EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

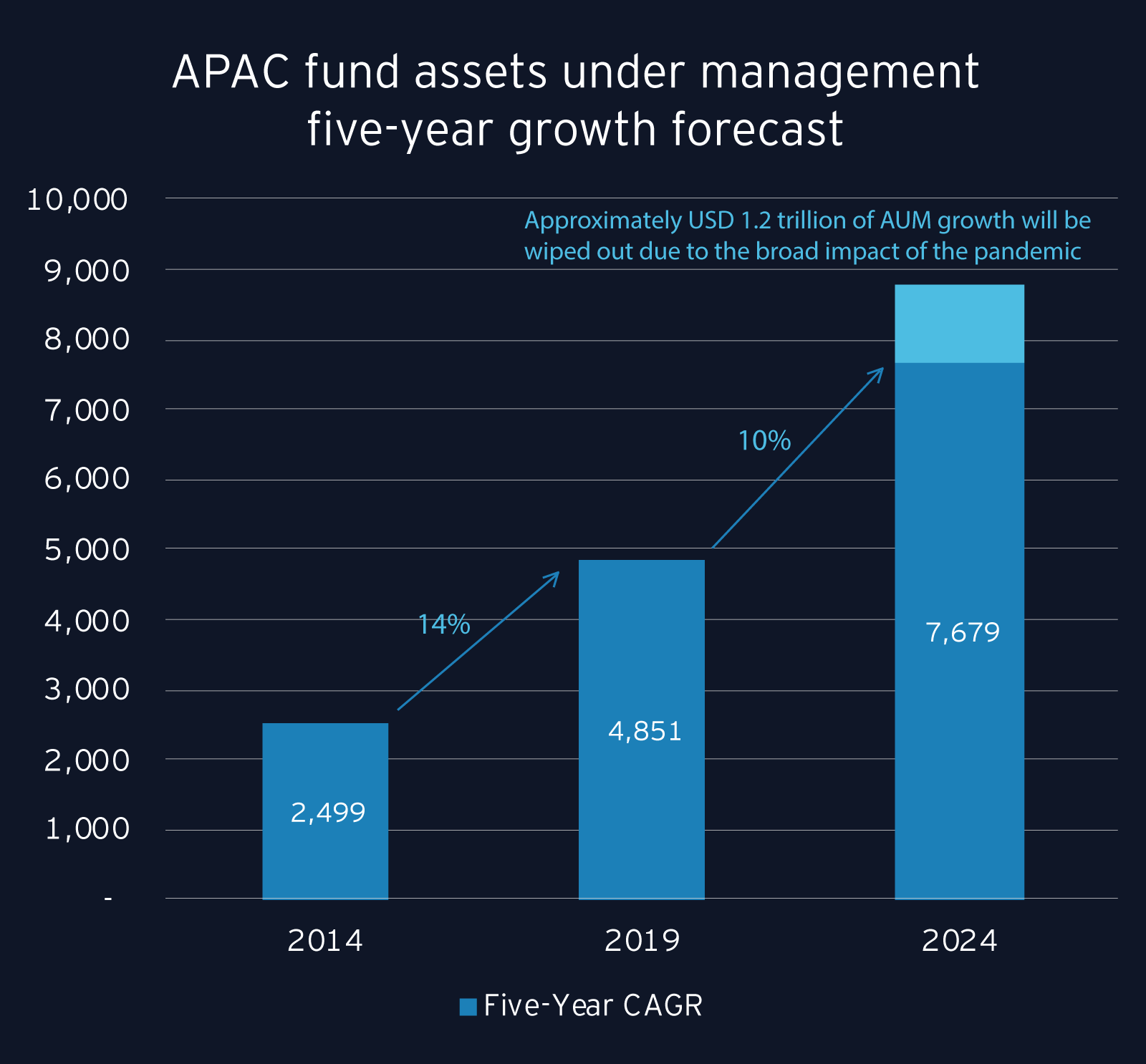

The Asia-Pacific (APAC) fund industry is characterized by its fast-growing landscape. It is enriched with a diverse economic environment, housing both developed and emerging markets. The region is a key driver of global economic growth, projected to contribute approximately 70% towards global growth in 2023.1 The asset management industry within the APAC region has also witnessed steady progress over the past ten years.

