EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Select your location

Local sites

PN No. 1/2022: Explanation in relation to the definition of factory for the purpose of reinvestment allowance claim under Schedule 7A, ITA

The Inland Revenue Board (IRB) has recently published PN No. 1/2022: Explanation in relation to the definition of factory for the purpose of RA claim under Schedule 7A, ITA, dated 17 January 2022. The PN was issued to explain the “factory” definition in Paragraph 9 of Schedule 7A of the ITA.

As highlighted in an earlier alert, Public Ruling (PR) No. 10/2020 – RA Part I – Manufacturing Activity was issued on 6 November 2020 (see Tax Alert No. 20/2020). The PR includes a diagram (refer to Paragraph 8.2 of the PR) which presents the following fact pattern:

i. The building is not used for the purposes of a qualifying project

ii. The building is extended, and the extension is used for a qualifying (diversification) project, and

iii. The storage space in the extended area is 30% of the total floor area of the extension

Based on the above, the PR concluded that the extension of the building would not qualify as a “factory” under Paragraph 9 of Schedule 7A of the ITA. This is because the storage space exceeds 10% of the total floor area of the extension.

Following the above, PN No. 1/2022 was issued to clarify that in a situation where the storage space in an extended area exceeds 10% of the total floor area of the extension, RA claims would still be allowed for the portion of the extension used for the purpose of a qualifying project (excluding the storage space). The PN also provides three examples to demonstrate the methodology of computing the “10% storage space area” and the tax treatment under various scenarios, as replicated in Appendix I to this Alert.

APPENDIX I

Examples of RA claim under Paragraph 9, Schedule 7A of the ITA

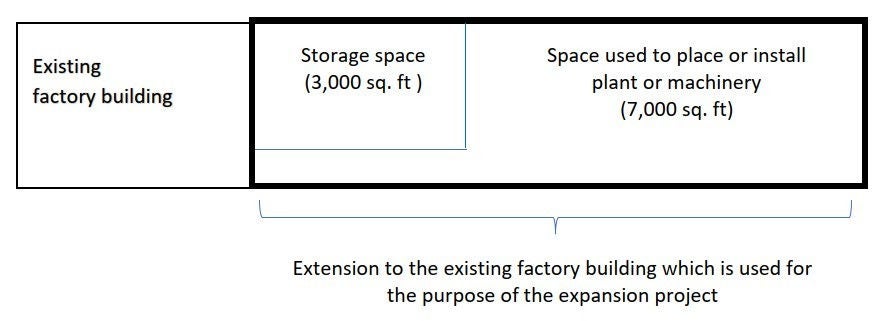

Example 1

Company A constructs an extension to the existing factory building for an expansion project to the manufacturing operation carried out. The total area of the extension to the building is 10,000 square feet (sq. ft). A portion of the extension with an area of 3,000 sq. ft is used to store raw materials while the remaining is used as a space to place plant or machinery as follows:

The capital expenditure incurred for the construction of the portion of space to place or install the plant or machinery in this expansion project (7,000 sq. ft) qualifies for RA. The raw materials storage space (3,000 sq. ft) does not qualify for RA claim because it does not meet the definition of ‘factory’ as the area exceeds one-tenth (1/10) which is 30% (3,000 sq. ft / 10,000 sq. ft x 100%) of the total area of the extension to the existing building.

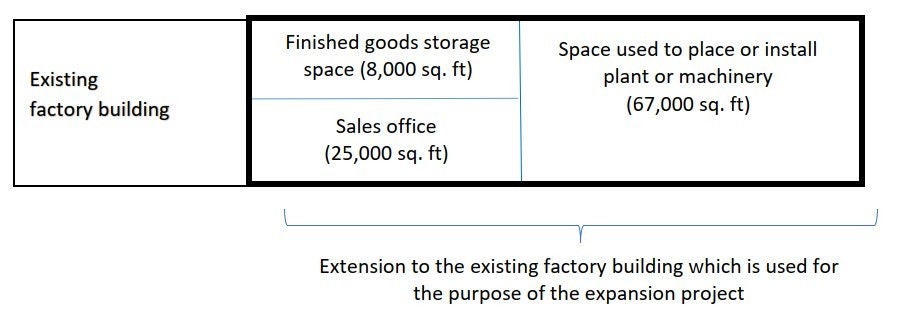

Example 2

Company B expands the production area of manufactured product by making an extension to an existing factory building. The additional area of the extension is 100,000 sq. ft. Apart from placing plant or machinery, a portion of the extension to the building is also used as a sales office and another part is used as storage space for finished goods. The use of the total space in the extension is shown as follows:

Sales office space is not included in the ‘factory definition’ in Paragraph 9, Schedule 7A of the ITA. Therefore, the total area of sales office space should be taken out for the purpose of determining ‘factory’ or space used for the purpose of the qualifying project. As the sales office does not fulfil the meaning of ‘factory’, hence, the expenditure for sales office space is not a qualifying expenditure for the purpose of Schedule 7A of the ITA.

Determination of RA eligibility for finished goods storage space shall be based on the ratio of the said storage space area (8,000 sq. ft) with the total area of the expansion project, namely the finished goods storage space and the space to place or install plant or machinery (8,000 sq. ft + 67,000 sq. ft).

As the finished goods storage space area has exceeded one-tenth (1/10) which is 10.67% (8,000 sq. ft / 75,000 sq. ft x 100%) of the total area of the expansion project, the said storage space does not fulfil the meaning of ‘factory’ and is not eligible for RA. Only the construction cost for the area used to place or install plant or machinery (67,000 sq. ft) is eligible to be given RA claim subject to stipulated conditions.

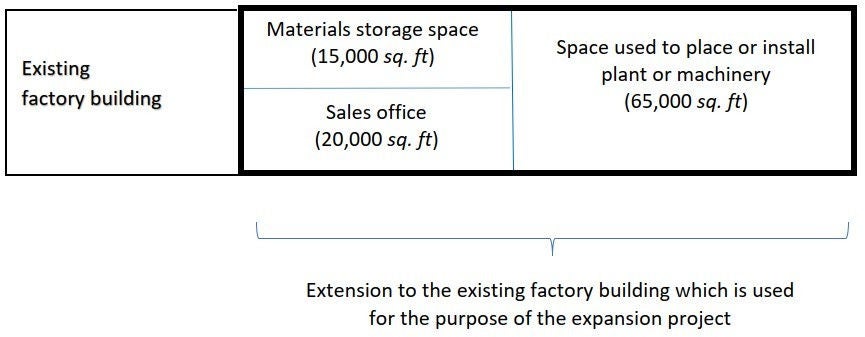

Example 3

Company C undertakes an expansion project for the company’s manufacturing business by extending the existing factory building for the installation of plant or machinery, storage of materials and also a sales office. The use of space in the extension to the building is shown as follows:

For the calculation of RA, only the portion of the space used to place or install plant or machinery fulfils the meaning of ‘factory’ and is eligible to be given RA claim. The space for storage of materials does not fulfil the meaning of ‘factory’ as the space exceeds one-tenth (1/10) which is 18.75% (15,000 sq. ft / 80,000 sq. ft x 100%) of the total area of the extension to the building used for the purpose of the expansion project. The portion of the sales office is not taken into account in the calculation of the total area of the expansion project as it does not meet the ‘factory’ definition.