EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Executive summary

o

n 20 December 2021, the Organisation for Economic Co-operation and Development (OECD) released the Pillar Two Model Rules as approved by the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS). The Model Rules define the scope and key mechanics for the Pillar Two system of global minimum tax rules, which includes the Income Inclusion Rule (IIR) and the Under Taxed Payments Rule (UTPR), referred to collectively as the “GloBE rules.”

Together with the Model Rules, the OECD also released a summary of the rules (The Pillar Two Model Rules in a Nutshell), an overview of the key operating provisions of the GloBE rules (Fact Sheets) and a Frequently Asked Questions document.

According to the timeline released in October with agreement of member jurisdictions of the Inclusive Framework, the Pillar Two rules should be brought into domestic law in 2022 to be effective in 2023, with the exception of the UTPR which is to enter into effect in 2024. The GloBE rules are designed as a common approach, which means that Inclusive Framework members are not required to adopt the GloBE rules but if they choose to do so, they should implement and administer the rules in a way that is consistent with the Model Rules. Inclusive Framework members are also required to accept the application of the GloBE rules by other Inclusive Framework members.

The OECD press release indicates that it expects to release the Commentary relating to the Model Rules and to address the interaction with the United States (US) Global Intangible Low-Taxed Income (GILTI) rules in early 2022. In addition, the Inclusive Framework is developing the model treaty provision for the Subject to Tax Rule (STTR), which is the third element of the Pillar Two global minimum tax framework, and a multilateral instrument for its implementation, which the OECD expects to release in the early part of 2022 with a public consultation event on it to be held in March 2022. Finally, the OECD notes the work to be done on development of an implementation framework addressing administration, compliance and coordination matters related to Pillar Two and announces that a public consultation event on the implementation framework will be held in February 2022.

On 22 December, the European Commission is expected to publish a proposal for a European Union (EU) Directive to require implementation of the GloBE rules across all EU Member States. It is expected that the Model Rules will be reflected in the proposed Directive with some modifications in light of EU law requirements.

Background

Building on its earlier work on BEPS that culminated in the issuance in 2015 of final reports on 15 action areas, the OECD in 2019 began a new project focused on addressing the tax challenges of the digitalization of the economy. The current project, referred to as BEPS 2.0, is being conducted through the OECD/G20 Inclusive Framework, which now has 141 participating jurisdictions.

In January 2019, the OECD released a Policy Note communicating that renewed international discussions would focus on two central pillars: one pillar addressing the broader challenges of the digitalization of the economy and focusing on the allocation of taxing rights, and a second pillar addressing remaining BEPS concerns.1 In February 2019, the OECD released a Public Consultation Document2 describing the two-pillar proposals at a high level. The OECD received extensive comments from stakeholders and held a public consultation in March 2019.3

Following the public consultation, in May 2019, the OECD released the “Programme of Work to Develop a Consensus Solution to the Tax Challenges Arising from the Digitalisation of the Economy,” reflecting the two pillars:4

- Pillar One on development of new nexus and profit allocation rules to assign more taxing rights to market countries

- Pillar Two on development of new global minimum tax rules

On 8 November 2019, the OECD released a Consultation Document on Pillar Two5 and on 9 December 2019 the OECD hosted a consultation meeting to give stakeholders an opportunity to discuss their comments with the Inclusive Framework jurisdictions.6

On 31 January 2020, the OECD released a Statement by the Inclusive Framework on the two-pillar approach indicating that the members of the Inclusive Framework affirmed their commitment to reach an agreement on new international tax rules by the end of 2020.7 Attached to the Statement were more detailed documents, including a progress update on Pillar Two.

In October 2020, the OECD released a series of documents with respect to the BEPS 2.0 project, including a detailed Blueprint on Pillar Two.8 In the Cover Statement, the Inclusive Framework expressed the view that while no agreement had been reached yet, the Blueprint provided for a solid basis for future agreement. In January 2021, the OECD hosted a virtual consultation session with stakeholders on the voluminous comments that were submitted on the Blueprints on both Pillar One and Pillar Two.9

On 1 July 2021, the OECD released a Statement on a Two-Pillar Solution to Address the Tax Challenges Arising from the Digitalisation of the Economy (July Statement), reflecting the agreement of 130 of the member jurisdictions of the Inclusive Framework on some key parameters with respect to both pillars.10 At that time, nine members of the Inclusive Framework (Barbados, Estonia, Hungary, Ireland, Kenya, Nigeria, Peru, Saint Vincent and the Grenadines, and Sri Lanka) did not join the July Statement. Barbados, Peru and Saint Vincent and the Grenadines subsequently joined the agreement. At the end of August 2021, Togo joined both the Inclusive Framework and the July Statement.

In October 2021, the OECD published a Statement indicating that the Inclusive Framework agreed on a two-pillar solution to address the tax challenges arising from the digitalization of the economy and providing a timeline for implementation.11 136 jurisdictions of the Inclusive Framework agreed to the Statement. Estonia, Hungary and Ireland, which did not join the July agreement, joined the October Statement. Pakistan, which joined the July statement, did not join the October Statement. Kenya, Nigeria, and Sri Lanka did not join either statement. Mauritania has since become a member of the Inclusive Framework and joined the October Statement, bringing to 137 the total number of jurisdictions participating in the agreement.

Detailed discussion

Pillar Two introduces new global minimum tax rules for multinational enterprises (MNEs) with an agreed rate of 15%. The minimum tax is calculated based on financial accounting standards and relies on two main components: profits and taxes paid. Generally, the rules apply to MNE groups with an annual revenue of €750 million or more.

Pillar Two includes two interlocking rules that together comprise the GloBE rules: i) the IIR, which imposes top-up tax on a parent entity with respect to a low-taxed foreign subsidiary; and ii) the UTPR, which imposes top-up tax through a denial of deductions or other adjustment if the low-taxed income of an entity in the MNE group is not subject to top-up tax under an IIR. Pillar Two also includes the STTR, which is a treaty-based rule that allows source jurisdictions to impose withholding tax on certain related party payments that are subject to tax below a minimum rate.

On 20 December 2021, the OECD released the Pillar Two Model Rules as approved by the Inclusive Framework. The Model Rules define scope and mechanics for the GloBE rules and contain 10 chapters:

Chapter 1 defines the scope of the GloBE rules.

Chapter 2 describes the application of the IIR and UTPR and how to allocate the top-up tax.

Chapter 3 determines the income or loss for the period for each company in the MNE group. This is the first component of the effective tax rate (ETR) calculation.

Chapter 4 identifies the taxes attributable to each company in the MNE group. This is the second component of the ETR calculation.

Chapter 5 provides the rules for determining the ETR for a jurisdiction and the top-up tax for constituent entities located in low-tax jurisdictions.

Chapter 6 contains rules relating to acquisitions, disposals and joint ventures.

Chapter 7 describes the application of the GloBE rules to tax neutrality and distribution regimes.

Chapter 8 addresses administrative aspects of the GloBE rules, including information filing requirements and safe harbors.

Chapter 9 sets out transitional rules.

Chapter 10 sets out defined terms and concepts used elsewhere in the Model Rules.

Chapter 1 – Scope

Chapter 1 provides the rules for determining the MNE Groups that are in scope of the GloBE rules. It also provides scope exclusions for specified investment-type entities and organizations with special status in their residence jurisdiction.

In scope

Generally, an MNE Group and its Constituent Entities are in scope of the GloBE rules if the annual revenue in the Consolidated Financial Statements of the Ultimate Parent Entity (UPE) is €750 million or more for two out of the four Fiscal Years immediately preceding the tested Fiscal Year. Although not specified in the Model Rules, the October Statement provides that jurisdictions are free to apply the IIR to groups headquartered in their jurisdictions without regard to the threshold.

For this purpose, an MNE Group is a Group that consists of entities located in more than one jurisdiction. A Group is a collection of Entities (i.e., legal persons or arrangements that prepare separate financial accounts) that are related through ownership or control and that either are:

Included in the Consolidated Financial Statements of the UPE

Excluded from such statements solely on size or materiality grounds or because the Entity is held for sale

In addition, a stand-alone entity (Main Entity) is considered an MNE Group if it has at least one Permanent Establishment located in another jurisdiction.

A Constituent Entity is an Entity included in a Group or a Permanent Establishment of a Main Entity.

The UPE is the Entity that is at the top of the ownership control chain and that is not owned by another Entity.