As examples of growth in the asset management sector, we mention the cases of Hong Kong, Singapore and Japan.

Source: Broadridge Data and Analytics

Hong Kong: a major hub in APAC for alternative asset management

Contributing to over one-fifth of the city’s GDP, the financial services sector is a vital component of the Hong Kong economy,2 with the alternative investment sector forming a crucial part of the financial ecosystem. Hong Kong serves as one of the most prominent jurisdictions in Asia-Pacific for alternative asset management, showcasing the highest volume of assets under management and a dense concentration of industry professionals.

In 2022, Hong Kong hosted 2,069 asset managers, a 5% rise from the previous year, and managed a total of HK$30.54 trillion (US$3.91 trillion) in assets (14% drop from 2021).3 The asset management and fund advisory business commanded an impressive figure of HK$22.39 trillion, while the private banking and private wealth management sector handled HK$8.97 trillion. The Hong Kong wealth and asset management industry comprised a workforce of 54,322 in 2022.4

It is worth noting that the rise in APAC’s contribution to global AUM is significantly fueled by alternative asset classes, with the Asia-Pacific region excelling in this sector at an even faster pace.5 Hong Kong manages most of the alternative assets within this area. It stands as Asia's largest international asset management hub, the top cross-border private wealth management, and hedge fund center, and it ranks second after Mainland China as the region's private equity center.6

There's still vast scope for further growth in the alternative assets sector as investors are exploring ways to diversify and expand their investment portfolios. There has been an increase in high-net-worth individuals in Mainland China and Southeast Asia, ranging from ultra-high-net-worth individuals to the emerging middle class. This growth remains consistent, and they all aim to preserve and grow their wealth. The count of ultra-high-net-worth individuals in China is expected to surpass that of all of Europe by 2027, and it is predicted that the population of millionaires will double in Mainland China between 2022 and 2027.7

Singapore: the largest market of foreign funds in Asia

According to the Singapore Asset Management Survey,8 in 2022, Singapore hosted 1,194 registered and licensed fund management companies, reflecting an 8% rise from the previous year. Despite a 10% decrease in total AUM from 2021, including a 20% decline in traditional assets and a 10% fall in alternatives, the total AUM stood at an impressive S$4.9 trillion (approximately US$3.65 trillion as at 31 December 2022).

These numbers reflect the sentiment of global asset managers and investors, that being: Singapore is a crucial gateway to harness the region’s growth opportunities. A significant 76% of the AUM is sourced from outside Singapore, with 15% coming from Europe. The vast majority, 88% of the total AUM, was invested abroad. Of this, 13% of the AUM was allocated to assets in Europe. Asia-Pacific ex-Singapore accounted for 44% of the invested AUM.

Singapore has positioned itself as an ideal location for asset managers to establish their core investment professionals and decision-makers. Further evidence of this is the fact that discretionary AUM composed more than half of the total AUM in 2022, recorded at 52%.8

Trade ties between Luxembourg and Singapore, especially in financial services, which form more than 90% of countries’ exchanges, have witnessed a significant surge in recent years. Interestingly, around 60% of the foreign funds circulated in Singapore originate from Luxembourg. Singapore stands as the leading market in Asia for foreign funds, with over 4,300 foreign funds registered for distribution within the country.9

Japan: significant efforts being made to reform the country’s asset management industry

