EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

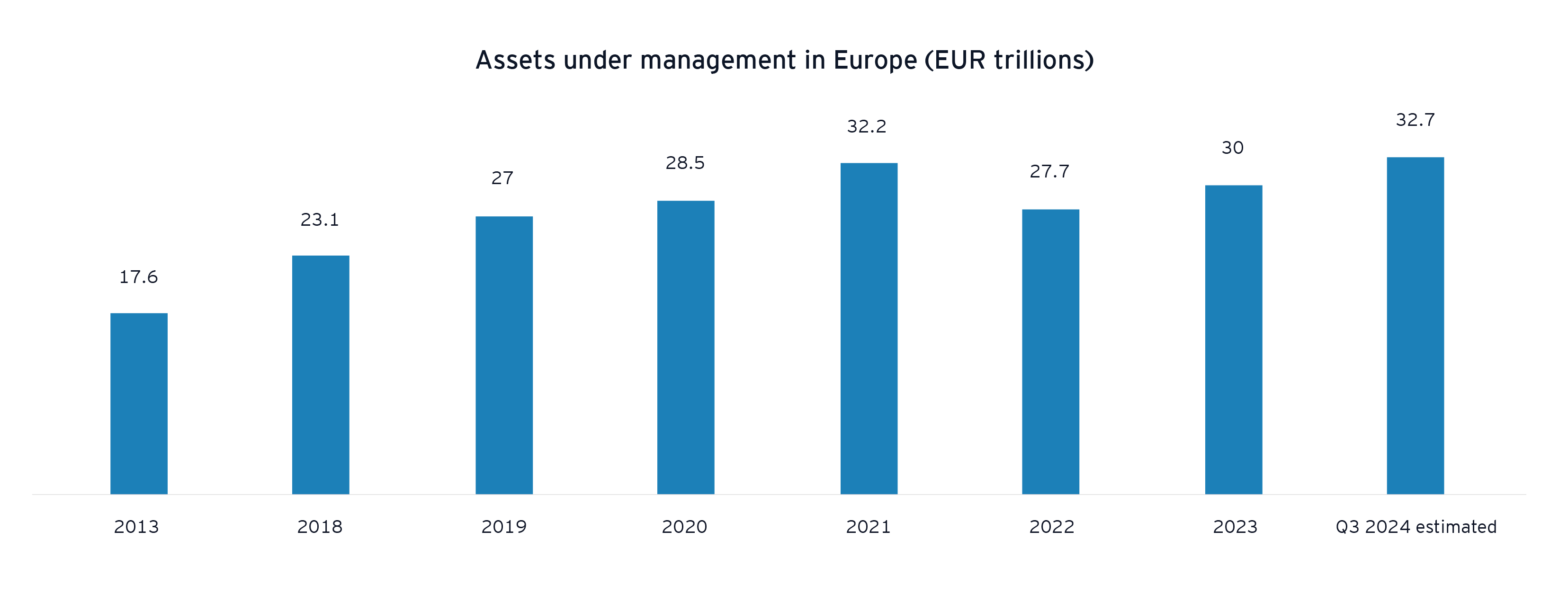

The wealth and asset management (WAM) industry has experienced significant changes in the last decade, with the early 2020s bringing instability and disruption. Despite economic headwinds, like high interest rates, resurging inflation, and geopolitical uncertainty, the industry has continued to grow. Nonetheless, there is pressure to reduce costs while asset managers strive to remain profitable.

Now more than ever, it is crucial for wealth and asset managers to future-proof their business for strategic resilience, by paying attention to five key trends.

Source: EFAMA1

Recent trends shaping the industry

Trend 1 – Consolidation: Winner takes all phenomena and new revenue-generators

There has been a surge in merger and acquisition (M&A) activity in the global asset management industry in response to increased financial pressures and EBITDA erosion.2 Wealth and asset managers are pursuing deals to scale, control costs, diversify into higher margin products and expand client reach. Several notable recent M&A transactions highlight this trend.

Source: EY Insights Analysis, 4Q23 Earnings Press Releases, Annual reports 2023, 10-Ks, 10-Qs and Financial Supplements

Major US acquisitions: In the US, a major financial institution finalized an agreement in 2020 to acquire a provider of advanced investment strategies and wealth management solutions with over USD500 billion in AUM. This acquisition positioned the firm as a leading asset manager with approximately EUR1.2 trillion in AUM and over EUR5 billion in combined revenues, enhancing its market leadership in the US.