Consolidated Financial Statements are financial statements that: (i) are prepared in accordance with International Financial Reporting Standards (IFRS) or the generally accepted accounting principles (GAAP) of a specified country; (ii) are not prepared in line with such a standard but reflect adjustments of items and transactions to prevent any divergences from IFRS of more than €75 million; or (iii) would have been prepared if the Entity were required to prepare statements in accordance with IFRS or a specified GAAP.

Excluded Entities

The Model Rules provide exclusions from the GloBE rules for specified Entities. However, such entities are not excluded for purposes of determining the MNE Group or whether the MNE Group meets the revenue threshold for being in scope of the GloBE rules.

Entities that are excluded regardless of whether they are a UPE are:

Governmental Entities12

International Organizations13

Non-Profit Organizations14

Pension Funds15

Entities that are excluded only if they are the UPE of an MNE Group are:

Investments Funds16

Real Estate Investment Vehicles17

Entities that are owned by one or more of the Excluded Entities listed above also are excluded if specified ownership thresholds and activity conditions are satisfied.

An election is available to not treat an Entity as an Excluded Entity, subject to a five-year consistency requirement.

Chapter 2 – Charging provisions

Chapter 2 provides rules for determining which entity is liable to any top-up tax and the portion of such top-up tax that is charged to such entity. Specifically, it sets out the mechanics of the IIR and the UTPR.

Mechanics of the IIR

The IIR requires a Parent Entity to pay its Allocable Share of the Top-up Tax with respect to a Low-Taxed Constituent Entity. The IIR includes an ordering rule that operates through a top-down approach, starting with the UPE. If the UPE is not located in a jurisdiction that has implemented the IIR, the highest Parent Entity in the ownership chain that is located in a jurisdiction that has implemented the IIR pays its Allocable Share of the Top-up Tax. A specific rule limits the application of the IIR to Low-Taxed Constituent Entities outside a Parent Entity's jurisdiction.

An exception to the top-down approach applies in split-ownership situations. A Partially-Owned Parent Entity applies the IIR in priority over its controlling Parent. This ensures that the income of a Low-Taxed Constituent Entity is subject to the IIR without requiring a Parent to apply the IIR with respect to income that it does not entirely own.

A Parent Entity’s Allocable Share of the Top-up Tax under the IIR is based on its Inclusion Ratio, which is effectively determined based on the Parent Entity's ownership in the Low-Taxed Constituent Entity. If the Parent Entity directly (or indirectly) owns 100% of such entity, its Inclusion Ratio for that entity generally is 100%. In a split-ownership situation, the Inclusion Ratio is determined on a pro-rata basis.

An IIR offset mechanism applies in situations where multiple entities in the chain apply the IIR with respect to a Low-Taxed Constituent Entity. For example, this may be the case if a Partially-Owned Parent Entity is held by two Parents, only one of which applies a Qualified IIR. In such case, the UPE that applies the IIR is required to reduce its allocable share of Top-Up Tax by an amount equal to its share of Top-up Tax imposed at the level of the Partially-Owned Parent Entity.

Mechanics of the UTPR

Under the UTPR, Constituent Entities are denied a deduction (or required to make an equivalent adjustment) resulting in an additional cash tax expense for the amount of the UTPR Top-up Tax allocated to that jurisdiction. This adjustment is applied to the extent possible for the taxable year. If the adjustment is insufficient to cover the full amount of the UTPR Top-up Tax for that year, the difference is carried forward for application in a succeeding taxable year.

The total UTPR Top-up Tax amount is determined using similar mechanics as the IIR. One notable difference between the IIR and the UTPR is that the UTPR does not provide a limitation to Low-Taxed Constituent Entities outside the UTPR jurisdiction. The total UTPR Top-up Tax amount is equal to the Top-up Tax calculated for each Low-taxed Constituent Entity (subject to certain adjustments). However, the Top-up Tax of a Low-Taxed Constituent Entity allocated under the UTPR is reduced by the Top-up Tax that is brought into charge under a Qualified IIR. In many cases this will mean that the UTPR does not result in additional Top-up Tax, unless the ETR in the IIR jurisdiction itself is below 15%.

The amount of UTPR Top-Up Tax that is allocated to a UTPR jurisdiction is calculated by multiplying the total UTPR Top-Up Tax amount by the jurisdiction’s UTPR Percentage. A jurisdiction’s UTPR Percentage is determined on the basis of two factors that reflect the relative substance of the MNE Group in each of the UTPR jurisdictions, with each factor given equal weight:

The Employee factor is the number of Employees in the UTPR jurisdiction relative to the total for all UTPR jurisdictions.

The Tangible Assets factor is the Net Book Value of the Tangible Assets in the UTPR jurisdiction relative to the total for all UTPR jurisdictions.

Based on a specific carve-out rule, a jurisdiction is excluded from this calculation if a UTPR Top-up Tax amount allocated to that jurisdiction in the previous year did not result in a corresponding additional cash tax expense. The next year's UTPR Percentage for such a jurisdiction is deemed to be zero and the employees and tangible assets of the Constituent Entities located in such jurisdiction are excluded from the calculation (unless all jurisdictions have a UTPR Percentage of zero, in which case this rule does not apply).

Chapter 3 - Computation of GloBE Income or Loss

Chapter 3 provides the rules for computing the GloBE income or loss of each Constituent Entity. This computation is a central element of the GloBE rules and plays an important role in the ETR calculation. Financial accounting net income or loss (determined under an acceptable accounting standard) is the starting point for the computation, which is then adjusted under the rules described in the Chapter.

Globe Income or Loss

The computation of the GloBE Income or Loss starts with net income or loss used in preparing the consolidated financial statements of the UPE, before any consolidation adjustments eliminating intra-group transactions, determined based on the accounting standard used by the UPE in such statements.

However, a different accounting standard may be used if the following conditions are all met:

The financial accounts of the Constituent Entity are maintained based on that accounting standard

The information contained in such financial accounts is reliable

Permanent differences in excess of €1 million are conformed to the UPE’s accounting standard.

To get from this starting point to GloBE Income or Loss, adjustments are required for:

The net amount of certain tax expense (including tax credits)

Excluded Dividends

Excluded Equity Gains or Losses

Included Revaluation Method Gains or Losses

Gains or Losses from Disposition of Certain Assets and Liabilities

Asymmetric Foreign Currency Gains or Losses

Policy Disallowed Expenses

Prior Period Errors and Changes in Accounting Principles

Accrued Pension Expense

For the purpose of computing GloBE Income or Loss, the Filing Constituent Entity may elect to substitute the deduction of stock-based compensation allowed for local tax purposes for the amount that was included in the financial accounts, under specified conditions. The election is applicable for five years and must be applied consistently to all Constituent Entities in the same jurisdiction. Transitional measures apply to the election.

Transactions between Constituent Entities located in different jurisdictions must be consistent with the Arm’s-Length Principle and the same transaction amount needs to be recorded in their respective accounts. A loss from a sale or other transfer of an asset between Constituent Entities within the same jurisdiction must be consistent with the Arm’s Length Principle if it is included in the GloBE income.

In the case of assets and liabilities that are subject to fair value or impairment accounting, the Filing Constituent Entity may elect to assess gains and losses by means of the realization principle for purposes of computing GloBE Income. The election would apply for a mandatory period of five years for all Constituent Entities in the jurisdiction.

An annual election is available to make adjustments, with a four-year look-back period, in the case of an overall aggregate gain derived from the disposition of local tangible assets to third parties by the Constituent Entities in a jurisdiction. The ETR and Top-up Tax, if any, for any previous Fiscal Year must be re-recalculated when applying this election.

The UPE may elect to apply a consolidated accounting treatment (for a mandatory period of five years), to transactions between Constituent Entities in the same jurisdiction that are included in a tax consolidation group, to eliminate income, expenses, gains and losses.

The GloBE Income or Loss of a Low-tax Entity excludes expenses attributable to intragroup financing arrangements that are reasonably anticipated not to be included in the taxable income of a High-tax Counterparty over the expected duration of the arrangement.

Specific rules apply to taxes paid by insurance companies that are charged to policyholders and to equity increases and decreases related to Tier One Capital of regulated entities.

Specific adjustments to Financial Accounting Net Income or Loss are required in the case of corporate restructurings and with respect to distribution regimes.