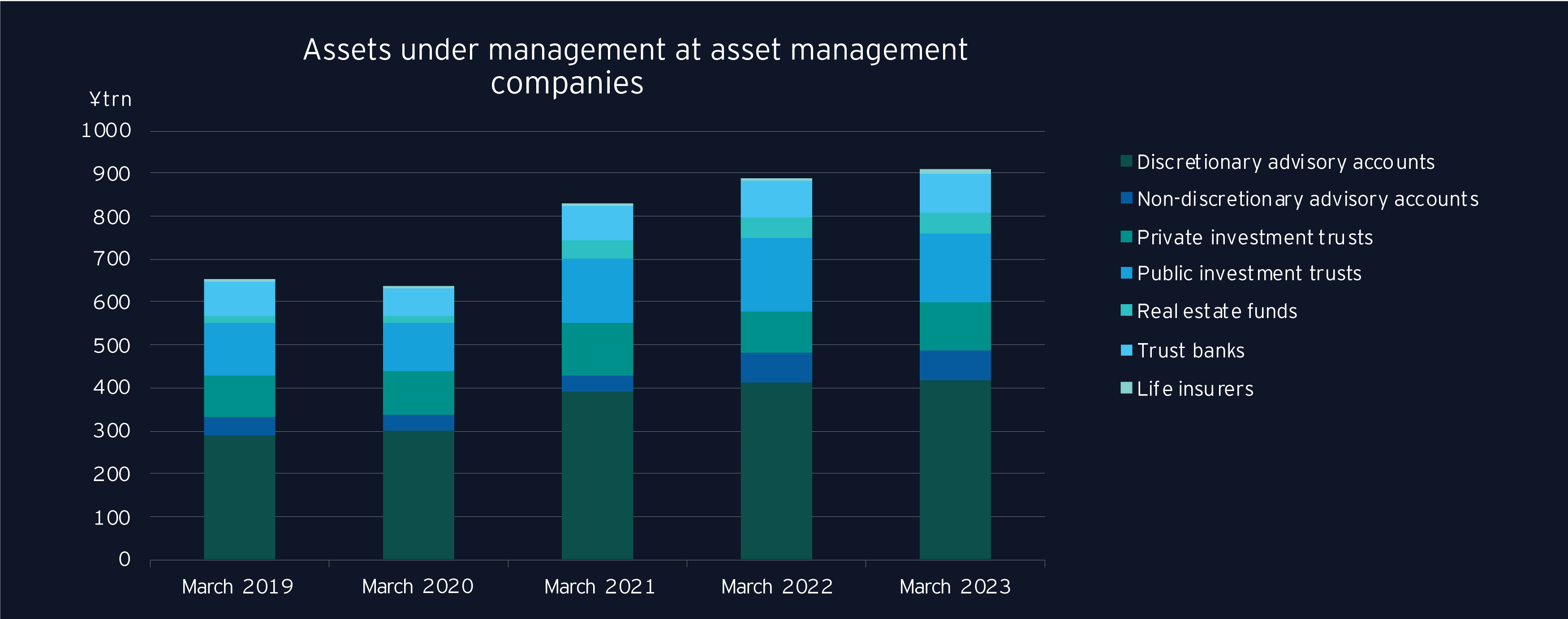

As of March 2023, Japanese asset management firms reportedly managed an estimated ¥909 trillion (€5.56 trillion),10 approximately 140% of the country’s GDP.11 This marks year-over-year growth of 2%. This growth rate is the second smallest in the past decade, a trend possibly due to the underperformance of both domestic and international bond markets in the wake of tightened monetary policies and other monetary adjustments. Considering the cross-border distribution of investment funds, only 1% of global cross-border money originates from Japan.12

Source: NRI, based on Japan Investment Trust Association (JITA) and Japan Investment Advisers Association (JIAA) data and financial reports of AMCs

