EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Limited, each of which is a separate legal entity. Ernst & Young Limited is a Swiss company with registered seats in Switzerland providing services to clients in Switzerland.

Select your location

Local sites

Food security - considering all ESG aspects - demands a new climate of innovation that supports effective plant protection products in the EU.

In brief

- Amid economic and political pressure, e.g., Green Deal, the EU needs productive, sustainable agriculture to meet food security and affordability challenges.

- The toolkit of plant protection products - synthetic, biocontrol and new tech are at different levels of maturity owing to innovation, investment levels and opportunity costs.

- EY study on return-on-investment shows the need for favorable innovation environment to better support the aim of food security in the EU.

Situation

As the world population grows, so too does pressure on our food system1. The situation is compounded by unpredictability in global supply chains as well as the continual reduction in the amount of arable land accessible to farmers2.

To ensure a safe and consistent food supply – in terms of both yield (for volume) and quality (to maintain nutritional value over a longer storage period) – all participants in the agricultural ecosystem must collaborate.

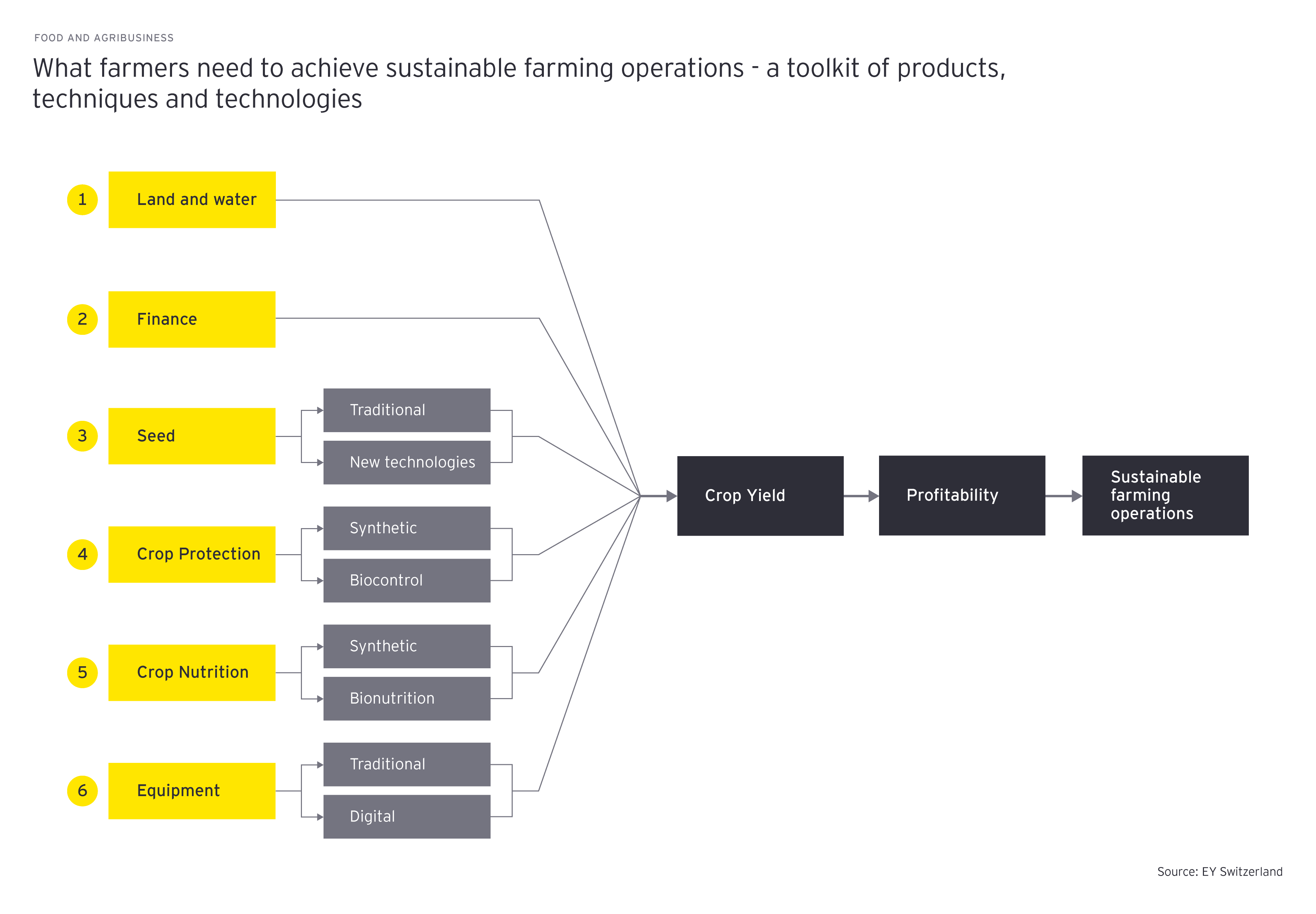

Farmers require inputs such as water, land, seed, equipment, finance, crop protection and crop nutrition to safeguard their yield, achieve profitability and contribute sustainably to the food supply system. This means they need at their disposal a toolkit of products, techniques and technologies that support these aims.

A definition of plant protection products

Plant protection products (PPP) are solutions that farmers use at the right time to control any pest or diseases on their crop. Historically, synthetic products have been utilized to enable better control of the crops, however, innovative exploration in digital and biocontrol spaces are being explored as additional – and sometimes complementary – toolkit options.

With many practical challenges to overcome regarding novel PPP approaches, regulators across the world should continue to build on their mission to ensure that when used appropriately, all PPP are safe for all stakeholders, including farmers.

In this article, EY (we) focus on the regulatory environment for PPP in the European Union (EU), providing insights based on our industry research. We have also put forward our proposal for the EU’s legislative framework for sustainable food systems.