International Shipping Income

Certain income from international shipping and ancillary activities is excluded from GloBE Income or Loss. Qualifying International Shipping Income relates to the transportation of passengers or cargo in international traffic, including the leasing of a ship on a time charter basis (or on a bareboat basis but only if leased to another Constituent Entity). Ancillary activities are specified activities that are performed primarily in connection with the transportation of passengers or cargo in international traffic. The qualifying net income from ancillary activities of all Constituent Entities in a jurisdiction is capped at 50% of such entity’s qualifying net income from international shipping activities.

In order to qualify for the exclusion, a Constituent Entity must demonstrate that the strategic or commercial management of all ships concerned is effectively carried on from within the jurisdiction where the entity is located.

Allocation to Permanent Establishments

Specific rules apply to allocate GloBE Income or Loss between a Permanent Establishment and its head office (the Main Entity).

For this purpose, a Permanent Establishment includes a place of business: (a) that is treated as a permanent establishment in accordance with an applicable tax treaty and taxed in accordance with a provision similar to Article 7 of the OECD Model Tax Convention on Income and Capital; (b) where the income attributable to it is taxed under a jurisdiction’s domestic tax law on a net basis (this includes a deemed place of business); (c) situated in a jurisdiction that has no corporate tax income system, if it would be treated as a permanent establishment under the OECD Model Tax Convention on Income and Capital and taxed on the income attributable to it under Article 7 of that model; or (d) if not described in (a)-(c), through which operations are conducted outside the jurisdiction of the head office, provided that the jurisdiction exempts the income attributable to those operations.

Generally, the net income as reflected in the separate financial accounts of the Permanent Establishment should be followed. Where separate accounts do not exist, then the net income will be the amounts that would have been reflected if the Permanent Establishment had prepared standalone financials in accordance with the UPE’s accounting standard.

The financial accounts will be adjusted, if necessary, to only reflect the income or loss attributable to the Permanent Establishment based on the applicable tax treaty, domestic law or OECD Model Tax Convention (depending on the type of Permanent Establishment), regardless of the actually taxed income.

The net income or loss of a Permanent Establishment generally will not be included in the GloBE Income or Loss of the Main Entity. There is one exception to this rule: when a Permanent Establishment has a loss that is treated as an expense in the income tax calculation of the Main Entity and is not offset against an item of income subject to tax in both the jurisdiction of the Permanent Establishment and the jurisdiction of the Main Entity. In this situation, a recapture rule will apply to income subsequently arising for the Permanent Establishment.

Allocation to Flow-through Entities

Special rules apply for the allocation of income or loss of Flow-through Entities. A Flow-through Entity is an entity that is tax transparent with respect to its income, expense, profit or loss in the jurisdiction where it is created, unless it is tax resident and subject to covered tax on its income and profit in another jurisdiction. Flow-through Entities also include Reverse Hybrid Entities, which are flow-through entities that are not tax transparent in the jurisdiction of their owner.

The income or loss of these entities is first reduced to account for the ownership interest of entities that are not part of the MNE Group. Then the income or loss is allocated to a Permanent Establishment of the Flow-through Entity if the business is carried out through a Permanent Establishment. The remaining income or loss generally is allocated to its owners in accordance with their ownership interests. The calculation is performed separately for each ownership interest. However, if the Flow-through Entity is the UPE or a Reverse Hybrid Entity, the remaining income is allocated to the UPE or the Reverse Hybrid Entity.

Chapter 4 - Computation of Adjusted Covered Taxes

Chapter 4 identifies the taxes attributable to the GloBE income or loss of each Constituent Entity, the so-called “covered taxes.” This is the second component of the ETR calculation. It includes a definition of covered taxes that applies solely for the purposes of the GloBE rules. It also provides specific rules for the allocation of taxes among the constituent entities and mechanisms to address temporary differences.

The computation of Adjusted Covered Taxes is one of the items that has changed significantly from the Pillar Two Blueprint. The major updates from the Blueprint are the use of the current tax expenses accrued for financial accounting purposes as the basis for the computation and the use of deferred tax accounting to address temporary book-tax differences.

Adjusted Covered Taxes

Adjusted Covered Taxes of a Constituent Entity for a Fiscal Year start with the current tax expense accrued in its Financial Accounting Net Income or Loss with respect to Covered Taxes for the Fiscal Year and is adjusted by the following amounts:

The net amount of its Additions and Reductions to Covered Taxes (described below)

The Total Deferred Tax Adjustment Amount (described below)

Any increase or decrease in Covered Taxes recorded in equity or Other Comprehensive Income relating to GloBE Income or Loss that is subject to tax under local tax rules

The Additions to Covered Taxes of a Constituent Entity is the sum of any amount of:

Covered Taxes accrued as an expense in the profit before taxation in the financial accounts

GloBE Loss Deferred Tax Asset that is used under the GloBE Loss Election (described below)

Covered Taxes paid in the Fiscal Year in relation to an uncertain tax position that has reduced Covered Taxes in a previous Fiscal Year18

Credit or refund of a Qualified Refundable Tax Credit reducing the current tax expense19

The Reductions to Covered Taxes of a Constituent Entity is the sum of any amount of:

Current tax expense with respect to income excluded from the computation of GloBE Income or Loss

Credit or refund in respect of a Non-Qualified Refundable Tax Credit that is not recorded as a reduction to the current tax expense20

Covered Taxes refunded or credited, except for any Qualified Refundable Tax Credit, that were not treated as an adjustment to current tax expense

Current tax expense that relates to an uncertain tax position

Current tax expense that is not expected to be paid within three years of the last day of the Fiscal Year

Definition of Covered Taxes

Covered Taxes means the following four categories of taxes:

Taxes recorded in the financial accounts of a Constituent Entity with respect to its income or profits or its share of the income or profits of a Constituent Entity in which it owns an Ownership Interest

Taxes on distributed profits, deemed profit distributions, and non-business expenses imposed under an Eligible Distribution Tax System

Taxes imposed in lieu of a generally applicable corporate income tax

Taxes levied by reference to retained earnings and corporate equity, including a Tax on multiple components based on income and equity

Top-up Tax accrued under a Qualified IIR or a Qualified Domestic Minimum Top-up Tax is excluded from Covered Taxes. Also excluded are taxes attributable to an adjustment as a result of a Qualified UTPR, a disqualified Refundable Imputation Tax, and taxes paid by an insurance company with respect to returns of policyholders.

Allocation of Covered Taxes

Specific rules are provided for the allocation of Covered Taxes from one Constituent Entity to another in order to match such taxes to the GloBE Income to which they relate:

Covered Taxes of a Permanent Establishment are allocated to the Permanent Establishment

Covered Taxes of a Constituent Entity that is an owner of a Tax Transparent Entity are allocated to the Constituent Entity-owner

Covered Taxes under a Controlled Foreign Company (CFC) Tax Regime are allocated to the CFC

In the case of a Constituent Entity that is a Hybrid Entity, Covered Taxes of the Constituent Entity-owner on income of the Constituent Entity under the fiscal transparency rule are allocated to the Hybrid Entity

Covered Taxes of a Constituent Entity’s direct Constituent Entity-owners on distributions from the Constituent Entity are allocated to the distributing Constituent Entity

In the case of a Constituent Entity that is a CFC or a Hybrid Entity and that applied the rules above, the Covered Taxes allocated to such entity with respect to Passive Income cannot exceed the Top-Up Tax Percentage for the Constituent Entity’s jurisdiction determined without regard to the Covered Taxes incurred on such Passive Income by the Constituent Entity-owner, multiplied by the Passive Income includible under the CFC Tax Regime or fiscal transparency rule.

The purpose of this limitation is to ensure that an ETR on Passive Income of the Constituent Entity is not higher than the 15% minimum rate. If the ETR on the Passive income of the Constituent Entity is higher than the 15% minimum rate, the ETR on other income of the Constituent Entity and on the income of other Constituent Entities in the same jurisdiction will be increased by the allocation rules. In the absence of this limitation, the Top-up Tax on other income of the Constituent Entity or on the income of other Constituent Entities in the same jurisdiction would be decreased.

Mechanism to address temporary differences

The Model Rules address temporary differences through the Total Deferred Tax Adjustment Amount, which starts with the deferred tax expense accrued in the financial accounts with respect to Covered Taxes. The deferred tax expense reflected in the financial accounts is required to be recast at the 15% minimum rate if the applicable tax rate is above the minimum rate. This deferred tax expense amount then is subject to specified exclusions and adjustments.