Note: Life Insurers' AUM represent DB pension assets in special accounts

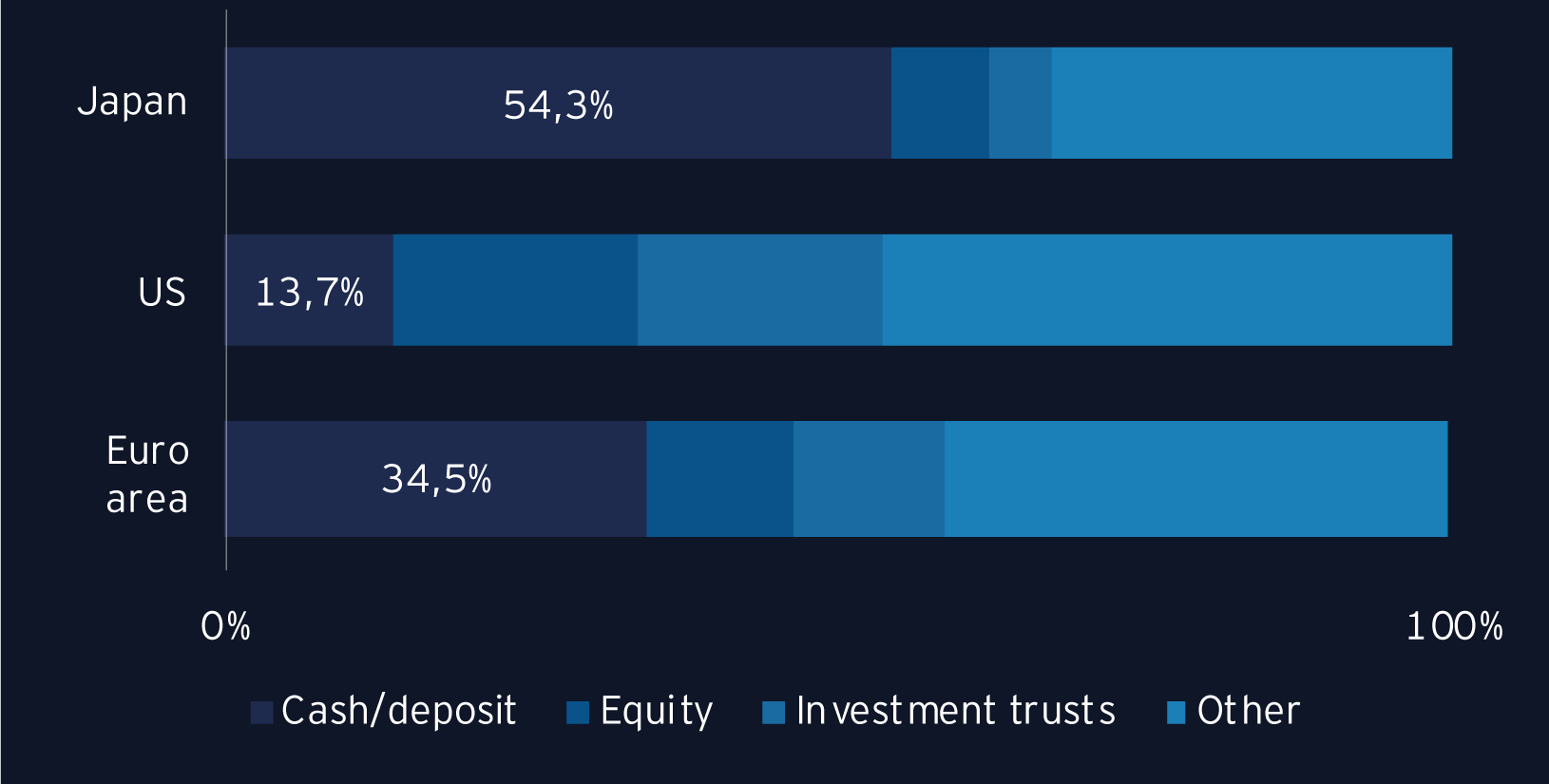

Data originating from the Bank of Japan reveals that Japanese households held total financial assets of approximately ¥2.12 quadrillion (€13 trillion) as of September 2023, with more than half of these assets maintained in cash or savings accounts. Compared to the US, Japanese household finances comprise 50% cash and savings, compared to almost 14% for the US, and 35% for the Euro area. This significant volume of funds presents a substantial untapped opportunity for asset managers.13

Source: Bank of Japan, Flow of Funds

Japan is embarking on a number of activities to elevate its status as a leading global asset management center, highlighted in the government plan, “Policy Plan for Promoting Japan as a Leading Asset Management Center”, released in December 2023. The growth plan is centered around reforming the country’s asset management market with a major objective to shift huge household savings to more long-term investments. At the same time, the plan addresses asset ownership, growth and diversification of investment opportunities, stewardship opportunities and strengthening public relations and communications. Aligned with this, the financial regulator has set out to make it easier to establish asset management firms in Japan, by permitting firms that focus mostly on investing, in so doing enabling firms to have smaller wealth management functions and outsource broader asset management functions (e.g., valuation, reporting), to third-party firms.14

