EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Indonesia's Ministry of Finance issues regulation to implement BEPS 2.0 Pillar Two

- On 31 December 2024, Indonesia issued an Implementing Regulation on Global Minimum Tax under BEPS 2.0 Pillar Two, which includes the Income Inclusion Rule (IIR), Domestic Top-up Tax (DMTT) and Undertaxed Payment Rule (UTPR).

- The regulation is effective for fiscal years beginning on or after 1 January 2025 and addresses obligations to submit a Top-up Tax Return for GloBE, DMTT and/or UTPR, a GloBE Information Return and a Notification.

Executive summary

On 31 December 2024, the Indonesian government enacted the Implementing Regulation on Pillar Two (i.e., Top-up Tax) through Ministry of Finance Regulation No. 136 Year 2024 (the Regulation).

This Regulation implements the Global Anti-Base Erosion (GloBE) Rules, part of the Organisation for Economic Co-operation and Development's (OECD's) Base Erosion and Profit Shifting (BEPS) 2.0 Pillar Two framework. The new Regulation mandates a supplementary tax for in-scope multinational enterprises (MNEs) operating in jurisdictions where the effective tax rate (ETR) of their constituent entities (CEs) falls below the 15% threshold.

In-scope MNEs

The legislation applies to all CEs in Indonesia that are members of an MNE group with an ultimate parent entity (UPE) that has consolidated revenues in Indonesian Rupiah equivalent to €750m or more in at least two of the four preceding fiscal years.

Effective date

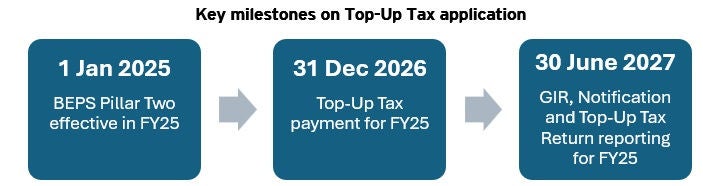

The Regulation is effective for fiscal years beginning on or after 1 January 2025.

Top-up tax charging mechanisms

The Regulation establishes three principal mechanisms for the levy of top-up taxes in accordance with the OECD Model Rules. The legislation also furnishes specific details, including safe harbors, elections and administrative obligations.

1. Domestic Minimum Top-up Tax (DMTT): All CEs in Indonesia will be liable to pay top-up tax under the DMTT if Indonesia's ETR is lower than 15%. The DMTT is intended to be a Qualified Domestic Minimum Top-Up Tax (QDMTT) under the OECD Model Rules.

2. Income Inclusion Rule (IIR): An Indonesian UPE, Intermediate Parent Entity or Partially Owned Parent Entity will be liable for the top-up tax under the IIR if one or more CEs in foreign jurisdictions in which it holds direct and indirect ownership are in low-taxed jurisdictions (i.e., jurisdictions where the ETR is lower than 15%).

3. Undertaxed Payment Rule (UTPR): All CEs in Indonesia will be liable for the allocated top-up tax under the UTPR if the top-up tax in low-taxed foreign jurisdictions has not been fully paid, either under a QDMTT or IIR, in those jurisdictions. The UTPR is deemed to be zero if the MNE Group is in the initial phase of international activity and fulfills the following requirements:

- It has a CE presence in no more than six countries/jurisdictions.

- The net book value for tangible assets outside the "reference jurisdiction" is no more than €50m.

The application of UTPR based on the Regulation will be begin from 1 January 2026.

Safe harbors

The Regulation also provides safe harbor provisions, including permanent safe harbors, a transitional country-by-country reporting (CbCR) safe harbor, a UTPR safe harbor and simplified calculation safe harbors for nonmaterial constituent entities.

The safe harbor will be applied if one of the three tests is met: (1) revenue and income is below the de-minimis threshold; (2) the ETR equals or exceeds an agreed rate; or (3) no excess profits remain after excluding routine profits (i.e., the amount of "substance-based income exclusion" is higher than the profit before taxes). If one of the three tests is met, the top-up tax is set at zero.

The DGT has the authority to conduct compliance tests on the application of safe harbors by issuing a request-for-clarification letter.

Filing obligations

All CEs in Indonesia are required to submit the following to the Directorate General of Tax (DGT):

Top-up Tax Return: If the UPE of an in-scope MNE Group is an Indonesian tax resident, the Top-up Tax Return for GloBE, DMTT and/or UTPR must be submitted to the DGT as follows:

- The GloBE Return must be submitted by the Indonesian UPE.