The following amounts, if any, are excluded from the Total Deferred Tax Adjustment Amount:

Deferred tax expense with respect to items excluded from the computation of GloBE Income or Loss

Deferred tax expense with respect to Disallowed Accruals and Unclaimed Accruals21

A valuation adjustment or accounting recognition adjustment with respect to a deferred tax asset

Deferred tax expense arising from a re-measurement with respect to a change in the applicable domestic tax rate

Deferred tax expense with respect to the generation and use of tax credits

The Total Deferred Tax Adjustment Amount is further adjusted as follows:

Increased by any Disallowed Accrual or Unclaimed Accrual paid during the Fiscal Year

Increased by any Recaptured Deferred Tax Liability determined in a preceding Fiscal Year that has been paid during the Fiscal Year

Reduced by any amount that would be a reduction to the Total Deferred Tax Adjustment Amount due to recognition of a loss deferred tax asset for a current year tax loss, where a loss deferred tax asset has not been recognized because the recognition criteria were not met

A deferred tax asset that has been recorded at a tax rate lower than the 15% minimum rate may be recast with the minimum rate in a Fiscal Year such deferred tax asset is recorded, if a taxpayer can demonstrate that the deferred tax asset is attributable to a GloBE Loss.

A recapture rule applies to any deferred tax liability that does not constitute a Recapture Exception Accrual if it is not paid within five years. The recaptured amount is treated as a reduction to Covered Taxes in the Fiscal Year in which it was originally recorded and the ETR and Top-up Tax for such year are recalculated.

Recapture Exception Accrual means the tax expense accrued attributable to changes in associated deferred tax liabilities, in respect of:

Cost recovery allowances on tangible assets

The cost of a license or similar arrangement from the government for the use of immovable property or exploitation of natural resources that entails significant investment in tangible assets

Research and development expenses

De-commissioning and remediation expenses

Fair value accounting on unrealized net gains

Foreign currency exchange net gains

Insurance reserves and insurance policy deferred acquisition costs

Gain from the sale of tangible property located in the same jurisdiction as the Constituent Entity that are reinvested in tangible property in the same jurisdiction

Additional amounts accrued as a result of accounting principle changes with respect to categories above

The GloBE Loss Election

A Filing Constituent Entity is allowed to make a GloBE Loss Election in lieu of applying the mechanism to address temporary differences. This election is made on a jurisdictional basis.

When the GloBE Loss Election is made, a Filing Constituent Entity calculates the GloBE Loss Deferred Tax Asset for each Fiscal Year with net GloBE Loss in the jurisdiction. The GloBE Loss Deferred Tax Asset is the net GloBE loss in a Fiscal Year multiplied by the 15% minimum rate. The GloBE Loss Deferred Tax Asset for the jurisdiction is carried forward to subsequent Fiscal Years to increase the Covered Taxes for the jurisdiction in a Fiscal Year when it is used.

Post-filing adjustments and tax rate changes

Detailed rules are provided for the treatment of adjustments to Covered Taxes for a previous Fiscal Year recorded in the financial accounts. An increase in Covered Taxes in a jurisdiction is treated as the adjustment of Covered Taxes in the Fiscal Year in which the adjustment is made. On the other hand, a decrease in Covered Taxes in a jurisdiction requires a recalculation of the ETR and Top-up Tax for the previous Fiscal Year when such taxes were included. However, a Filing Constituent Entity may make an annual election to treat an immaterial decrease (i.e., a decrease of less than €1 million for the jurisdiction) as an adjustment of Covered Taxes in a Fiscal Year in which such adjustment is made.

Detailed rules also are provided for the treatment of changes in the domestic tax rate. The deferred tax expense resulting from a decrease in the applicable domestic tax rate is treated as an adjustment to a Constituent Entity’s liability for Covered Taxes for a previous Fiscal Year if such decrease results in a rate that is less than the minimum tax rate. On the other hand, the deferred tax expense, when paid, that has resulted from an increase in the applicable domestic tax rate is treated as an adjustment to a Constituent Entity’s liability for Covered Taxes for a previous Fiscal Year if such amount was originally recorded at a rate less than the 15% minimum rate, and the adjustment is limited to an increase up to the deferred tax expense recast by the minimum rate.

If more than €1 million of the amount accrued by a Constituent Entity as current tax expense and included in Adjusted Covered Taxes for a Fiscal Year is not paid within three years after the end of the Fiscal Year, the ETR and Top-Up Tax for such Fiscal Year must be recalculated by excluding such unpaid amounts.

Chapter 5 - Computation of Effective Tax Rate and Top-up Tax

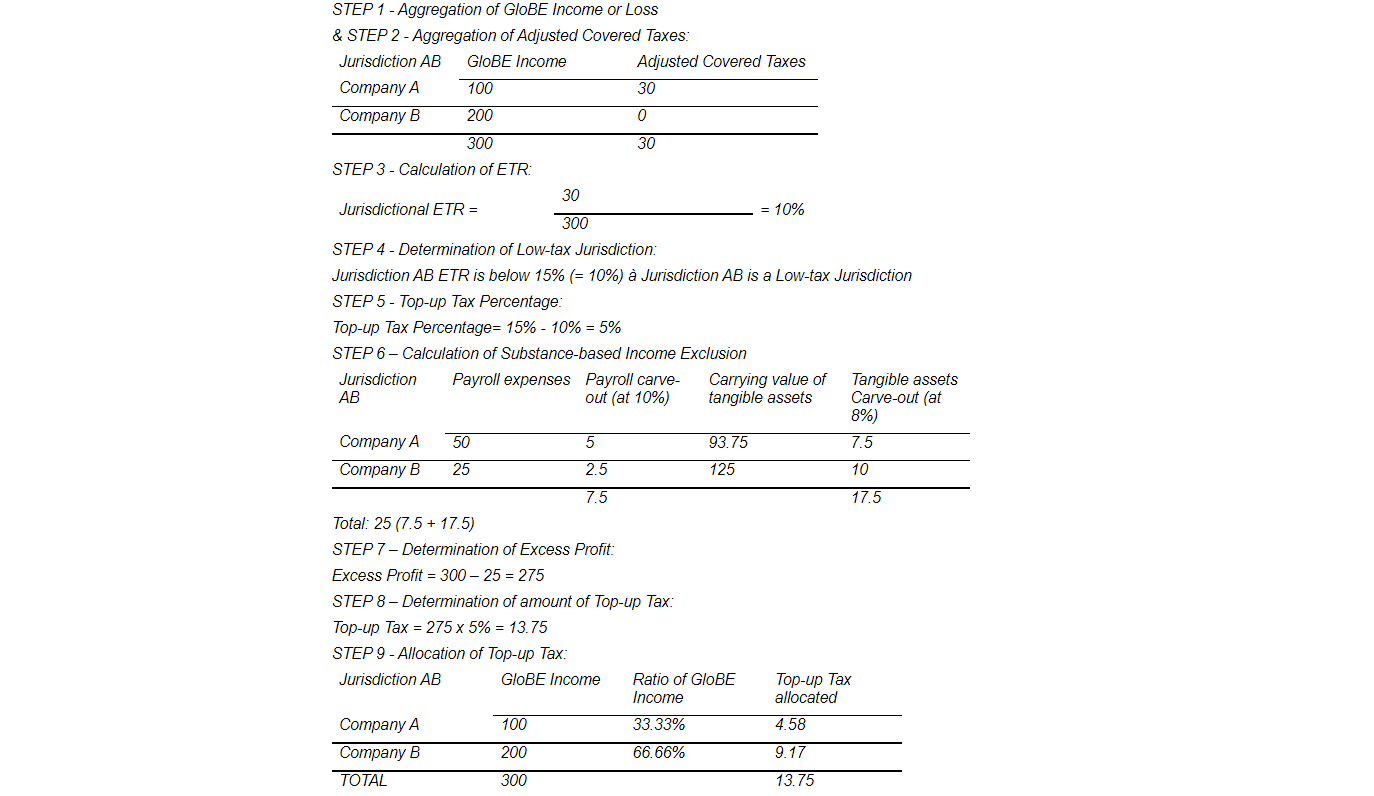

Chapter 5 provides rules for the computation of ETR and Top-up Tax, using a nine-step methodology:

Step 1: Aggregating each Constituent Entity’s GloBE Income or Loss with those of other Constituent Entities located in the same jurisdiction

Step 2: Aggregating each Constituent Entity’s Adjusted Covered Taxes with those of other Constituent Entities located in the same jurisdiction

Step 3: Dividing the jurisdictional aggregated Adjusted Covered Taxes with the aggregated GloBE Income or Loss to determine an Effective Tax Rate for the jurisdiction

Step 4: Identifying which jurisdiction is a Low-Tax Jurisdiction (i.e., has an ETR that is below the 15% minimum rate)

Step 5: Computing a jurisdictional Top-Up Tax Percentage for each Low-Tax Jurisdiction (equal to the positive difference between the minimum rate and the jurisdictional ETR)

Step 6: Calculation of the Substance based Income Exclusion

Step 7: Determination of the Excess Profits in that jurisdiction, by reducing the Net GloBE Income in the Low-Tax Jurisdiction by the Substance-based Income Exclusion

Step 8: Determining the Top-up Tax; and finally

Step 9: Allocating such Top-up Taxes to the Constituent Entities in the Low-Tax Jurisdiction

An example is provided below to illustrate these steps.

