EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Canada | Prince Edward Island budget 2025-26

- On 10 April 2025, the Prince Edward Island budget was tabled and included tax measures affecting corporations and individuals.

- The budget proposed to decrease the provincial general corporate income tax rate from 16% to 15% and increase the CA$500,000 small-business limit to CA$600,000, effective 1 July 2025.

- The budget also included a proposed increase in the provincial personal income tax brackets of 1.8% and increases to certain personal tax credits.

On 10 April 2025, Prince Edward Island Finance Minister and Chair of Treasury Board Jill Burridge tabled the province's fiscal 2025-26 budget. The budget contains tax measures affecting corporations and individuals.

The minister anticipates a deficit of CA$166.3m for 2024-25 and projects a deficit of CA$183.9m for 2025-26, followed by further deficits for each of the next two years (CA$167.8m for 2026-27 and CA$119.5m for 2027-28). The projected 2025-26 deficit includes a CA$32m tariff and trade contingency fund to provide direct support to businesses and workers affected by tariffs, reinforce trade relationships and help Prince Edward Island businesses diversify into new markets (an additional CA$10m tariff working capital program will also provide financial relief through flexible loans).

Following is a brief summary of the key tax measures.

Business tax measures

Corporate income tax rates

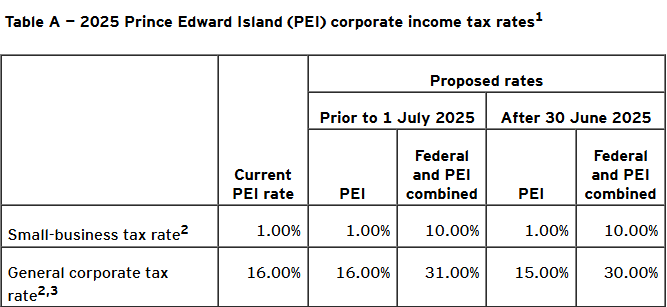

Effective 1 July 2025, the budget proposes to decrease the general corporate income tax rate from 16% to 15% and increase the CA$500,000 small-business limit to CA$600,000. The small-business corporate income tax rate will remain at 1%.

Prince Edward Island's current and proposed 2025 corporate income tax rates are summarized in Table A.

1 The rates represent calendar-year-end rates unless otherwise indicated.

2 The federal corporate income tax rates for manufacturers of qualifying zero-emission technology are reduced to 7.5% for eligible income otherwise subject to the 15% federal general corporate income tax rate or 4.5% for eligible income otherwise subject to the 9% federal small-business corporate income tax rate. These reductions are not reflected in the combined federal and Prince Edward Island rates above.

3 An additional tax applies to banks and life insurers at a rate of 1.5% on taxable income (subject to a CA$100m exemption to be shared by group members).

Personal tax

Personal income tax rates

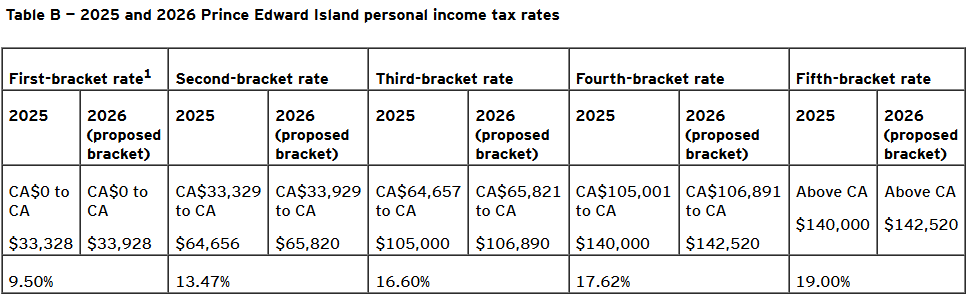

The budget does not include any changes to personal income tax rates. However, the minister proposes to increase the five tax brackets by 1.8% for 2026.

The 2025 and 2026 Prince Edward Island personal income tax rates are summarized in Table B.

