after transfers, approaching the level that prevailed prior to FC14.

Discontinuation of RNGs: Vertical and horizontal implications

One of the most consequential departures under FC16 is the discontinuation of RNGs. Historically, these grants played a central role in ensuring that, after tax devolution, states were able to meet their normatively assessed expenditure needs. Earlier FCs utilized the following framework:

Assessed revenue need of a state = assessed expenditure need – share of central taxes through tax devolution – assessed own revenue receipts

This ensured that no state was left with a normative revenue need gap after Finance Commission transfers. However, the discontinuation of RNGs by FC16 implies that many states are likely to have post-transfer assessed revenue deficits.

The Commission justifies this by pointing to a declining trend in RNGs under FC15 and presenting an aggregate assessment suggesting that states, taken together, have a low revenue deficit. The aggregate revenue deficit of deficit states is estimated at 0.8% of GDP for FY24, equivalent to a substantial level of 6.4% of GoI’s pre-transfer gross revenue receipts. It may be noted that revenue surpluses of some states cannot offset revenue deficits of others. Thus, FC16 was expected to assess the revenue needs of individual states over its award period, particularly when the devolution criteria and their associated weights have undergone a change. However, FC16 provides only a partial estimate of the aggregate of states, making the framework less transparent. Further, under earlier arrangements, states that lost due to changes in the tax devolution formula could be compensated through Article 275 grants. With these grants discontinued, such losses persist without being offset.

The post transfer revenue need of a state depends, among other things, on the level and distribution of tax devolution. If states as a group show a revenue surplus, or if the GoI remains in deficit, it suggests that the FC has given excessive devolution to the states. The FC’s task is to ensure that neither the GoI nor any state consistently ends up with surpluses or deficits in its assessment. In this context, the FC16 appears to have relied on a ‘grand bargain’[1] between the GoI and the states rather than explicitly deriving a distribution of their combined resources that is expected to place both in a position of near balance.

Inter se allocation of GoI’s sharable taxes: Transfer profiles of losing and gaining states

The horizontal distribution of tax devolution is governed by the criteria and weights the FC chooses. A notable feature in the FC16 recommendations relates to the introduction of a new criterion based on a state’s contribution to all state GSDP. This contribution criterion has been assigned a weight of 10%.

When all criteria are applied together, clear patterns emerge in terms of gaining and losing states. Total loss over the FC16 award period for the group of large‑population and low‑income states including Madhya Pradesh, Uttar Pradesh and Bihar amounts to INR1,62,106 crore (Table 1). For the group of small and/or hilly states, the cumulative loss is INR89,618 crore.

The contribution criterion raises deeper questions about the balance between equity and efficiency. The Commission presents this criterion as efficiency enhancing, but it relies on per capita GSDP[2], a variable already used in the income distance criterion for equity. Using the same underlying variable to pursue two distinct objectives defies the Tinbergen rule[3], weakening the equalization content of transfers and creating distortions in terms of uneven patterns in per capita transfers and regressivity at the upper end of the income scale.

Subsidies and freebies

FC16 recommended that states should review and rationalize subsidies and freebies and retain only those that are well targeted towards the poor. However, it may have been more effective if FC16 had undertaken a normative assessment of state‑level expenditures and explicitly identified and excluded subsidies that were not justified. A similar normative review may also have been carried out for expenditures of the central government.

Conclusion

FC16 marks a gradual recentralisation of resources by discontinuing RNGs and not recommending any state or sector specific grants, reversing much of the gains that states saw after FC14 recommendations. The revised tax devolution formula redistributes resources unevenly, with large low income and small/hilly states losing significantly. The introduction of the contribution criterion has made transfers less equalising across states, and the absence of state wise revenue needs assessment has reduced transparency. Although FC16 urges rationalisation of subsidies and freebies, it does not undertake a normative expenditure review of the states.

Download the full pdf

FAQs

Summary

16th Finance Commission awards create tighter fiscal space for states, near complete dependence on criteria-based tax devolution, and unresolved concerns around equity and balance in India’s fiscal federal architecture.

How EY can help

-

Watch provides an in-depth review of salient developments in India’s macro economy and economic policy in a global context.

Read more -

Tax policy advisory services by EY India offers insights & strategies to navigate complex tax regulations, driving business growth and compliance.

Read more -

EY-Parthenon professionals can help your business design and provide transformative strategies for sustainable growth. Learn more.

Read more

Related articles

FY27 Budget: Downward expenditure adjustments and slowing fiscal consolidation

FY26 tax reforms reduce revenues by INR1.925 lakh crore; FY27 sees slower fiscal consolidation, lower state transfers and subdued nominal GDP growth.

FY27 Budget outlook: Sustaining growth while negotiating global headwinds

Read about FY27 Budget Outlook for India, highlighting growth prospects with FY26 real and nominal GDP projected at 7.4% and 8.0%, fiscal consolidation targets, potential deficit reduction and expenditure priorities.

With robust economic growth, what are the Union Budget 2026 prospects?

India’s FY26 outlook shows strong 8% growth, low inflation and fiscal pressures, with GST revenues, capex momentum and consolidation shaping the economic path.