Chapter 5 also includes a de minimis exclusion and special rules for calculating the ETR in respect of Minority-Owned Parent Entities.

Determination of ETR

The jurisdictional ETR of the MNE Group for each jurisdiction is:

The Net GloBE Income of a jurisdiction for a Fiscal Year is the positive amount, if any, resulting from:

GloBE Income of all Constituent Entities in the jurisdiction - GloBE Losses of all Constituent Entities in the jurisdiction

Adjusted Covered Taxes and GloBE Income or Loss of Investment Entities are excluded from the determination of the jurisdictional ETR and the determination of Net GloBE Income.

Top-up Tax

The starting point for the calculation of the Top-up Tax due for a Constituent Entity is the determination the Top-up Tax Percentage for a jurisdiction for a Fiscal Year, which is the positive percentage point difference, if any, between the 15% minimum rate and the ETR.

This percentage is applied to the Excess Profit for the jurisdiction for the Fiscal Year, which is the excess, if any, of the Net GloBE Income over the Substance-based Income Exclusion. The Substance-based Income Exclusion refers to the Payroll Carve-out and the Tangible Asset Carve-Out, described below.

Finally, the Jurisdictional Top-up Tax for a jurisdiction for a Fiscal Year is the sum of (i) the Top-up Tax Percentage multiplied by the Excess Profit, increased by (ii) the Additional Current Top-up Tax and reduced by (iii) the Domestic Top up Tax.

The Additional Current Top-up Tax is (i) the amount of additional tax due because of an adjustment of the ETR of a prior year, or (ii) for situations where there is no Net GloBE income, but where the Adjusted Covered Taxes are less than zero and less than the amount of Expected Adjusted Covered Taxes (i.e., the GloBE Income or Loss multiplied by the 15% minimum rate), the difference between Adjusted Covered Taxes and Expected Adjusted Covered Taxes.

The Domestic Top-up Tax is the amount payable under a Qualified Domestic Minimum Top-Up Tax of the jurisdiction for the Fiscal Year. Qualified Domestic Minimum Top-Up Tax refers to a minimum tax regime that is implemented in the legislation of a jurisdiction and that mimics the impact of the GloBE top-up tax on domestic companies.

Finally, the Top-up Tax is allocated to each Constituent Entity of a jurisdiction that has GloBE Income based on the ratio of that Constituent Entity’s GloBE Income over the Aggregate GloBE Income of all Constituent Entities in that jurisdiction.

Substance-based Income Exclusion

The Substance-based Income Exclusion for a jurisdiction reduces the Net GloBE income in order to determine the Excess Profit, which is taken into account for purposes of computing the Top-up Tax. An annual election is available not to apply this exclusion.

The Substance-based Income Exclusion amount for a jurisdiction is the sum of the Payroll Carve-out and the Tangible Asset Carve-out for each Constituent Entity (other than Investment Entities) in that jurisdiction.

The Payroll Carve-Out for a Constituent Entity located in a jurisdiction is equal to 5% of its Eligible Payroll Costs of Eligible Employees that perform activities for the MNE Group in such jurisdiction, other than Eligible Payroll costs that are:

Capitalized and included in the carrying value of Eligible Tangible Assets

Attributable to excluded International Shipping Income and Qualified Ancillary International Shipping Income

The Tangible Asset Carve-Out for a Constituent Entity located in a jurisdiction is equal to 5% of the carrying value of Eligible Tangible Assets located in such jurisdiction. Eligible Tangible Assets are:

Property, plant, and equipment located in the jurisdiction

Natural resources located in the jurisdiction

A lessee’s right of use of tangible assets located in the jurisdiction

A license or similar arrangement from the government for the use of immovable property or exploitation of natural resources that entails significant investment in tangible assets

The computation of carrying value of Eligible Tangible Assets is based on the average of the carrying value (net of accumulated depreciation, amortization, or depletion and including any amount attributable to capitalization of payroll expense) at the beginning and ending of the Reporting Fiscal Year as recorded for the purposes of preparing the Consolidated Financial Statements of the UPE.

Special rules apply for the computation of the Eligible Payroll Costs and Eligible Tangible Assets of Permanent Establishments and Flow-through Entities.

As was provided in the October Statement, under transition rules, the 5% rate is increased to 10% for the Payroll Carve-out and 8% for the Tangible Asset Carve-out and phased down to 5% over ten years under a specified schedule.

Additional Current Top-up Tax

Rules are provided for situations when the ETR and Top-up Tax for a prior Fiscal Year is required or permitted to be recalculated pursuant to an ETR Adjustment.

De minimis exclusion

Under an annual elective de minimis exclusion, the Top-up Tax for the Constituent Entities located in a jurisdiction is deemed to be zero for a Fiscal Year if:

The Average GloBE Revenue of such jurisdiction is less than €10 million; and

The Average GloBE Income or Loss of such jurisdiction is a loss or is less than €1 million.

To calculate these averages, the GloBE Revenue and the GloBE Income or Loss for the two preceding years are taken into account together with the GloBE Revenue and the GloBE Income or Loss for the current year.

Minority-Owned Constituent Entities

Specific rules apply for a minority-owned subgroup (under which the GloBE rules apply as if it was a separate MNE Group) and for minority-owned Constituent Entities that are not part of a minority-owned subgroup (under which the GloBE rules apply on a stand-alone basis).

Example:

The simplified example below illustrates step-by-step how the computation of the ETR would operate.

Chapter 6 – Corporate Restructurings and Holding Structures

Chapter 6 contains rules relating to certain reorganizations. Relating to the scope rules in Chapter 1, this chapter provides further rules for calculating the consolidated revenue threshold in the case of merger and demerger transactions that took place in the prior four-year period. It also provides special rules for the application of the GloBE rules when assets and liabilities are transferred and when a Constituent Entity enters or leaves an MNE Group during the Fiscal Year. Chapter 6 also brings certain Joint Ventures within the scope of the GloBE rules. Finally, this Chapter sets out how the rules should apply in the context of certain multi-parented MNE Groups.

Application of consolidated revenue threshold to group mergers and demergers

Rules are provided that broadly guide how MNE Groups should take into account the impact of mergers and demergers in the context of the €750 million Consolidated Revenue Threshold for determining whether the GloBE rules apply to the relevant group in a particular Fiscal Year.

The individual revenues (as shown in their Consolidated Financial Statements) of the merging groups for each Fiscal Year prior to the merger are required to be added together. Where the sum of the merging group’s revenues in a particular Fiscal Year is at least €750 million, the merged MNE Group will be considered to have met the consolidated revenue threshold for that income year.

On this basis, when measuring a merged MNE Group’s consolidated revenue for the four previous years, if a merger has taken place in that period, the consolidated revenue for purposes of considering the €750 million threshold in each year leading up to that merger is the sum of the consolidated revenues of each of the merging groups.

A similar approach is taken where a standalone entity merges with another entity or group, but does not itself have Consolidated Financial Statements (due to not being a member of any group) for a year. In such circumstances, an aggregation is required of the revenues shown in the standalone Financial Statements or Consolidated Financial Statements (as relevant), and the combined MNE Group will be deemed to have met the consolidated revenue threshold in relation to a year if the sum of the revenues for that year is at least €750 million.