Luxembourg becomes a gateway for Asian entities to penetrate the European market

Asian entities are already benefiting from Luxembourg as a hub to access the European market. The FAQ on the payments industry in Luxembourg for Chinese/Asian players, issued by EY Luxembourg in January 2023, affirms that branches of large Asian players, which are also active in other parts of the world (e.g., South-East Asia, the Middle East and South America), are setting up in Luxembourg.15 Many Asian-headquartered firms, like several international players, choose Luxembourg due to the international recognition of its financial center as well as the possibility to use the European passport, which enables delivery of cross-border services to other states in the EU.

Luxembourg financial center key figures: APAC focused

- Luxembourg stands as the #1 investment funds center in Europe, and #2 globally after the US, managing €5,285 billion in net assets under management (December 2022)16

- 76 Promoters of APAC origin with a total of 368 funds domiciled in Luxembourg, amounting to €84.1 billion in total AUM17

- 16 ManCo/AIFMs whose parent origin is from the APAC region17

- 20 banks of APAC origin established in Luxembourg18

- At least seven EMIs/PIs/VASPs of APAC origin set up in Luxembourg: Alipay (China), PingPong (China), Rakuten (Japan), Bitflyer (Japan), Sygnum (Singapore), B2C2 (Japan), and XGD (China)

The top fund managers in Europe and APAC are dominated by cross-border groups, with the same top three in both regions (in order: BlackRock, JPMorgan AM, and Fidelity) showing that, despite local differences, it is possible to have global success.19

Why Luxembourg for Asian fund managers

Asian fund managers can benefit from the Luxembourg environment to enter and/or expand their presence in the European market. Luxembourg is hailed as one of the premier global hubs for fund domiciliation, standing out as the second largest investment fund center worldwide after the United States. Its appeal lies in its robust regulatory environment, particularly its versatile legal framework that supports various types of investment funds.

