EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

In parallel with private equity strategies making headlines over the last 10 years with record-breaking deals and soaring returns, a batch of US and European asset managers have leveraged overall investor appetite toward the asset class and have gone public in 2021, reinforcing the trend that started a decade ago.

Laurent Capolaghi, Partner, Private Equity Leader, EY Luxembourg and Sonia Michel, Senior Associate, EY Luxembourg

What is meant by “listed private equity houses”?

Traditional private equity strategies consist of investing in closed-ended funds which in turn invest in companies that are not listed on a stock exchange. As the industry matures, several private equity houses have been trying to launch semi-open-ended structures and/or have some of their structures listed.

Another trend is the IPO of an asset management boutique, i.e., the entity which manages the assets but does not own them. The performance of these boutique asset managers is thus only indirectly correlated to the capability to create value at the exit of the investments but measured on the amount of management fees that the asset manager will receive over the lifetime of the fund it manages.

As a result, the performance is supposed to be less correlated with the performance of the financial markets and rather predictable considering that the assets under management are held by closed-ended structures. Committed capital is known at fund launch and will remain until the investments are exited, therefore producing stable and recurring cash flows for the company.

A bumpy start for listed private equity houses but the past years have marked a new era

The first private equity firm went public in 1997, but the true boom didn't start until 2007 with three large buyout firms: Blackstone, Fortress and Main Street.

The initial performance of listed private equity firms was rocky - Carlyle and Blackstone's stocks lagged the S&P 500 index between 2007 and 2018, in a context where – at the time – the overall investor appetite for private equity as a strategy was still confidential and the outlook of the financial markets was uncertain.

While other major players tried going public in the early 2010s with mixed results, 2018 marked a turning point as private equity giants made the switch from partnerships to publicly traded corporations with expanded shareholder rights. This came at a time where monetary policy started to be more accommodating and the overall appetite for private equity as an asset class gained traction in the investor community.

The most recent wave of private equity IPOs has been spearheaded by European firms, a full decade after the listing of US private equity giants.

Such increase in market capitalization eventually allowed these shares to be included in indexes and mutual fund portfolios, leading to a positive response from investors and prompting a new wave of private equity firms to consider going public, creating a virtuous cycle for this segment from the end of 2020. 2021 seemed to mark the peak of this sudden appetite with returns significantly outperforming the S&P 500 index.1

The race to grow assets under management and the transparency issue

One of the consequences of the listing is that these firms have rapidly evolved from mainstream public assets into diversified asset managers including public and private assets, exercising management over several funds totaling hundreds of billlons of dollars, in contrast to their unlisted rivals.

According to Pitchbook, listed private equity firms may also be more aggressive in growing their fund size to increase management fees and potential performance fees or carried interest. Between 2015 and 2018, listed companies had an average flagship fund size of $18.9 billion, while unlisted companies belonging to the same league had an average fund size of $11.6 billion.

Another consequence is for the investors committing funds to the private products they market: private equity firms that go public may tend to prioritize accumulating billions of dollars in assets by raising larger funds, rather than focusing on the return of the funds they raise.

Lastly, entering the public eye can be a challenge for an industry that has traditionally operated under the radar. This has led to increased scrutiny of the sector, and some investors have called for more transparency and disclosure from listed private equity firms. Most of the criticism relates to executive compensation and corporate governance.