Finally, a demerged group is treated as meeting the consolidated revenue threshold:

In the first Fiscal Year ending after the demerger, if the demerged group itself had annual revenues of at least €750 million in that year

In the second to fourth Fiscal Years ending after the demerger, if the demerged group had annual revenue of at least €750 million in at least two of the Fiscal Years following the year of demerger

For purposes of these rules, mergers are defined by the creation of common control and demergers are defined by a cessation of consolidation by the same UPE.

Constituent Entities joining and leaving an MNE Group

Modifications apply to the GloBE rules in situations where entities join or leave MNE Groups during a Fiscal Year as a result of transfers of direct or indirect Ownership Interests in the relevant entity.

A joining or leaving entity (the “target entity”) is treated as a member of the MNE Group for the joining or leaving year, if any portion of its assets, liabilities, income, expenses or cash flows are ”included on a line-by-line basis” (i.e., consolidated) in the Consolidated Financial Statements of the UPE in that year. In particular, the MNE Group must only take into account the income and taxes of the target entity that are taken into account in those Consolidated Financial Statements of the UPE.

In addition, the target entity must use its historical carrying value of assets and liabilities in determining its GloBE Income or Loss and Adjusted Covered Taxes. As a result, any step-up or step-down recorded in carrying amounts as a result of an acquisition will be ignored.

Additional clarifications on the interaction with other concepts in the GloBE rules include:

In computing Eligible Payroll Costs, only those payroll costs of the target entity that are reflected in the UPE’s Consolidated Financial Statements may be taken into account

The calculation of the carrying value of the Eligible Tangible Assets of the target entity is apportioned to reflect the period during the relevant Fiscal Year that the target was a member of the MNE Group

Deferred tax assets and liabilities of the target entity (other than the GloBE Loss Deferred Tax Asset) that are transferred to the new MNE Group are required to be treated by the new MNE Group as if it had controlled the target entity when they arose

Where deferred tax liabilities of the target have previously been taken into account in calculating the entity’s Total Deferred Tax Adjustment Amount, the amount shall be treated as having been reversed in the disposing MNE Group, and treated as arising in the acquiring MNE Group. This will effectively reset the five Fiscal Year period in respect of the deferred tax liability in the hands of the acquiring MNE Group.

Where the target entity is a Parent Entity and is a member of two or more different MNE Groups during the relevant acquisition year, it is effectively required to apply the IIR provisions separately for each MNE Group.

Where a jurisdiction in which a target Constituent Entity is located treats the acquisition or disposal of a Controlling Interest in the entity as an acquisition or disposal of the underlying assets and liabilities of the entity and imposes a Covered Tax on such disposal, equivalent treatment is provided under the GloBE rules. This treatment is also extended to certain Tax Transparent Entities.

Transfer of assets and liabilities

Special rules also are provided for situations where assets and liabilities are transferred, including business acquisitions and disposals (i.e., transfers of a going concern). Modifications are required to reflect the impact of these transactions on the computation of GloBE Income or Loss for the disposing and acquiring entities.

The implications of such a transfer differ in three alternative scenarios:

Firstly, as a base case, the disposing entity includes the gain or loss on disposition in the computation of its GloBE Income or Loss, and the acquiring entity determines its GloBE Income or Loss based on the carrying value of assets and liabilities (as determined under the UPE’s accounting standard)

However, if the transfer is part of a GloBE Reorganization, the transfer is effectively disregarded, with the disposing entity disregarding any gain or loss, and the acquiring entity adopting the carrying values from the disposing entity

Finally, if the transfer is part of a GloBE Reorganization and the disposing entity recognizes a Non-qualifying Gain or Loss, such gain or loss is to be recognized by the disposing entity in its GloBE Income or Loss, and corresponding adjustments to the carrying amounts acquired by the acquiring entity are made

For these purposes, a GloBE Reorganization is defined to cover a broad range of transactions where the following criteria are satisfied:

Equity interests are issued as consideration for the transfer

The gain or loss arising to the disposing entity upon the transfer is (wholly or partially) not subject to tax

Under its local tax laws, the acquiring entity effectively inherits the tax basis in the assets from the disposing entity

A Non-qualifying Gain or Loss is defined as the lesser of:

The gain or loss of the disposing entity that is subject to tax in its jurisdiction

The financial accounting gain or loss arising in connection with the relevant GloBE Reorganization

In certain jurisdictions, entities are required or permitted to make fair value adjustments to the tax base of its assets or liabilities. In this regard, an election is available that will allow such entities to:

Reflect such fair value adjustments in the computation of GloBE Income or Loss, either in that Fiscal Year or spread across a five-year period

Use the revised fair values for future calculations of GloBE Income or Loss

Joint Ventures

Associates in which investments are recorded using the equity method are generally not included as Constituent Entities of the MNE Group due to an absence of control, and any profits recorded (and the associated taxes) in respect of such investments are excluded from the calculation under the GloBE rules.

However, a modification to this treatment is provided in the context of certain Joint Ventures and their subsidiaries. For these purposes, Joint Venture is defined as an Entity:

Whose financial results are reported using the equity method in the UPE’s Consolidated Financial Statements

That has at least 50% of its Ownership Interests held directly or indirectly by the UPE

For these purposes, Ownership Interests is defined to mean any equity interest that carries rights to the profits, capital or reserves of an Entity and/or its Permanent Establishments.

The GloBE rules are effectively applied to calculate the Top-Up Tax of the Joint Venture and its JV Subsidiaries as if they were a separate MNE Group, with the Joint Venture as the UPE, subject to specified modifications.

Parent Entities holding a direct or indirect Ownership Interest in a Joint Venture or JV Subsidiary then apply the IIR to their share of the Top-up Tax calculated in respect of the members of the JV Group.

To the extent there is an amount of JV Group Top-up Tax remaining after the respective Parent Entities in the group have applied any Qualified IIRs, the remaining amount is added to the Total UTPR Top-up Tax Amount.

Multi-Parented MNE Groups

Finally, special rules are provided for Multi-Parented MNE Groups, such as dual-listed or stapled structure groups, which would otherwise present unusual difficulties in applying the GloBE rules.

For these purposes, Multi-Parented MNE Group is defined as two or more Groups where both of the following criteria are satisfied:

The UPEs of the Groups enter into a Stapled Structure arrangement or a Dual-listed arrangement

At least one Entity or Permanent Establishment of the combined Group is located in a different jurisdiction than the other Entities of the combined Group

Broadly, such Multi-Parented MNE Groups are treated as a single MNE Group for the purposes of the GloBE rules, and the Consolidated Financial Statements prepared for the combined Multi-Parented MNE Group are utilized for these purposes.

Each of the Parents in the Multi-Parented MNE Group is required to apply the IIR to their allocable share of the Top-up Tax of Low-taxed Constituent Entities and Constituent Entities. Likewise, the UTPR is applied by Constituent Entities in the Multi-Parented MNE Group taking into account the Top-Up Tax of all Low-Taxed Constituent Entities of the wider Multi-Parented MNE Group.

Such Multi-Parented MNE Groups may elect to designate a single entity to file the GloBE Information Return in respect of the combined Multi-Parented MNE Group. If no such election is made, each UPE is required to submit the GloBE Information Return.

Chapter 7 - Tax neutrality and distribution regimes

Chapter 7 covers the application of the GloBE rules to certain tax neutrality and other distribution regimes. More specifically, it provides special rules in relation to UPEs that are subject to a tax neutrality regime (such as a tax transparency regime or a deductible dividend regime). It also provides special rules for certain tax regimes that subject an Entity to tax on its earnings when those earnings are distributed or deemed distributed. Lastly, it provides special rules for controlled lnvestment Entities that seek to preserve the tax neutrality of these Entities without giving rise to any leakage under the GloBE rules.

Special rules are provided for UPEs that are either Flow-Through Entities or subject to a Deductible Dividend Regime.

A Flow-Through Entity is an entity that is fiscally transparent in the jurisdiction where it is located. A Deductible Dividend Regime is a regime that allows a deduction for distributions of profits to owners. UPEs that are Flow-through Entities or are subject to Deductible Dividend Regimes are allowed to exclude GloBE Income attributable to each Ownership Interest22 or Deductible Dividend23 under specified circumstances. The GloBE Income of the UPE can be reduced by the GloBE Income of a holder of an ownership interest or a dividend recipient that is subject to tax on such income at a nominal rate equal to or higher than the 15% minimum rate. Additionally, the UPEs can exclude income that is attributable to interests of natural persons or Government Entities, International Organizations, Non-Profit Organizations or Pension Funds that are resident in the UPE jurisdiction and hold 5% or less of the profits and assets of the UPE. Flow-through Entity UPEs must reduce their GloBE Loss by the amount of GloBE Loss attributable to each Ownership Interest unless the holders are not allowed to use the loss in computing their separate taxable income. UPEs that reduce their GloBE Income under these rules must also reduce their Covered Taxes (other than the Taxes for which the dividend deduction is allowed) proportionately to ensure a proper ETR calculation.