1 Individuals resident in Prince Edward Island on 31 December 2025 with taxable income up to CA$17,934 pay no provincial income tax as a result of a low-income tax reduction. The low-income tax reduction is clawed back for income exceeding CA$22,250 until the reduction is eliminated, resulting in an additional 5% of provincial tax on income between CA$22,251 and CA$29,250.

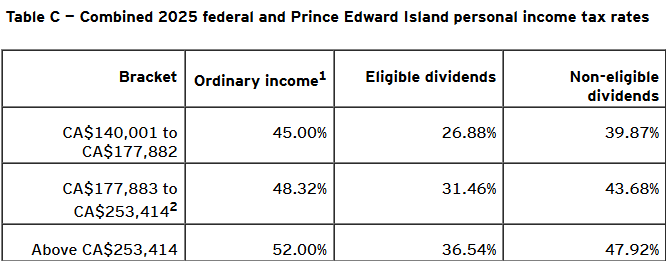

For taxable income exceeding CA$140,000, the 2025 combined federal-Prince Edward Island personal income tax rates are outlined in Table C.

1 The rate on capital gains is one-half the ordinary income tax rate.

2 The federal basic personal amount comprises two elements: the base amount (CA$14,538 for 2025) and an additional amount (CA$1,591 for 2025). The additional amount is reduced for individuals with net income exceeding CA$177,882 and is fully eliminated for individuals with net income exceeding CA$253,414. Consequently, the additional amount is clawed back on net income exceeding CA$177,882 until the additional tax credit of CA$239 is eliminated; this results in additional federal income tax (e.g., 0.32% on ordinary income) on net income between CA$177,883 and CA$253,414.

Personal tax credits

This budget proposes changes to the following personal credits/amounts:

- Basic personal amount — Increase in the basic personal amount from CA$14,250 to CA$14,650 and to CA$15,000 for 2025 and 2026, respectively

- Low-income tax reduction — Similar CA$400 and CA$350 increases in the income threshold for the low-income tax reduction to CA$22,650 and to CA$23,000 for 2025 and 2026, respectively

- Spousal and equivalent amounts — Increase in the spouse or common-law partner amount, as well as in the amount for an eligible dependent, from CA$12,103 to CA$12,443 for 2025 and to CA$12,740 for 2026, and increase in the related income threshold from CA$1,210 to CA$1,244 for 2025 and to CA$1,274 for 2026

Other tax measures

Tobacco tax

The budget proposes to increase the tobacco tax rate per cigarette from CA$0.2952 to CA$0.3000, effective 28 April 2025.

Real property transfer tax

The budget proposes to increase the real property transfer tax rate from 1% to 2% once a CA$1m threshold is reached, effective 28 April 2025. Although no further details are provided in the budget, it is presumed that the 2% rate will apply where the amount subject to the tax (i.e., the greater of the consideration for the transfer of a real property or its assessed value) is CA$1m or higher.

It is also proposed that the current first-time-homebuyers exemption from the tax will not apply where the consideration or the assessed value is equal to or above the CA$1m threshold. The new 2% rate will apply.

For additional information concerning this Alert, please contact:

Ernst & Young LLP (Canada), Toronto

- Linda Tang

- Mark Kaplan

- Phil Halvorson

- Terri McDowell

- Trevor O'Brien

- Leslie Ivany

Ernst & Young LLP (Canada), Quebec and Atlantic Canada

- Albert Anelli

- Angelo Nikolakakis

- Brian Mustard

- Nicolas Legault

- Nik Diksic

- Philippe-Antoine Morin

- Joannie Ethier

Ernst & Young LLP (Canada), Prairies

- Mark Coleman

- Liza Mathew

Ernst & Young LLP (Canada), Vancouver

- Eric Bretsen

For a full listing of contacts and email addresses, please click on the Tax News Update: Global Edition (GTNU) version of this Alert.

Published by NTD’s Tax Technical Knowledge Services group; Carolyn Wright, legal editor