Complication - Regulatory pressure

In the agricultural industry, there is a tendency toward more stringent regulations for agricultural input in developed nations than in developing nations3. In the EU in particular, complexity of regulatory frameworks for PPPs are higher than other geographies4. The EU is keen on promoting non-chemical alternatives for pest control and integrated pest management (IPM) systems, especially focusing on biological pesticides, known as biocontrols5. This is in line with the overall trend toward increasing regulatory requirements for PPP in the EU, including the recent Chemicals Strategy for Sustainability (CSS) to achieve more biodiversity and mitigate climate change.

EU target

Reduced risk of chemical pesticides and use of more hazardous pesticides by 2030

For instance, by 2030 the European Commission has committed to reducing by 50% the usage and risk of chemical pesticides and reducing by 50% the use of more hazardous pesticides via the Farm to Fork (F2F), European Green Deal (GD), and Biodiversity strategies. This is in addition to a 50% decrease in the number of approved active substances in pesticides over the last 25 years, according to the European Commission, the European Food Safety Authority (EFSA) and EU member states.

- The Global Population Will Soon Reach 8 Billion—Then What? | United Nations

- FAOSTAT

- A review of the global pesticide legislation and the scale of challenge in reaching the global harmonization of food safety standards

- European journal of risk regulation

- SANTE/11319/2017-EN CIS and Farm to Fork targets - Progress

- Phillips-McDougall-Evolution-of-the-Crop-Protection-Industry-since-1960

- Clinical development times for innovative drugs

- Biopesticide Regulation: A Comparison of EU and U.S. Approval Processes

- Commercialization of biotech-derived crop in since 1990s - USDA

- +From the current assessment

Summary

Regulators and farmers ultimately want the same thing: a safe, secure and sustainable food supply system for consumers. While the EU can certainly continue on its own path, there needs to be some means of incentivizing, encouraging and enabling innovation if the objectives of the Green Deal are to be realized in practice. We encourage dialogue between all stakeholders in the agri-food value chain to ensure that supply chains continue to meet the needs of consumers in the future, aiming towards a globally aligned framework to allow innovation for sustainability.