Looking forward: steering through turbulent markets

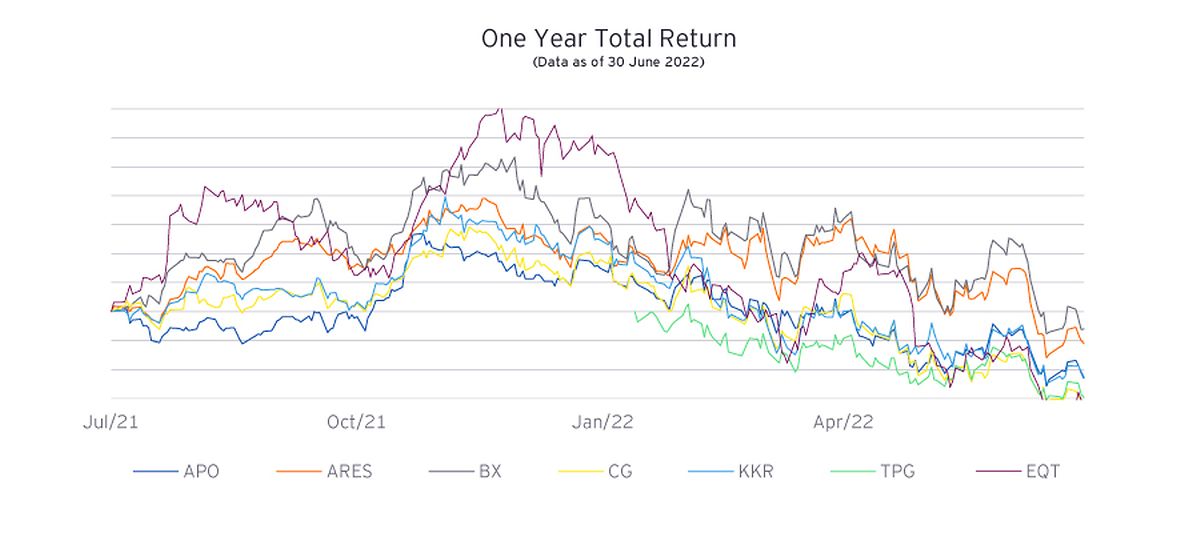

Even the highest-ranked publicly traded private equity companies are feeling the squeeze, as they all brought in a total return performance that was worse than the S&P 500 for the six-month period that concluded on June 30:

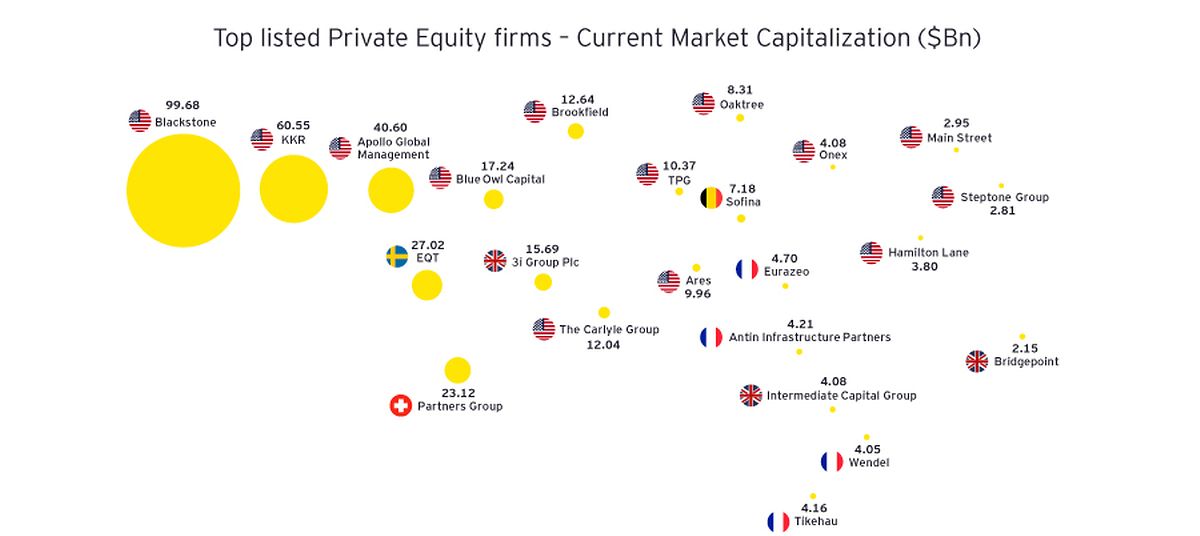

The market capitalization of publicly listed private equity firms has on average decreased by half between the end of 2021 and the end of 2022 due to current market volatility. As a result of to market conditions, moves to go public in 2023 for some private equity firms have been put on hold.

As at the end of 2022, the current market capitalization for the top listed private equity firms is as follows.2

The recent performance of listed private equity firm seems to be increasingly correlated with the performance of the stock exchanges. In other words, although the buzz around private assets has decreased, the fundamentals of the business model remain.

The stability and recurrence of cash flows leveraged from assets under management can provide a secure source of income to investors. Nevertheless, considering the increase in scrutiny from national and supra-national competent authorities, it remains to be seen how regulation costs, including the extra financial return measurement, will impact profitability, and subsequently share price and valuation, over time.

[1] The S&P Listed Private Equity Index comprises some of the leading listed private equity houses – data as of 03/01/2022

[2] Source: Bloomberg – January 2023

This article was published in Luxembourg Times.

Summary

In parallel with private equity strategies making headlines over the last 10 years with record-breaking deals and soaring returns, a batch of US and European asset managers have leveraged overall investor appetite toward the asset class and have gone public in 2021, reinforcing the trend that started a decade ago.