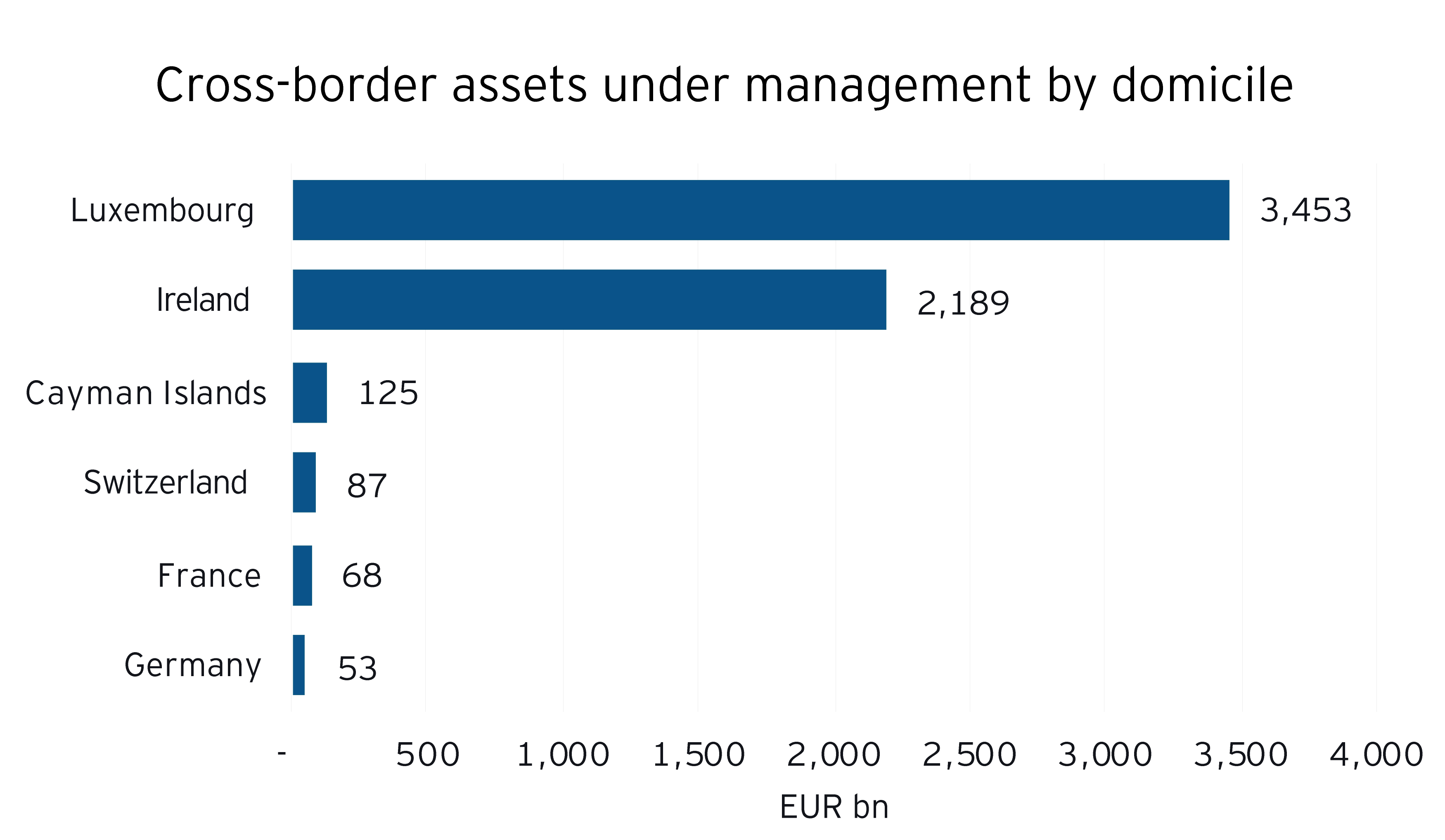

Distribution is a strength of Luxembourg's fund industry. Luxembourg funds are distributed in more than 70 countries. The world’s biggest fund managers use Luxembourg as their distribution hub for distributing their investment funds across the world. The local ecosystem has the necessary expertise to overcome most obstacles that arise in worldwide fund distribution because of its understanding of the legal, technical, operational and cultural complexities of the global asset management industry.

Banks in Luxembourg specializing in fund services and offering both local and international private banking and corporate finance networks, serve as efficient conduits for fund distribution. Notably, a number of service providers within the Grand Duchy support direct distribution of funds, and also ensure the supervision and control of a fund's distribution network. Remarkably, Luxembourg accounts for more than half of all cross-border assets worldwide.20

Source: Broadridge GMI, March 2022, fund view excluding money market and fund of funds. Cross border only.

Some of the reasons why Luxembourg is so attractive for fund managers include:

- EU Passport: Authorized fund managers can benefit from both a management and a marketing passport across the EU/European Economic Area. The management passport means that the IFM can manage and market funds in different EU countries. Some specific vehicles (such as UCITS and ELTIF) also benefit from a product passport which allows the fund’s shares, units or partnership interests to be marketed to investors across the EU through a regulator-to-regulator notification regime.

- Stability: Luxembourg has a very stable political and economic environment. It is one of the jurisdictions which has triple-A credit rating, which is one of the key aspects when fund managers and institutional investors screen and select their investment targets. International investors generally associate Luxembourg funds (including UCITS and AIFs) with strong investor protection and stringent regulatory supervision. This makes Luxembourg a natural choice of fund domicile when fund managers desire to raise capital from international investors for global investments.

- Tax regime: Luxembourg’s tax regime and wide treaty network are also conducive to the development of the onshore fund and fund management industry, encouraging global fund managers to set up both the fund and fund management vehicles in Luxembourg for global investments. Funds are usually exempt from income tax but are subject annual subscription tax. Exemptions may apply.

- Flexibility: Luxembourg provides the industry with a vast fund toolbox which allows fund managers to choose the vehicle which fits best its strategy.