Expansion into Europe: In 2022, another prominent US-headquartered firm completed the acquisition of an investment management company for EUR1.7 billion, increasing its assets under supervision in Europe to over USD600 billion and aligning with its strategic goals to expand its European presence.

By the end of 2024, a significant deal was confirmed for EUR5.1 billion to acquire an asset management business, expected to create one of Europe’s largest firms with over EUR1.5 trillion in AUM.

Ongoing consolidation in Asia: In Asia, consolidation is ongoing but at a smaller scale. At the start of 2022, a global investment firm acquired an Indonesian asset manager with USD340 million in AUM, strengthening its commitment to the Southeast Asian market.

Proposed joint venture to create a global player: In early 2025, a proposed joint venture between two asset management operations aims to create a major global player with EUR1.9 trillion in AUM and position itself as the largest asset manager in Europe by revenues.

Strategic partnerships and inorganic growth avenues: Ongoing discussions of other major deals indicate continued consolidation in the industry, as firms seek growth through strategic partnerships with insurers. Additionally, asset managers are pursuing inorganic growth strategies to expand their footprint and capitalize on the private markets, with traditional firms restructuring to create cohesive, integrated structures across all asset classes.

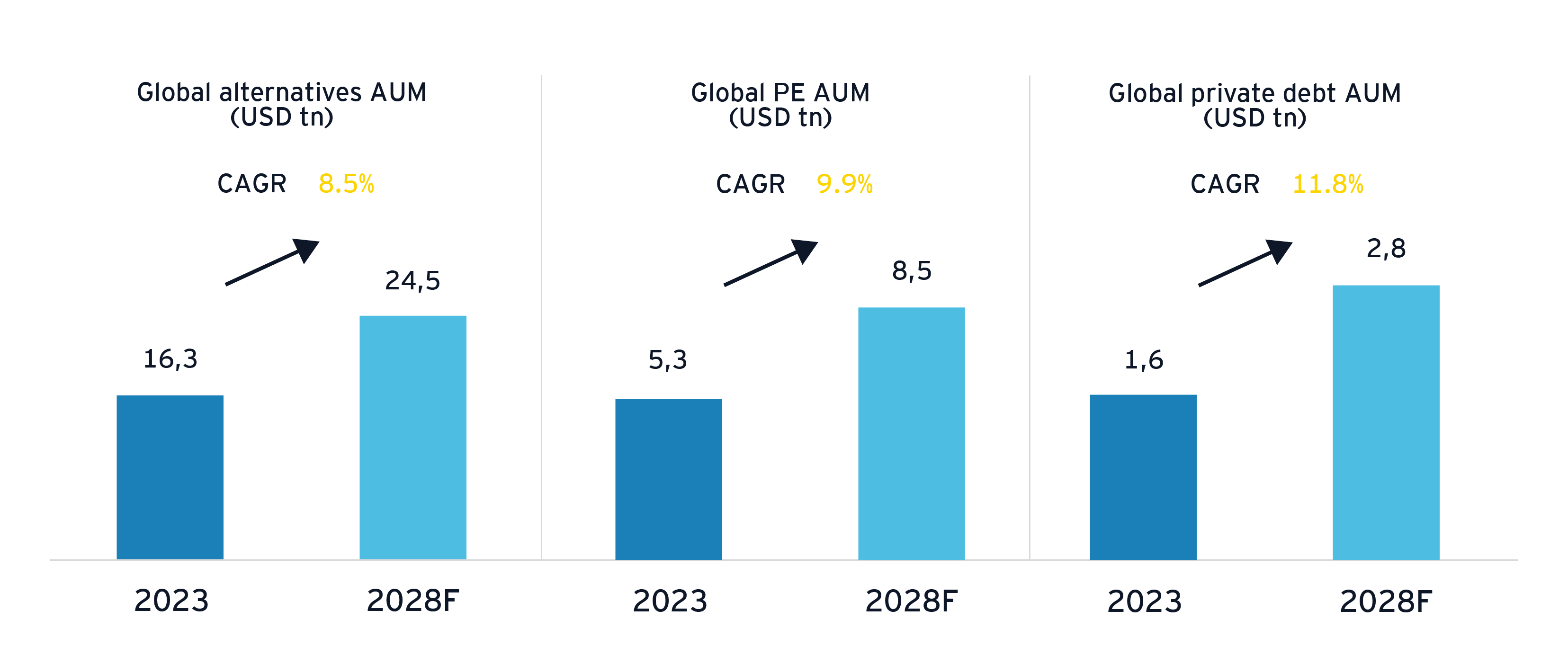

The global pool of alternative AUM is expected to grow at a faster rate than that of traditional investments, at 8.5% compound annual growth rate (CAGR) between 2023 and 2028. This is demonstrated by recent examples of giant asset managers acquiring boutique alternative investment firms. This trend in consolidation within WAM, with both alternative and traditional assets brought under one roof, underlines the importance of catering to changing needs of investors and opening up new revenue streams.

