EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Limited, each of which is a separate legal entity. Ernst & Young Limited is a Swiss company with registered seats in Switzerland providing services to clients in Switzerland.

How EY can help

-

Discover how EY can help the banking & capital markets, insurance, wealth & asset management and private equity sectors tackle the challenges of risk management.

Read more

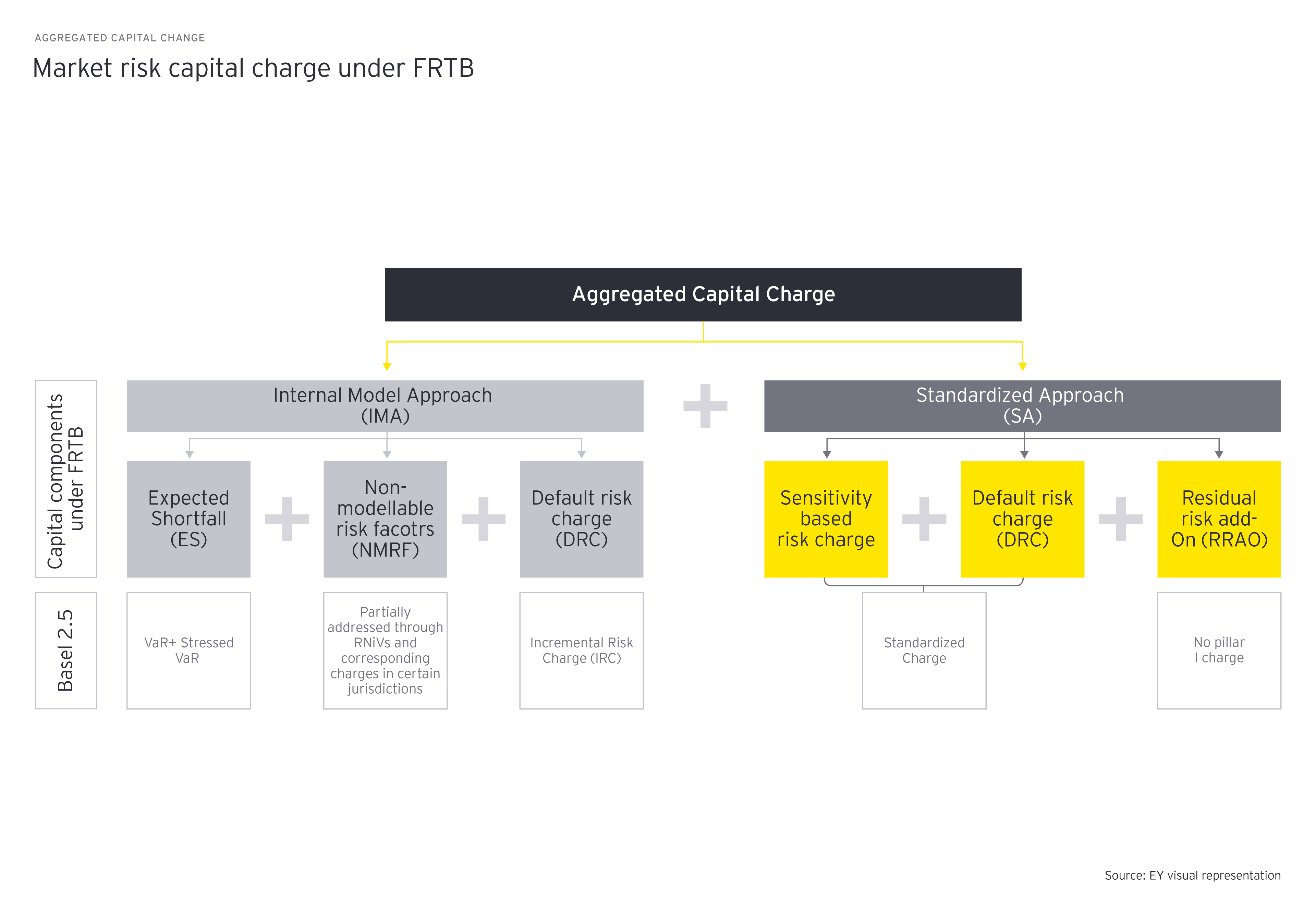

The IMA allows banks to utilize their own proprietary models to estimate risk and calculate capital requirements based on their specific trading activities, subject to regulatory approval. This approach acknowledges the unique characteristics and complexities of individual portfolios, potentially resulting in more precise risk assessments.