An annual election is available with respect to a Constituent Entity subject to an Eligible Distribution Tax System. This is a corporate income tax system that imposes a tax generally payable when the corporation distributes or is deemed to distribute profits to its shareholders or incurs certain non-billable expenses. The system must impose a rate equal to or higher than the 15% minimum rate and must have been in force on or before 1 July 2021. The election can be made by the Filing Constituent Entity and allows the Deemed Distribution Tax to be included in the Adjusted Covered Taxes for the year. The Deemed Distribution Tax is equal to the lesser of the following: (1) the amount of Adjusted Covered Taxes necessary to increase the ETR for the jurisdiction to the Minimum Rate or (2) the amount of tax that would have been due if the entity had distributed all its income. An Annual Deemed Distribution Recapture Account will be established when the election is made to track the extent to which Deemed Distribution Tax is actually paid. A loss on the recapture account would be able to be carried forward for four years and, if not paid, would ultimately be applied as a reduction to the Adjusted Covered Taxes for that fourth year.

Special rules also apply for Investment Entities. Investment Entities are defined as (1) an Investment Fund or a Real Estate Investment Vehicle, (2) an Entity that is at least 95% owned directly by an Investment Fund or a Real Estate Investment Vehicle or through a chain of such entities and operates exclusively or almost exclusively to hold assets or invest funds for the benefit of these Investment Entities or (3) an Entity owned at least 85% by an Investment Fund or a Real Estate Investment Vehicle provided that substantially all its income is Excluded Dividends or Excluded Gain or Loss for the purposes of the GloBE Income or Loss calculation. These rules do not apply to Investment Entities that are Tax Transparent Entities.

The rules aim to ensure that the MNE Group is subject to GloBE with respect only to its allocable share in Investment Entities. A variation of the Substance-based Income Exclusion applies.

Under certain circumstances, a Filing Constituent Entity can elect to treat an Investment Entity as a Tax Transparent Entity for a period of five years. This election is only available if the Constituent Entity that owns the Investment Entity is subject to a mark-to-market tax regime on its ownership interests in the entity a tax rate that equals or exceeds the 15% minimum rate.

A Taxable Distribution Method election is available for a Constituent Entity’s interest in an Investment Entity, if the Constituent Entity is subject to tax on the distributions from the Investment Entity at a rate that is equal or higher than the 15% minimum rate. This is a five-year election.

Chapter 8 – Administration

Chapter 8 addresses certain administrative matters. It sets out an obligation to file a standardized information return (the GloBE Information Return) that will provide tax authorities with the information required to assess the tax liability under the GloBE rules. It also provides for the development of optional safe harbors to reduce the compliance and administrative burden. Finally, it references the future development of agreed administrative rules, guidance and procedures as part of the implementation framework.

The GloBE Information Return

A Constituent Entity subject to GloBE rules located in an implementing jurisdiction must file a Globe Information Return with the local tax administration in a standard template no later than 15 months after the last day of the Reporting Fiscal Year. The return can be filed directly by the Constituent Entity or by a Designated Local Entity located in that same jurisdiction on its behalf.

Under these rules, a Constituent Entity is discharged from its filing obligation when the UPE or a Designated Filing Entity files the GloBE Information Return with another jurisdiction that has an agreement (a Qualifying Competent Authority Agreement) to exchange the return with the tax administration of the Constituent Entity’s jurisdiction. In those cases, a Constituent Entity or a Designated Local Entity located in the implementing jurisdiction shall notify the tax administration where it is located of the identity of the entity that is filing the GloBE Information Return and the jurisdiction in which it is located. This mechanism would allow filing of a single GloBE Information Return covering all Constituent Entities in the MNE Group.

The GloBE Information Return will include the following information concerning the MNE Group:

Identification of the Constituent Entities and their status, including their tax identification numbers, and the jurisdiction in which they are located, as well as the overall corporate structure of the MNE Group

The information required for purposes of computing the ETR for each jurisdiction and the Top-up Tax of each Constituent Entity

The allocation of Top-Up Tax under the IIR and the UTPR Top-Up Tax Amount to each jurisdiction

A record of the elections made in accordance with the relevant provisions of the GloBE rules

Other information that is agreed as part of the implementation framework (which is under development) and is necessary to carry out the administration of the rules

The domestic laws of the implementing jurisdiction with respect to penalties and confidentiality of the returns will apply to the GloBE Information Return.

Safe harbors

In order to limit the compliance and administrative burden associated with the application of the GloBE rules, the Model Rules refer to the development of optional safe harbors under which MNE Groups will not need to undertake the GloBE rules calculations in respect of entities that are likely to be taxed above the 15% minimum rate. If an election is made, the Top-up Tax for that jurisdiction (the safe harbor jurisdiction) will be deemed to be zero for that fiscal year.

The rules also provide tax administrations with a mechanism that allows them to challenge the use of a GloBE safe harbor. In such cases, the tax administration challenging the application of the safe harbor will provide notification, within 36 months after the filing of the GloBE Information Return, of specific facts and circumstances that may have materially affected the eligibility for the safe harbor and will invite the impacted Entities to clarify within six months the effect of those facts and circumstances on the eligibility for that safe harbor. If the entity fails to demonstrate within the response period that those facts and circumstances did not materially affect its eligibility for the safe harbor, the GloBE safe harbor will not be applicable.

Chapter 9 - Transition rules

Chapter 9 sets out transitional rules that apply where an MNE Group enters within the scope of the GloBE rules in a jurisdiction for the first time. It also provides specific rules that modify the percentages to be applied in the calculation of the Substance-based Income Exclusion during the transitional period, an exclusion from the UTPR for MNE Groups that are in the initial phase of their international activity and transitional relief rules for filling obligations.

Tax attributes upon transition

Special rules apply to the tax attributes of a Constituent Entity in the transition period to the GloBE rules.

When determining the ETR for a jurisdiction in a Transition Year (i.e., first Fiscal Year that the MNE Group comes within the scope of the GloBE Rules in respect of that jurisdiction), and for each subsequent year, the MNE Group takes into account all the deferred tax assets and liabilities reflected or disclosed in the financial accounts of all the Constituent Entities in a jurisdiction for the Transition Year. Such deferred tax assets and liabilities must be taken into account at the lower of the 15% minimum rate or the applicable domestic tax rate. Deferred tax assets can be recast at the 15% minimum rate if recorded at a lower rate, provided that the taxpayer demonstrates that the assets are attributable to a GloBE Loss.

Chapter 9 also provides an exclusion from the ETR determination for a jurisdiction in a Transition Year for deferred tax assets arising from items that were excluded from the computation of GloBE Income or Loss when generated in a transaction after 30 November 2021.

In the case of a transfer of assets between Constituent Entities that takes place after 30 November 2021, but before the start of the Transition Year, the basis in the acquired assets (other than inventory) should be the disposing entity's carrying value of the transferred assets upon disposition with the deferred tax assets and liabilities brought into the GloBE rules determined on that basis.

Transition relief for the Substance-based Income Exclusion

When determining the Substance-based Income Exclusion for a jurisdiction, a transition period of 10 years (between 2023 and 2032) is provided, during which the amount excluded will be 8% of the carrying value of tangible assets and 10% of payroll, declining annually for the first six years by 0.2 percentage points, and for the last four years by 0.4 percentage points for tangible assets and by 0.8 percentage points for payroll. After the transition period, the amount excluded will be 5% of the carrying value of payroll and tangible assets.

