EY refers to the global organisation, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

-

EY Studio+ helps you deliver unique customer experience (CX), using empathy and purpose and adding lasting value to customers, your business and society.

Read more

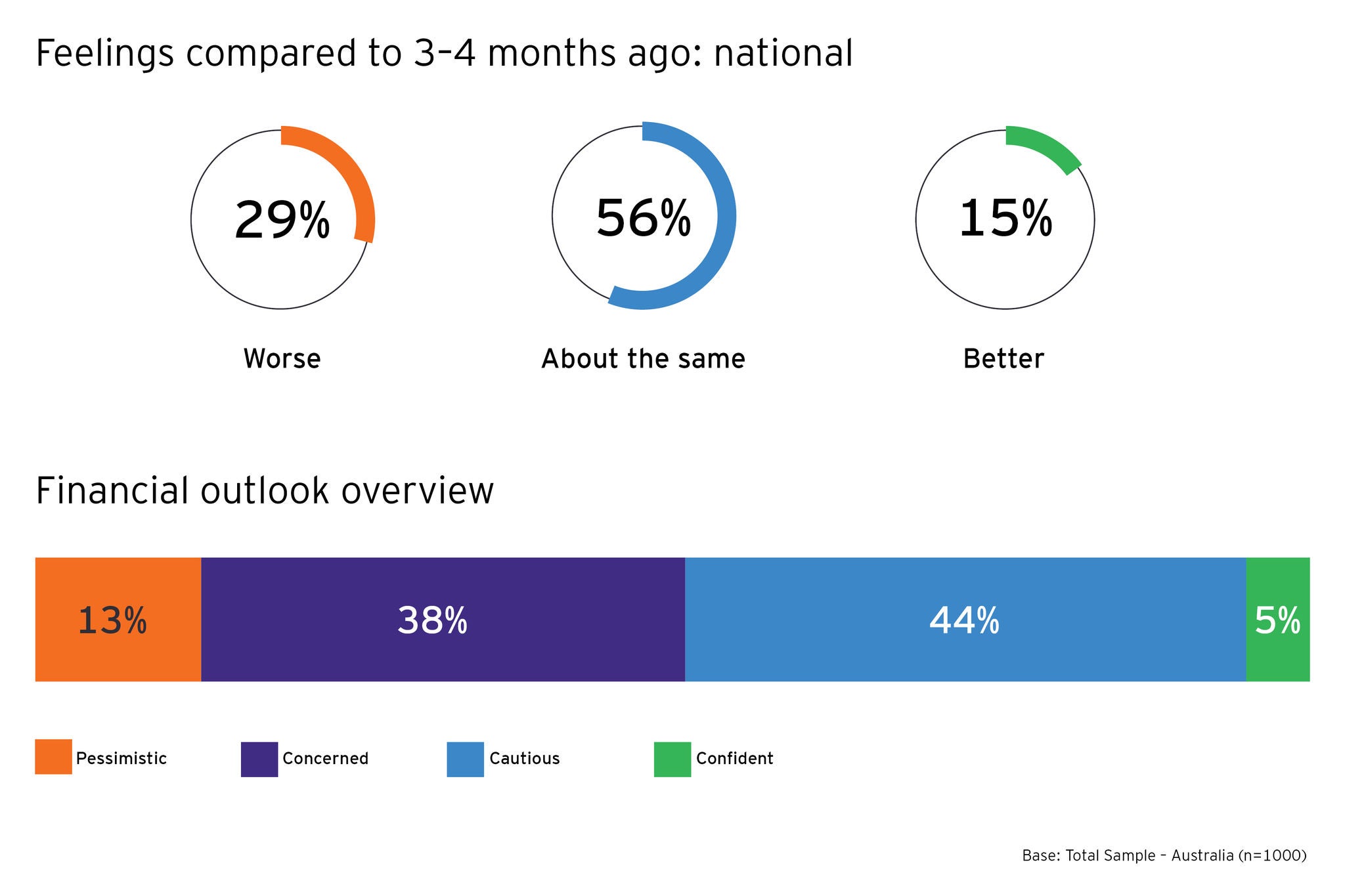

Economists often observe that nations enter recession at a sprint but come out at a much slower pace. The 12th EY Future Consumer Index suggests they may once again be right, as a quarter of Australians expect the economy to be in a similar position in three years’ time and just over a third (34%), anticipate it will be worse.