Under the current system, IMA is approved at the bank level, encompassing all activities and levels. However, under FRTB the validation process will be conducted independently for each desk.

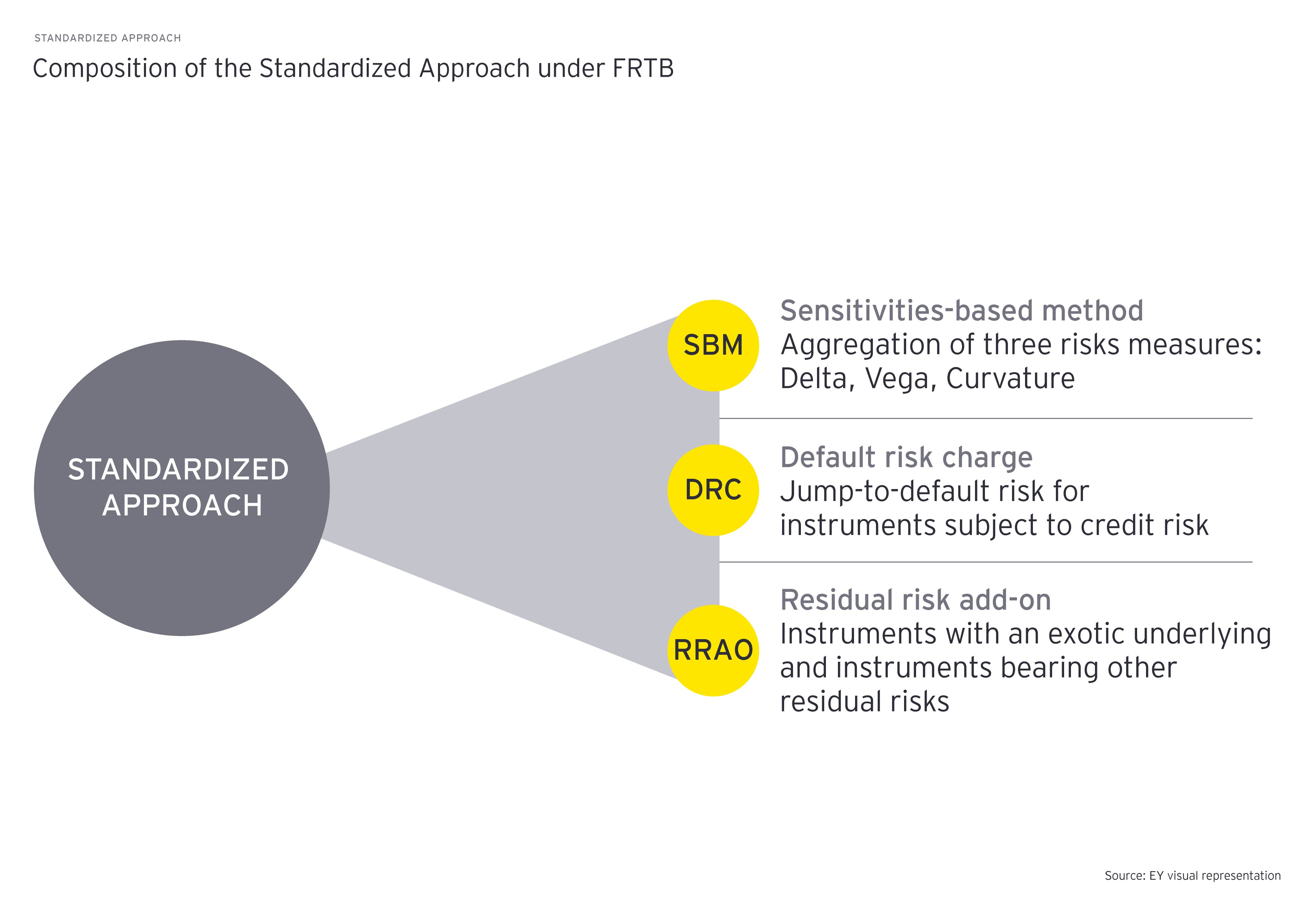

On the other hand, the SA advocates the use of a standardized formula – provided by regulators – to assess market risk. This approach offers simplicity and uniformity across banks and financial institutions, but it may not fully capture the nuances of various trading portfolios.

Choosing whether to apply the IMA or SA is not a decision to be taken lightly as it has significant implications for financial institutions. Even though the IMA offers the potential for more accurate risk measurement, it requires significant resources, modeling capabilities and risk management frameworks. Conversely, the SA provides a simpler and less advanced alternative, making it more accessible for smaller institutions or those with less sophisticated risk management capabilities.