Source: S&P Capital IQ, Preqin

Recommendation: How can WAM firms strike the right balance between growth and profitability?

- Be opportunistic in acquiring to develop niche capabilities, enter new markets or scale, notably in strong growth areas like private markets and artificial intelligence (AI).

- Understand where there is maximum efficiency and profitability to be achieved via outsourcing.

- Use new operating models, integrated platforms, automation and external ecosystems to reduce costs and build an efficient infrastructure.

- Leverage managed services, particularly in areas such as finance, to drive efficiency, scalability and resilience.

Trend 2 – Innovation: Gaining a competitive edge through innovative investment products

Institutional and private investors increasingly demand a complete range of asset classes , driven by growing awareness of AI, digital currencies and assets. Firms should adopt a transparent approach to new technologies and accelerate the use of digital wrappers, tokenization and blockchain.

As an example, a major asset manager recently launched the first Luxembourg-domiciled fully tokenized UCITS product, offering investors enhanced transparency, security, and accuracy through blockchain technology.

According to recent EY research in collaboration with Coinbase, alternative funds are the most preferred asset classes for investing in tokenized assets among institutional investors (61%), as these asset classes are typically illiquid in nature, and tokenization provides investors an investment opportunity with lower minimums. Investors are also interested in investing in public funds (e.g., mutual funds, ETPs, UCITS) (44%) and real estate (43%).3

Regional differences persist in the digital assets space – the Americas lead in approving crypto ETFs, while Europe and Asia-Pacific (specifically Japan) have a mixed response to embracing it.4 5

Trend 3 – Regulation: Rapidly evolving regulatory environment

Since the financial crisis, the industry has seen increased regulation around consumer and data protection. In the EU, for example, top regulatory priorities include maintaining financial stability and risk management, sustainability, technology risks and investor protection.

Europe: The EU’s Digital Operational Resilience Act (DORA), which has been in application since January 2025, is one such example, providing consistent rules addressing digital operational resilience needs of all regulated financial entities and establishes an oversight framework for critical ICT third-party providers.

Asia-Pacific: The Asia-Pacific region has a very broad set of priority areas. Australia is prioritizing product design and distribution, sustainability and investor protection. In Mainland China, capital markets stability and protection against financial crime is a focus area, while Japan is accelerating corporate governance reform alongside financial crime, ESG and digital assets. In Hong Kong, building global competitiveness is a priority. One recent example is the Securities and Futures Commission’s announcement of the launch of the Fund Authorisation Simple Track (FASTrack) to expedite the processing of applications for simple investment funds, with the aim of bolstering Hong Kong’s market appeal.6

Faced with varied regulatory regimes across markets – and global investors with footholds in several jurisdictions – wealth and asset managers must comply with a multitude of evolving rules, but also to handle regulatory issues for their clients. This places a heavy burden on costs and operating models.

Recommendation: How can WAM firms strategically navigate regulatory complexity?

- Transform regulatory compliance through greater consistency and a holistic framework, instead of meeting evolving requirements through incremental additions.

- Put customer protection at the heart of all efforts to build trust and transparency. Deploy agile compliance and risk management frameworks adaptable to new demographics, channels, products and geographies.

- Take a transparent approach to evolving regulations around new technologies and sustainability.

Trend 4 – AI: The role of AI in transforming business operations and driving business priorities

The transformative impact of AI and generative AI (GenAI) has caused it to move rapidly from adoption by first movers only to much broader uptake in wealth and asset management.

According to EY Research, 84% of wealth and asset managers are already investing in GenAI or making plans to invest and 75% of wealth and asset managers are already building or mobilizing GenAI teams. WAM firms are more readily adopting AI to transform routine operations, drive innovative strategies, and enhance client engagement. They are also eager to understand and implement GenAI capabilities where there is opportunity.7

While the potential benefits are undeniable, the right partners, the right talent, and robust risk management and governance frameworks are needed to succeed in AI and GenAI endeavors. A strong data infrastructure and strategy are also critical to deployment and delivering positive return on investment.

