EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

India’s promising growth narrative faces short- and long-term pressures.

In brief

- OECD’s 2025 projections for India reconfirm its emergence as world’s leading economy, in a selected feasible scenario.

- In that scenario, in PPP terms, the Indian economy is projected to overtake the US and Chinese economies in 2045 and 2063, respectively.

- India’s per capita GDP is forecasted to cross the corresponding global average by 2065 in PPP terms in this scenario.

Emerging pressures: Short- and long-term

The economic shadow of the continuing West Asian conflict is likely to be accompanied by a number of other developments casting clouds over the Indian economy. Apart from the relatively high crude prices and uncertain supplies of crude, gas and other energy products, there may also be supply and price shocks related to other primary commodities. The Indian economy may also be affected by the forthcoming El Niño, which is likely to impact agricultural output in general and food output in particular.

Possible fertilizer shortages may pose additional challenges. India’s exports are also likely to show a subdued performance due to a slowdown in global growth resulting from the crude supply and price shock. Further, there may be a reduction in inward remittances from the gulf countries affected by the West Asian crisis.

Along with these, the fast-paced evolution of AI is expected to have a long-term impact on employment of India’s skilled labor force which had, hitherto, found placement in the lucrative IT sector job market. In the context of global competition for strategic and economic influence, policy choices by advanced economies may not always fully align with India’s priorities. These developments may have a bearing on India’s growth performance both in the short and long run.

Reconfirming India’s growth prospects: OECD’s latest projections

OECD’s latest projections of country-wise potential GDP (2025) provide six plausible scenarios. According to the OECD, India’s potential real GDP growth had reached a level of 6.4% in 2023 (FY24). Going forward, focusing on the ET2 scenario, which assumes median climate damage, fast reduction in carbon mitigation costs and accelerated energy transition, growth of India’s potential GDP remains close to 6% up to 2031. Subsequently, it declines steadily, dropping below 2% in 2068. Juxtaposing this growth trajectory with India’s population growth profile, the country’s comparative growth advantage appears to be in the decades where the share of its working age population remains above 75% or so.

India’s share of working age population to its total population falls below 75% close to 2060[1]. The OECD projects the Indian economy to overtake the US and Chinese economies respectively in 2045 and 2063, thereby becoming the world’s largest economy in PPP terms.