- The DMTT Return must be submitted by the Indonesian CEs.

- The UTPR Return must be submitted by the Indonesian CEs if there is any tax payable based on the UTPR in Indonesia.

The DGT may provide further details on the form, guidance, payment and reporting on the Top-up Tax Return.

GloBE Information Return (GIR): In addition to the Top-up Tax Return, the Indonesian UPE must also submit a GIR, which consists of detailed information on the CEs, the MNE Group's organizational structure and the top-up tax computation. The Indonesian CE will be required to file a GIR with the DGT if the non-Indonesian UPE designates the Indonesian CE as a filing entity or if the Filing CE is in a country/jurisdiction that does not have a qualifying competent authority agreement in effect with Indonesia.

Notification of in-scope MNE: All CEs in Indonesia that are members of an in-scope MNE must submit a Notification to the DGT. An exemption applies if the Indonesian CE has submitted a GIR to the DGT. The notification must include detailed information about the UPE, detailed information of the Indonesian CEs and the designated CE responsible for filing the GIR.

Filing and payment deadlines

Any top-up tax that is payable (DMTT, IIR or UTPR) is due by the end of the following fiscal year. The GIR and Notification filings with the DGT must be submitted within 15 months after the end of the UPE's fiscal year. The Top-up Tax Return must be submitted four months after the end of the fiscal year in which the top-up tax becomes payable — i.e., with regard to a payment due 12 months after year-end, the Top-Up Return is due 16 months after year-end.

For the first fiscal year in which the MNE group is subject to the top-up tax under this Regulation, there is a three-month extension (to 18 months) for the GIR and a two-month extension for the Top-up Tax Return. Thus, the first payments are due 31 December 2026, and the first wave of filings will be due by 30 June 2027 for in-scope MNE groups with a fiscal year ending on 31 December 2025.

Surcharge and penalties

Surcharges and penalties will apply for non-submission or late submission of the Top-up Tax Return, as well as for unpaid or late-paid Top-up Tax, in accordance with the surcharges and penalties regulated under the General Procedure and Provision of Tax Law (KUP Law).

Next steps

Actions for in-scope MNEs to consider include:

- Evaluate the impact of the Top-Up Tax on their groups, including DMTT and/or IIR for Indonesian-based in-scope MNEs, and DMTT for foreign-based in-scope MNEs with an Indonesian subsidiary, especially where the Indonesian subsidiary has been granted a Tax Holiday.

- Consider assessing qualification for safe harbors, as it could help reduce the complexity of ETR calculation and release top-up tax burdens.

- Prepare for top-up tax compliance obligations and closely monitor further guidance as it becomes available.

1. Consider top-up tax provisioning (if any) and comply with the relevant financial reporting obligation (e.g., disclosure requirements).

2. Monitor the upcoming regulations on tax incentives, which are expected to provide cash grants and/or various incentives to eligible investors. (The regulations are aimed at maintaining Indonesia's competitiveness and attracting foreign direct investment to the country.)

- Companies liable for DMTT should revisit existing tax incentive regimes and observe new relief measures (e.g., cash grants) for future investment planning. An incentive feasibility study in light of the Pillar Two implementation should also be considered.

- MNEs considering group restructuring, mergers or acquisitions should account for the potential impact of these transactions on their Pillar Two profiles.

- Include new Notification filings into compliance systems and monitoring.

For additional information concerning this Alert, please contact:

EY Tax Indonesia, Jakarta (Indonesia)

- Bambang Suprijanto

- Ihsan Muttaqien

- Peter Mitchell, Jakarta

- Ben Koesmoeljana

- Peter S Ng

Ernst & Young LLP (United States), Indonesia Tax Desk, Chicago

- Ibnu Aryo Baskoro

Ernst & Young LLP (United States), ASEAN Tax Desk, New York

- Bee-Khun Yap

Ernst & Young LLP (United States), Asia Pacific Business Group, New York

- Gagan Malik

- Dhara Sampat

Ernst & Young LLP (United States), Asia Pacific Business Group, Chicago

- Pongpat Kitsanayothin

Published by NTD’s Tax Technical Knowledge Services group; Carolyn Wright, legal editor

For a full listing of contacts and email addresses, please click on the Tax News Update: Global Edition (GTNU) version of this Alert.