Recommendation: How can WAM firms modernize data to harness the power of AI and other disruptive technologies?

- Develop a holistic data framework integrating public and private data.

- Capture data seamlessly across the value chain, mining information to new depths for proprietary insights and better investor advice.

- Take a transparent and ethical approach to AI, with controls and testing over output, alongside strong controls over the security and privacy of data.

- Accelerate investments in data resources, technology platforms, AI infrastructure and training talent, people and staff.

- Explore and leverage opportunities around data-as-a-service to reduce cost, drive innovation and create data ecosystems.

Trend 5 – Sustainable investing: Prioritizing transition finance

Asset managers have an invaluable opportunity to play a growing role in mobilizing capital for decarbonization and other goals in partnership with investors, institutions and governments. There is an equally strong appetite from many institutions and individuals to provide that capital.

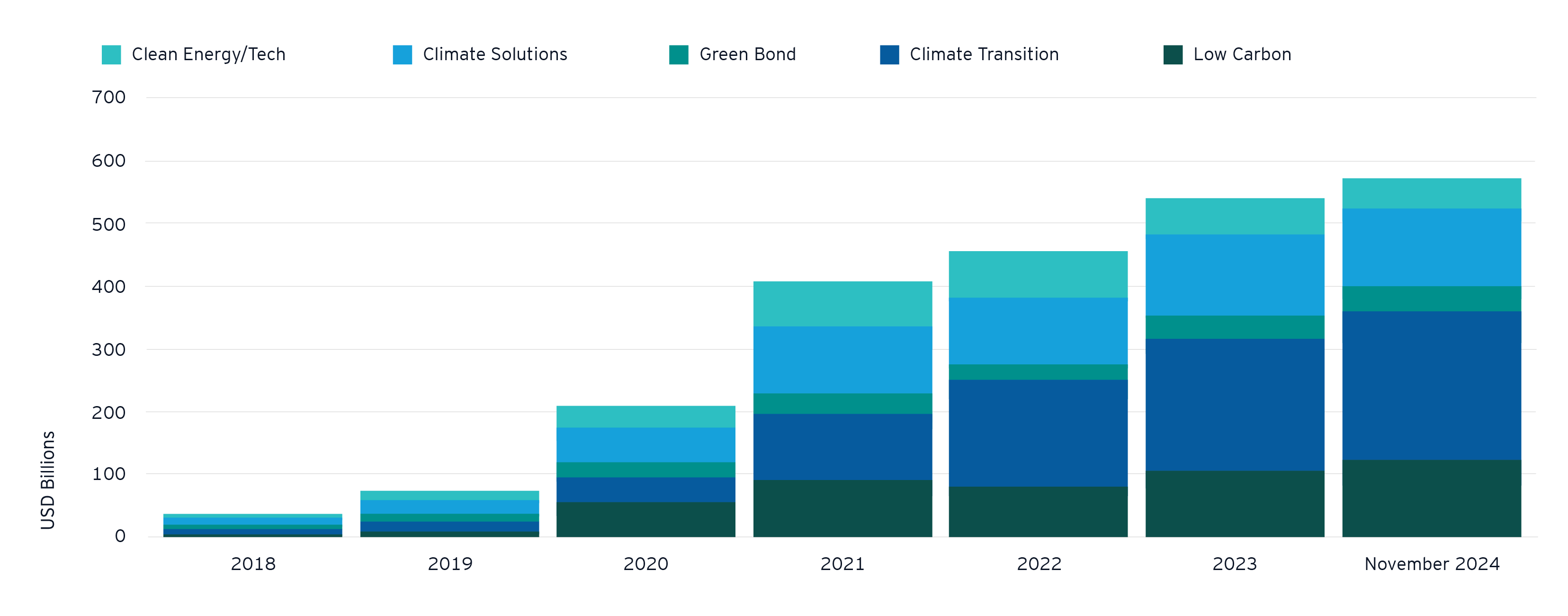

Globally, climate focused funds’ AUM increased substantially from 2018 to 2024, driven by inflows and new product development. Wealth and asset managers are also developing thematic funds, focused on themes like biodiversity and the blue economy (sustainable use and conservation of the oceans and seas). Europe is the main contributor, making up 85% of global climate assets.8

Global assets in climate funds by category

Source: Morningstar Sustainalytics as of November 2024

Despite regulatory and policy fragmentation across regions, and the complexities of ESG investing, transition finance is gaining momentum among WAM firms.