Exclusion from the UTPR for MNE Groups in the initial phase of international activity

For MNE Groups in the initial phase of their international activity, the Top-Up Tax is reduced to zero. Two criteria must be met for an MNE Group to qualify under this exception:

The MNE group has Constituent Entities in six jurisdictions or fewer

The sum of the Net Book Values of Tangible Assets of all Constituent Entities located in all jurisdictions other than the Reference Jurisdiction does not exceed €50 million

For this purpose, the Reference Jurisdiction of an MNE Group is the jurisdiction where the MNE Group has the highest total value of Tangible Assets for the Fiscal Year in which the MNE Group originally comes within the scope of the GloBE Rules and the total value of Tangible Assets in a jurisdiction is the sum of the Net Book Values of all Tangible Assets of all the Constituent Entities of the MNE Group that are located in that jurisdiction.

This exclusion is available for up to five years, starting the first day of the first Fiscal Year when the MNE Group originally came within the scope of the GloBE Rules. For MNE Groups that are in scope when the GloBE rules come into effect, such starting date is when the UTPR rules come into effect.

There also is an optional provision under which the Reference Jurisdiction of the MNE Group can apply specified rules to the initial phase of the MNE Group's international activity.

Transitional relief for filing obligations

The GloBE Information Return is required to be filed with the tax administration within 18 months after the last day of the Reporting Fiscal Year that is the Transitional Year, instead of the standard deadline of 15 months established in Chapter 8.

Chapter 10 - Definitions

Chapter 10 provides the defined terms used throughout the Model Rules. It also includes rules for determining the location of an Entity and a Permanent Establishment for the purposes of applying the GloBE rules.

Location of an Entity and a Permanent Establishment

The location of an Entity that is not a Flow-through Entity is generally the jurisdiction where it is tax resident. In the case of a dual resident Entity, where there is no resolution after applying the tie-breaker rules under an applicable tax treaty, its location is to be determined as follows:

It is considered to be located in the jurisdiction where it paid the greater amount of Covered Taxes (excluding taxes paid under a CFC regime) for the fiscal year

If the amount of Covered Taxes is the same or zero in both jurisdictions, the Entity is considered to be located in the jurisdiction where it has the greater amount of Substance-based Income Exclusion computed on an entity basis

If the amount of the Substance-based Income Exclusion in both jurisdictions is the same or zero, the Entity is considered a Stateless Constituent Entity, unless it is the UPE of the MNE Group in which case it is considered to be located in the jurisdiction where it was created

A Flow-through Entity is treated as a Stateless Entity unless it is the UPE of the MNE Group or it is required to apply an IIR, in which case it is considered to be located in the jurisdiction where it was created.

The location of a Permanent Establishment generally is the jurisdiction where either:

There is a right to tax the income attributable to it in accordance to the business profit article under the applicable tax treaty

In the absence of an applicable tax treaty, it is subject to net basis taxation based on its business presence

In the absence of such a location, a place of business (including a deemed place of business) is treated as a stateless Permanent Establishment if the jurisdiction where the Main Entity is located exempts the income attributable to operations conducted outside that jurisdiction.

Where an Entity changes its location during the Fiscal Year, its location is considered to be the jurisdiction where it was located at the beginning of that year.

Next steps

According to the implementation plan included in the October Statement, Pillar Two should be brought into law in 2022 and be effective in 2023, with the exception of the UTPR which is scheduled to enter into effect in 2024.

An implementation framework covering administrative matters (e.g., filing obligations, review processes) and safe harbors to facilitate coordinated implementation of the GloBE rules is expected to be released by the end of 2022 at the latest. The OECD plans to host a public consultation event on the implementation matters in February 2022.

A model treaty provision for the STTR supplemented by commentary that explains the purpose and the operation of the rule is expected to be released in early 2022. The OECD plans to host a public consultation event on the STTR in March 2022.

Implications

The Model Rules provide a substantial update to the Pillar Two Blueprint that was released in October 2020. There are some significant changes in the Model Rules relative to the concepts described in the Blueprint so it will be important for companies to review the Model Rules carefully with this in mind. In addition, the Commentary that the OECD expects to release in early 2022 will provide additional information relevant to the interpretation and operation of the Model Rules, making it an essential component of the global minimum tax package. The Commentary will require close attention when released as well.

The Model Rules reveal the complexity of the global minimum tax and the significant investment that will be required by companies that are in scope of the new rules in order to be ready to comply when the rules take effect. In this regard, the Inclusive Framework is working to develop an implementation framework to provide guidance on coordination, administration and compliance matters with respect to the Pillar Two global minimum tax. However, the timeline laid out in the October Statement contemplates that the implementation framework may not be released until the end of 2022, which would be immediately before the anticipated entry into effect in January 2023. The public consultation event that the OECD plans to host in February 2022 may provide some information regarding the administration and compliance mechanisms being considered and will be a valuable opportunity for businesses to share practical perspectives on compliance matters with the OECD and the Inclusive Framework as the framework is being developed. In addition, given the potential timing for release of the implementation framework, businesses may need to start preparing for compliance with the new global minimum tax before the final implementation framework is available.

The Model Rules and the coming Commentary are intended to be used by governments in incorporating the global minimum tax into their domestic tax legislation. Because there may well be variation – potentially substantial – in how different jurisdictions reflect the Model Rules, it will be important for companies to monitor the legislative activity in all relevant jurisdictions. Moreover, the Model Rules and Commentary likely will also be considered by jurisdictions that are evaluating potential changes to their domestic tax architecture in response to the adoption of global minimum tax rules by other jurisdictions. This may include, for example, modifications to their incentives regimes and the possible introduction of domestic Top-up Taxes. Companies should monitor this activity in relevant jurisdictions as well.

The first major legislative proposal with respect to implementation of the new Pillar Two rules is expected be released on 22 December 2021, with the European Commission’s planned publication of a draft Pillar Two Directive for the EU. In addition, there is pending legislative activity in the US involving changes to the existing GILTI rules to bring them more in line with the agreed Pillar Two approach. Legislative activity on Pillar Two is expected to begin shortly in other jurisdictions as well.

The Model Rules reflect consideration of some key points that have been made by business representatives during the public consultations hosted by the OECD in the earlier stages of development of the Pillar Two rules. In particular, the Model Rules include specific provisions allowing deferred tax accounting concepts to be taken into account to address certain book-tax timing difference. This aspect of the Model Rules, and the related elements of the coming Commentary, should be reviewed carefully. The need for predictability and importance of simplification have also been stressed by business stakeholders in Pillar Two discussions, and the OECD has indicated that these matters will be addressed in the implementation framework that is being developed.

Key aspects of the Model Rules that bear continued monitoring as implementation activity in jurisdictions around the world begins include:

Jurisdictions are free to apply the IIR to MNEs headquartered in their jurisdiction even if they do not meet the €750 million revenue threshold in the Model Rules. If jurisdictions follow this approach, companies that have not been subject to country-by-country reporting obligations will be subject to elaborate new reporting obligations with significant tax consequences under such an IIIR. It is therefore important for MNEs that do not meet the revenue threshold in the Model Rules to monitor implementation of the IIR in their home country.

Computation of the GloBE tax base and covered taxes is based on financial accounting rather than tax accounting, but will require multiple adjustments resulting in a new measurement that is not used for any other purpose. For the calculation of adjusted covered taxes, the use of deferred tax accounting in the Model Rules is based on deferred tax expense recorded in the financial accounts, but also requires adjustments, recalculation based on the 15% minimum rate, and potential future recapture. Thus, in order to be able to do the computations required to apply the IIR and the UTPR, companies will need to maintain additional data – including historical data and non-tax data.

In addition to these complexities with the calculation of ETR under the Model Rules, the calculation of the top-up tax also is complex and will require a clear understanding of all the key concepts in the GloBE rules.

Businesses considering mergers and acquisitions will need to analyze the historical consolidated revenue of target entities for prior years to determine the impact on the current year application of the GloBE rules. Note that historical profits in target entities relating to businesses disposed of before the acquisition could cause the merged group to exceed the revenue threshold and be within scope of the GloBE rules.

The Model Rules include a provision that treats transferred deferred tax assets and liabilities as if the acquiring MNE Group controlled the relevant entity when the deferred tax assets and liabilities arose. This may create some issues in situations where the relevant groups apply different accounting standards for the recognition or measurement of deferred tax balances.

The Model Rules reference a new information reporting reform to be used to provide tax authorities with all the data required for the GloBE rules. Businesses will need to collect significant information on an entity and jurisdictional basis in order to prepare the GloBE Information Return. Further reporting requirements may be laid out in the implementation framework that is under development. Some of the necessary data may not be relevant for any other purpose and would be required to be collected and maintained specifically for purposes of the new global minimum tax rules.