EY helps clients create long-term value for all stakeholders. Enabled by data and technology, our services and solutions provide trust through assurance and help clients transform, grow and operate.

At EY, our purpose is building a better working world. The insights and services we provide help to create long-term value for clients, people and society, and to build trust in the capital markets.

Effective as of 1 January 2022, the Cypriot Income Tax and the Assessment and Collection of Taxes Laws were amended to introduce Transfer Pricing rules in accordance with the Organization for Economic Co-operation and Development on Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations (OECD TP Guidelines).

The TP rules provide for the content of the TP Documentation Files (Local and Master Files) and the Summary Information Table (SIT) as well as introduce the concept of Advance Pricing Agreements (APAs).

Master File is a document which contains high level information about the global business operations of a multinational group. The content of the Master File should be in line with the OECD TP Guidelines. The Master File shall be prepared by Multinational groups that meet both of the below requirements:

Consolidated revenue exceeding Euro 750 million (groups with CbCR obligation)

The Ultimate Parent Entity (UPE) or Surrogate Parent Entity of the group is Cypriot tax resident company.

The Master File is to be prepared by the Income Tax Return submission deadline for the respective tax year. After the preparation deadline the Master File must be made available by the taxpayer and submitted to the tax authorities upon request within 60 days.

The Local File is a document which contains detailed information about the local business of the taxpayer, including description and documentation of related- party transactions. The content of the Local File should be in line with the OECD TP Guidelines. The Local File shall be prepared by Cypriot tax resident companies/Cypriot tax resident companies with a foreign branch/Cypriot branches of non- Cypriot tax resident companies being engaged in related-party transactions with an accumulated amount during the tax year exceeding Euro 750,000 (per transaction category as defined in the SIT).

The Local File should be subject to Quality Assurance Review (sign-off) by a person who has a practicing certificate of ICPAC or any other recognized institute of certified accountants in Cyprus.

The Local File is to be prepared by the Income Tax Return submission deadline for the respective tax year. After the preparation deadline the Local File must be made available by the taxpayer and submitted to the tax authorities upon request within 60 days.

The SIT is an additional form (i.e., TP return) that should reflect high-level information about the taxpayer’s related-party transactions, including details of the counterparties, category of intercompany transactions entered into, and amound per transaction category. The categories of transactions as per SIT is Goods, Services, Royalties and Other Intangibles, Financing Transactions and Others.

The SIT reporting obligation is applicable to all taxpayers engaged in related party transactions, with no reporting materiality threshold. The SIT shall be submitted to the tax authorities on an annual basis concurrently with the Income Tax Return.

Taxpayers may submit advance pricing agreements (APA) to the Cypriot tax authorities, to agree on pricing methodologies in advance. Such APAs may have unilateral, bilateral or multilateral application and will be valid for a period of up to four years.

More specifically, an APA determines an appropriate set of criteria (e.g., method, comparables and appropriate adjustments thereto, critical assumptions as to future events) to be applied for a fixed period of time with respect to specific controlled transactions concluded based on the arm’s-length principle.

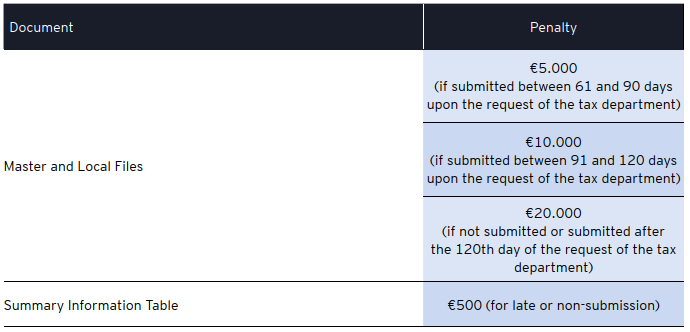

Penalties for non-compliance with the submission deadlines for the TP Documentation Files and the SIT shall be as follows:

Transfer Pricing Alert – February 2023

On 10 February 2023, the Cyprus Tax Authority released a set of FAQs which addresses a number of aspects relating to the application of the new TP legislation that is effective as of 1 January 2022.

One of the main points addressed relates to the abolishment of the Interpretive Circular 3 (dated 30 June 2017) on back-to-back financing arrangements. The abolishment is effective as from 1 January 2022, as announced in the Circular issued on 5 January 2023.

The following eight FAQs are addressed and published on Tax Department’s website.

FAQ Transfer Pricing Table

No.

Frequently Asked Questions (FAQs)

Answer

1

If the controlled transactions in category "A" cumulatively exceed €750,000 or shall exceed €750,000 on the basis of the arm's-length principle as described in article 33(9)(a) of the Income Tax Law (ITL), and at the same time the controlled transactions in category "B" cumulatively do not exceed the €750,000 threshold in a tax year, is there an obligation to include the controlled transactions of category "B" in the Cyprus Local File?

No, there is no obligation to include category "B" controlled transactions in the Cyprus Local File.

Only, the controlled transactions of a category which cumulatively exceed or shall exceed €750,000 on the basis of the arm's-length principle during a tax year must be documented and analyzed in the Cyprus Local File.

In this specific example, it would be category "A" controlled transactions only.

2

How is the €750,000 threshold determined in the context of rental income activities during each tax year?

The threshold is determined by reference to the total rental income on the basis of the arm's-length principle in a tax year.

3

Do purchases and sales need to be aggregated for the purposes of assessing whether the threshold has been exceeded?

Yes, the threshold refers to the absolute values of the controlled transactions for each category occurring in a tax year. For example, if total purchases and total sales amount to €400,000 and €500,000, respectively, the cumulative amount in this category is €900,000. Therefore, the threshold in this category has been exceeded.

4

Are the Cyprus Local File and Summary Information Table prepared using the tax year or the accounting year of the company?

The Cyprus Local File and Summary Information Table are prepared with respect to the tax year.

5

Under which category of the Summary Information Table should financial guarantees be reported?

Financial guarantees should be reported under the category "Financial Transactions."

6

Should a benchmarking study be prepared every tax year, or only if something changes with regards to the intra group loans?

A benchmarking study should be prepared when an intra group loan is initiated, and updated when:

•New loans are provided or received by the company; or

•Significant terms of the existing loans change or are amended; or

•The functional profile of the company changes; or

•The market and economic conditions change significantly (if applicable).

The above list is indicative and not exhaustive. Further guidance is provided in the OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations.

Please note that in accordance with article 33(10) of the ITL, the master file (where applicable) and the local file must be updated every tax year.

7

Who is responsible for the completion and submission of the summary information table?Who is responsible for the completion and submission of the summary information table?

It is the responsibility of the taxpayer to complete the Summary Information Table.

The Summary Information Table is to be submitted by the statutory auditor or tax consultant.

8

Is the circular dated 30 June 2017 with title "Tax treatment of intra group back-to-back financing transactions" still applicable following the enactment of the new TP legislation and regulations?

The back-to-back circular was abolished as from 1 January 2022.