Luxembourg fund toolbox

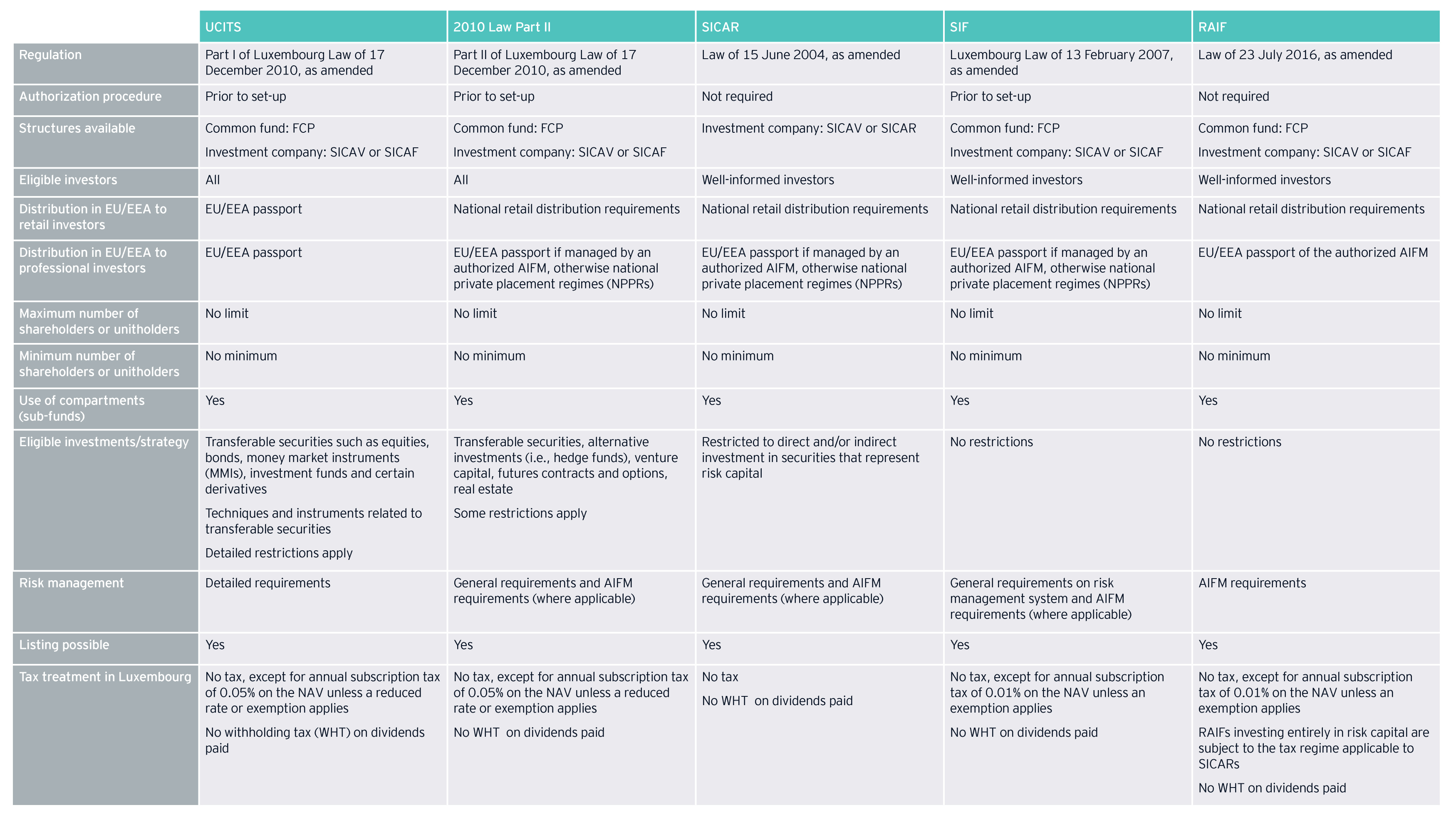

Luxembourg’s legal and regulatory framework continually undergoes enhancements to provide investment managers with the most effective tools for structuring their investments and safeguarding the interests of investors. Several investment vehicles are available for investment in transferable securities and alternative investments, including real estate, private equity, venture capital and hedge funds. The Luxembourg financial sector offers a versatile array of both regulated and unregulated investment vehicles. Below there is a matrix summarizing the Luxembourg vehicles which are directly or indirectly supervised by the CSSF. Note that funds can also be set as securitization vehicles (as per the Law of 22 March 2004 on securitization, as amended) or in any legal structures available under 1915 Law (such as, SCS, SCA and SCSp). Funds can also be set under other EU labels (e.g., ELTIF, EuSEF and EuVECA).

Luxembourg fund toolbox

Which current hot European regulations should APAC asset managers keep an eye on, when entering or expanding their presence in Europe?

RIS: The European Commission’s endeavor to address retail investor participation

Launched in May 2023, the Retail Investment Strategy (RIS) is the European Commission’s avenue to increase retail investor participation in Europe’s capital markets, which currently lag behind other regions. Data highlights that EU household assets invested in financial securities like stocks or bonds are at a mere 17%,21 in stark contrast to the US's 43%. The initiative also intends to address high fees for retail investors, usually 40% higher than for institutional investors, and concerns over investment advice neutrality, with 45%22 of European investors sceptical about it.23 Countries like Japan, characterized by substantial household finances primarily in savings or cash, stand to gain significant insights and potential strategies from the direction of this initiative.

EY thought leadership

For more information regarding ELTIF, please refer to our thought leadership:

ELTIF 2.0: Alluring for alternative investors in APAC, specifically those focused on infrastructure and real estate

The revised European Long-Term Investment Fund Regulation (ELTIF 2.0), applicable since January 2024, is set to make the ELTIF more attractive for investment in infrastructure, real estate, and small and medium enterprises (SME) across Europe, especially at a time when there's growing interest in private equity and debt investments. The changes introduce more flexibility in eligible assets, portfolio composition, distribution, and authorization, which many asset managers in the APAC region may find appealing. This change is indicative of an increased willingness to explore alternative investment funds and may impact financial services sectors in several APAC countries, especially, for example, China, which is known for its extensive investment in infrastructure projects.