The IMA/SA dilemma highlights the need for banks to find a balance between accuracy and simplicity in their market risk management practices. Financial institutions must carefully evaluate their capabilities, resources and risk profiles to determine the most suitable approach.

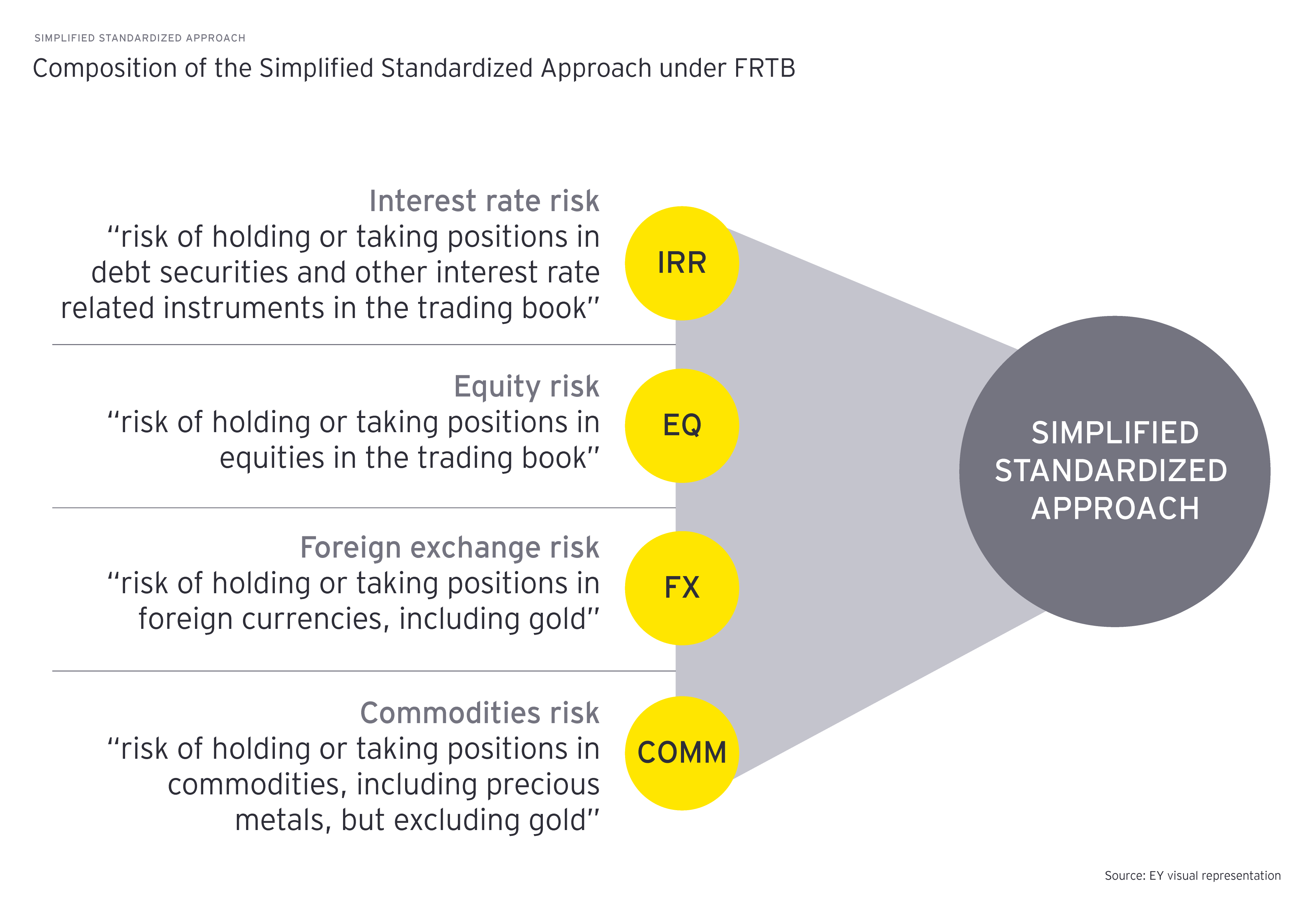

With regards to the SA, local regulators can allow individual banks to use a simplified standardized approach (equivalent to the current Basel 2.5 standardized approach) if they meet certain criteria. In this article, we leave aside the IMA and focus on comparing the path to the compliance based on whether a standardized approach or simplified standardized approach is applied.