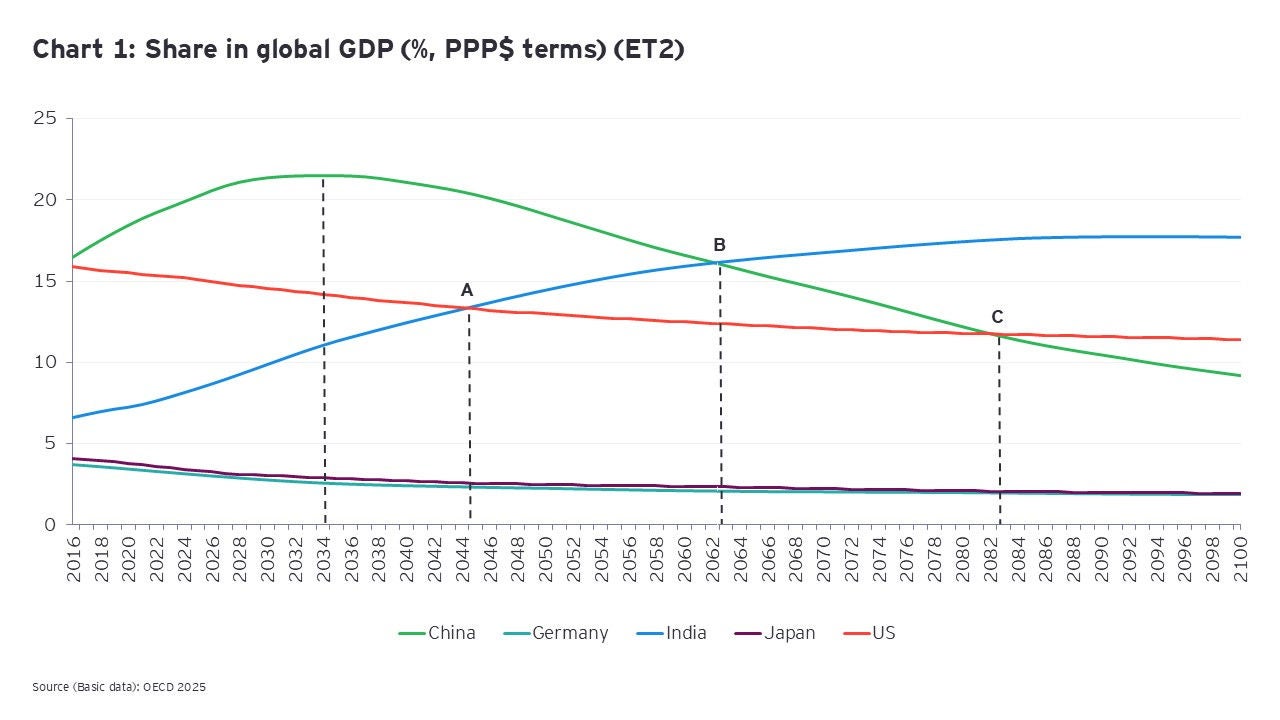

Important crossover years

In OECD’s ET2 scenario, India’s share in global potential GDP relative to other contemporary major economies is shown in Chart 1. With respect to countries that have a share higher than 10% in global GDP in PPP terms, there are three significant points of intersection that are marked as A, B and C. At point A, OECD projects India to overtake the US economy in 2045, and at point B, in 2063, it projects India’s GDP to overtake China’s GDP in PPP terms. Until the end of the projection period, India’s share in the world economy remains the largest.

Notably, China’s share, which was projected at 21.5% in 2034, steadily declines to reach a level of below 10% by 2094. In fact, US overtakes China again in terms of share in the world economy at point C in 2082. The US share, however, continues to remain below that of India, which progressively increases until it stabilizes at around 17.7% 2082 onwards. In 2100, the Indian economy is projected to be 55% larger than the US and 93.2% larger than China in PPP terms.

Evolving profile of per capita income

India is in a unique situation where its population is also growing fast along with its PPP GDP. This combination slows down the growth of its per capita GDP. This is why it is shown to take relatively long for India’s per capita GDP to reach the level of global per capita GDP. However, within the century, India does cross this threshold in 2068 (Chart 2). By the end of the century, India’s per capita PPP GDP is projected to be nearly 20% higher than the corresponding world per capita GDP.

Realigning growth strategy: coping with vulnerabilities, optimizing demographic dividend

In view of the mounting pressures emanating from the West Asia crisis impacting India, and the changing world trade and economic order in general, India may recast its growth strategy to prevent any persistent damage to its stipulated medium to long-term path. In this context, as short-term measures, the PM recently proposed a seven-step strategy, including reduction in gold imports, saving in foreign travel, and strategies for reducing domestic consumption of fuel.

Going forward, India may formulate a long-term growth strategy to prepare for unanticipated economic shocks and vulnerabilities by 1) building strategic reserves for crude oil, LPG, fertilizers, processed and unprocessed rare earth materials, and basic medicines and critical medical equipment, 2) building dual-use infrastructure to minimize adverse impacts of unanticipated nuclear and biological threats, and 3) re-strategizing achieving sustainable levels of current account and fiscal imbalances. Among other initiatives, an accelerated nuclear and green energy transition by India, which includes Thorium-based production, focussing on developing indigenous technologies, may also be needed along with a sharper shift towards electric vehicles. Recent diversification of sources of petroleum has already helped India reduce its dependence on the Strait of Hormuz. As per a PIB release[2], share of crude oil coming through the Strait of Hormuz has come down to 30% compared to 45% earlier. India may need to work on diversification and acceleration of alternative trade corridors/routes including the India-Middle East-Europe Economic Corridor and the Indo-Pacific Corridor covering the Malacca Strait.

OECD’s (2025) projections of India’s potential GDP growth in PPP terms are not overly optimistic. These fall from a peak of 6.7% to about 2% over the decades. Actual performance can improve over the OECD projections by following policies that maximize saving and investment rates and labor productivity. At the same time, long-term structural changes, particularly those pertaining to AI’s employment impact will pose challenges for optimal utilization of India’s demographic dividend.

To cope with the evolving structural changes in the world economy and the technology-related impact on potential employment, an accelerated shift in India’s human resource development strategy and training and skilling of its young age and working age population should be implemented.

Learn more about India's economic outlook

Download the full pdf

Summary

In view of the ongoing West Asian crisis impact on India and the changing world economic order, to preserve India’s long-term growth prospects, there is a need to 1) build strategic reserves for crude oil, gas, fertilizers and rare earth materials, 2) re-strategize achieving sustainable levels of current account and fiscal imbalances, and 3) build dual-use infrastructure to minimize impacts of unanticipated nuclear and biological threats.

How EY can help

-

Watch provides an in-depth review of salient developments in India’s macro economy and economic policy in a global context.

Read more -

Tax policy advisory services by EY India offers insights & strategies to navigate complex tax regulations, driving business growth and compliance.

Read more -

Our BEPS team can help you navigate the OECD Multilateral Instrument (MLI) and understand what it means to your business and structure. Find out how.

Read more

Related articles

Why recent macro fiscal shifts call for a reassessment of FC16 projections

New GDP data, GST changes and global uncertainty call for a reassessment of FC16 projections and fiscal sustainability in India.

GoI-state fiscal transfers: The next five years

The 16th Finance Commission report analyzes tax devolution, grant discontinuation and fiscal transfer shifts impacting the finances of states and Center.

FY27 Budget: Downward expenditure adjustments and slowing fiscal consolidation

FY26 tax reforms reduce revenues by INR1.925 lakh crore; FY27 sees slower fiscal consolidation, lower state transfers and subdued nominal GDP growth.