How EY can help

Maintaining a dedicated APAC representation here in the Grand Duchy has empowered EY professionals in Luxembourg and the APAC region to work closely together as a team for many years, serving clients based in Luxembourg in their native languages as well as English. The transnational collaboration involves a comprehensive team approach to facilitate smooth communication and coordination.

EY has a global commitment to wealth and asset management (WAM), and Japanese clients are now further supported by EY Luxembourg’s dedicated Japan desk. There are over 800 EY WAM professionals in APAC (320 in Hong Kong, 200 in Japan, 300 in China, 100 dedicated to WAM Assurance in Singapore) and 500 WAM professionals in Luxembourg.

Investment fund management setup services

Here at EY Luxembourg, we guide our clients through the comprehensive process of obtaining ManCo and AIFM licensing permissions. Our enduring and reliable relationships with the CSSF are forged from numerous successful authorization projects for fund managers spanning various asset classes. Consequently, we've cultivated a profound understanding of regulatory compliance, and comprehend our clients' strategic objectives and business imperatives.

Cross-border fund distribution services

EY integrates a wide range of services to assist clients in the cross-border distribution of their funds, including, but not limited to: permanent monitoring, initial registration, fund maintenance, KID updates, customized support, regulatory-related event management aligned with the fund lifecycle, and other ad hoc services (e.g., distribution strategy assessment, coordination of translation services, documentation filing, among others).

Audit and tax

EY provides comprehensive audit and tax services, enabling our clients to remain compliant with financial regulations and optimize their tax strategies. Our expert tax consultants and auditors deliver insights that help transform our clients’ operational structures and drive greater efficiency and growth.

Summary

The Asia-Pacific (APAC) region is a key driver of global economic growth, projected to contribute approximately 70% towards global growth in 2023. Discover how Luxembourg becomes a gateway for Asian entities to access the European market.