As a significant development in sustainability regulation, the European Commission recently adopted the first Omnibus package, with proposals to simplify EU rules, boost competitiveness, and unlock additional investment capacity. Refer to our article The Omnibus Package: what does the future of sustainability reporting look like?

Recommendation: How can wealth and asset managers play an active role in the sustainability agenda?

- Work with peers, regulators and clients to develop an informed, long-term sustainability strategy. Focusing on the energy transition is especially vital, and it remains essential to mitigate potential greenwashing risks.

- Engage in more scenario analysis around sustainability as regulations across countries change.

- Embed climate and environmental risks into strategy, governance and operations, making them an integral part of products and portfolios. Ensure robust regulatory reporting and meet mandatory disclosure requirements.

- Continue to develop a greater choice of thematic funds and increase allocations to themes, such as diversity, transition investing, biodiversity and the blue economy.

- Work with like-minded peers and regulators to tackle greenwashing, ensure transparent and accurate reporting to shareholders, and align performance with social impact.

Conclusion

The WAM industry is at an inflection point, shaped by years of disruption and reinvention. Firms have weathered multiple financial crises and lasting geopolitical instability, proving their ability to adapt.

But the challenges ahead may be even more complex and unforgiving. The trends of the past few years, which we have unpacked here, are not slowing down.

As cost pressures compile, client demands shift, and technology accelerates, only those who embrace transformation now will remain relevant. Wealth and asset managers must anticipate change, innovate boldly, and position themselves strategically to secure sustained long-term growth and resilience.

How EY can help

EY offers a comprehensive suite of services covering the entire fund life cycle as well as the full value chain of investment fund managers and their servicers. Our multi-disciplinary and cross-border approach covering Assurance, Tax, Transaction and Consulting services allows us to provide a holistic answer to clients’ needs. Specific to setting up an investment fund structure in Luxembourg, we offer, inter alia, the following services:

- Establishing fund structures from a regulatory, tax and operational perspective

- Setting up management companies, alternative investment fund managers and MiFID firms

- Service provider selection

- Design of operating models

- Managed services including fund registration, regulatory reporting, ESG reporting and tax reclaims

- Transaction and due diligence services

- Assurance services

- Fund and corporate accounting services

- Risk management and reporting

- Information technology selection and implementation

- Migration of investment fund vehicles

Summary

The wealth and asset management (WAM) industry has experienced significant changes in the last decade, with the early 2020s bringing instability and disruption. Despite economic headwinds, like high interest rates, resurging inflation, and geopolitical uncertainty, the industry has continued to grow. Nonetheless, there is pressure to reduce costs while asset managers strive to remain profitable.

Now more than ever, it is crucial for wealth and asset managers to future-proof their business for strategic resilience, by paying attention to five key trends.

Explore more March 2025 Market Pulse articles

Rise of active ETFs: hype, hurdles and road ahead

Actively managed ETFs differ from traditional passive ETFs by involving an investment manager who actively makes decisions to deviate from an index or benchmark. These ETFs aim to outperform through strategic security selection and sector allocation, and – while they also come with their own challenges – offer flexibility to adjust allocations based on research and market conditions.

Know Your Assets: the last update of the CSSF as a wake-up call to all sectors

Know Your Assets (KYA) is a critical process that involves identifying, assessing and managing money-laundering and terrorist financing (ML/TF) risks posed by the investments, to which professionals of the financial sector, in scope of the law of 12 November 2004 on the fight against money laundering and terrorist financing, as well as professionals of the insurance sector, are exposed. The KYA practice is essential not only for compliance with regulatory requirements but also for effective ML/TF risk management.

Retailization of Alternatives - focus on semi-liquid products

Retailization refers to the process of making alternative investments – such as private equity, venture capital, real estate, infrastructure and hedge funds – more accessible to retail investors or non-professional individuals.

The Omnibus Package: what does the future of sustainability reporting look like?

The financial industry has been animated about the latest developments in sustainability reporting. On 26 February 2025, the EU Commission published the first Omnibus Package (the “Simplification Package” or “the Package”) which aims to simplify the sustainability reporting framework by reducing the existing requirements. Market players have been sharing their feedback on this evolution, with many welcoming it as a positive turning point, some cautious about implementation and pausing their efforts, others considering that sustainability goes beyond regulation and continuing their efforts. Despite this, most can agree that the Package brings with it significant simplifications, even if no regulatory requirements are not outright removed.