EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

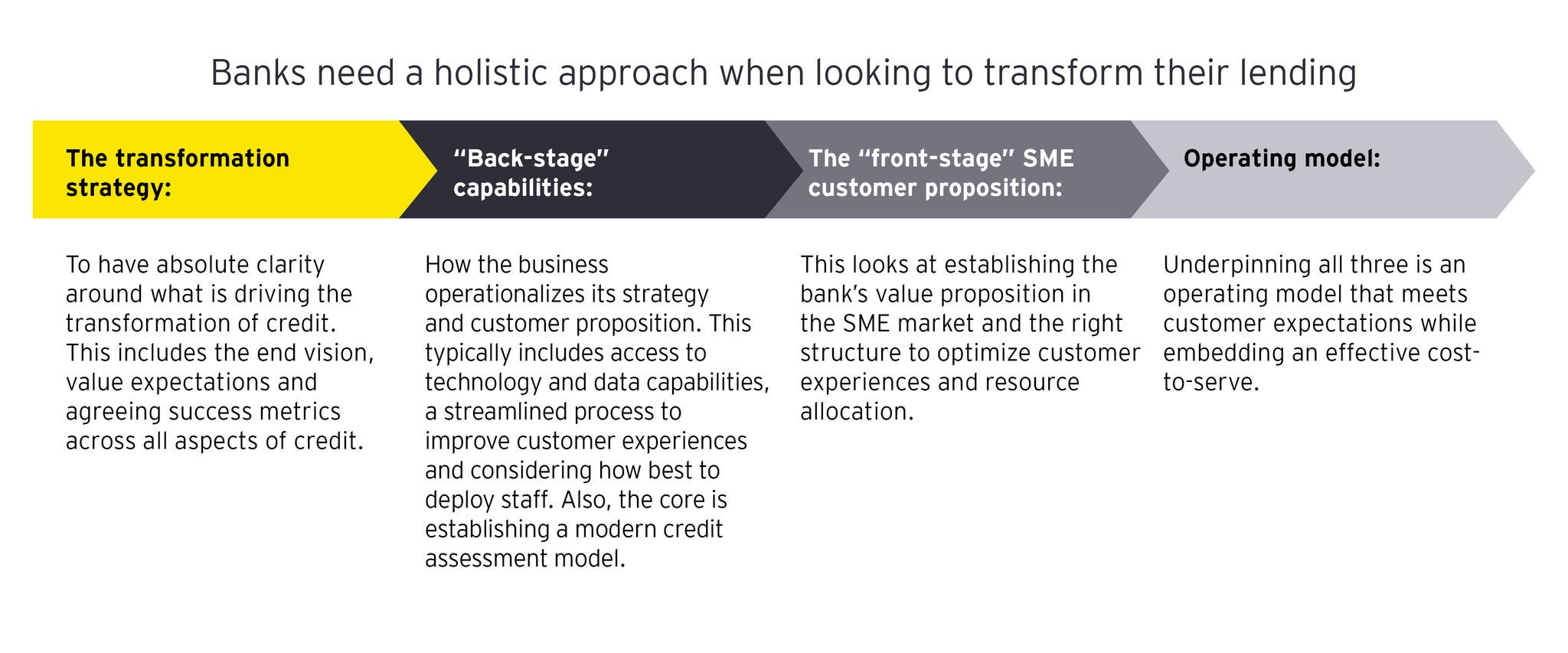

-

Our payments professionals can help your business enhance innovation, drive growth and improve performance. Find out more.

Read more

Decreasing revenues and operating margins

Banks can no longer rely only on cost optimization for profitability. They need to focus on generating new revenue. Corporate banks are increasingly realizing the revenue potential from the SME sector (particularly the middle-market clients), especially if they can simplify the lending process through extensive digitalization and automation.

A standing start

As banks look to react to the opportunities around lending, they will have to overcome some significant existing barriers in their current systems and processes:

Slow process

Some lenders continue to rely on employees to review and manually enter information from physical documents such as financial and payroll statements. This is something that could be easily automated to be faster and cheaper.

Poor user experience

Banks require a wide variety of documents, often in paper form and in different tranches, compromising the customer experience. SMEs would prefer a simpler credit process, using standardization and more user-friendly technologies.

Lack of data-driven processes

Given the unique characteristics of each SME, banks find it difficult to assess creditworthiness, depending on detailed commercial plans, profit and loss sheets, or financial forecasts. That can lead to an increase in default risk. Today, lenders can enhance credit models by using real-time data and alternative data sources.

Low understanding of SME business

Lenders are often not meeting the needs of SMEs – products are not attractive enough and lack customization. Banks can use more data from new regulations, such as Payment Services Directive Two (PSD2), and leverage open banking to obtain detailed credit data. They can then analyze and adapt their offerings as needed.