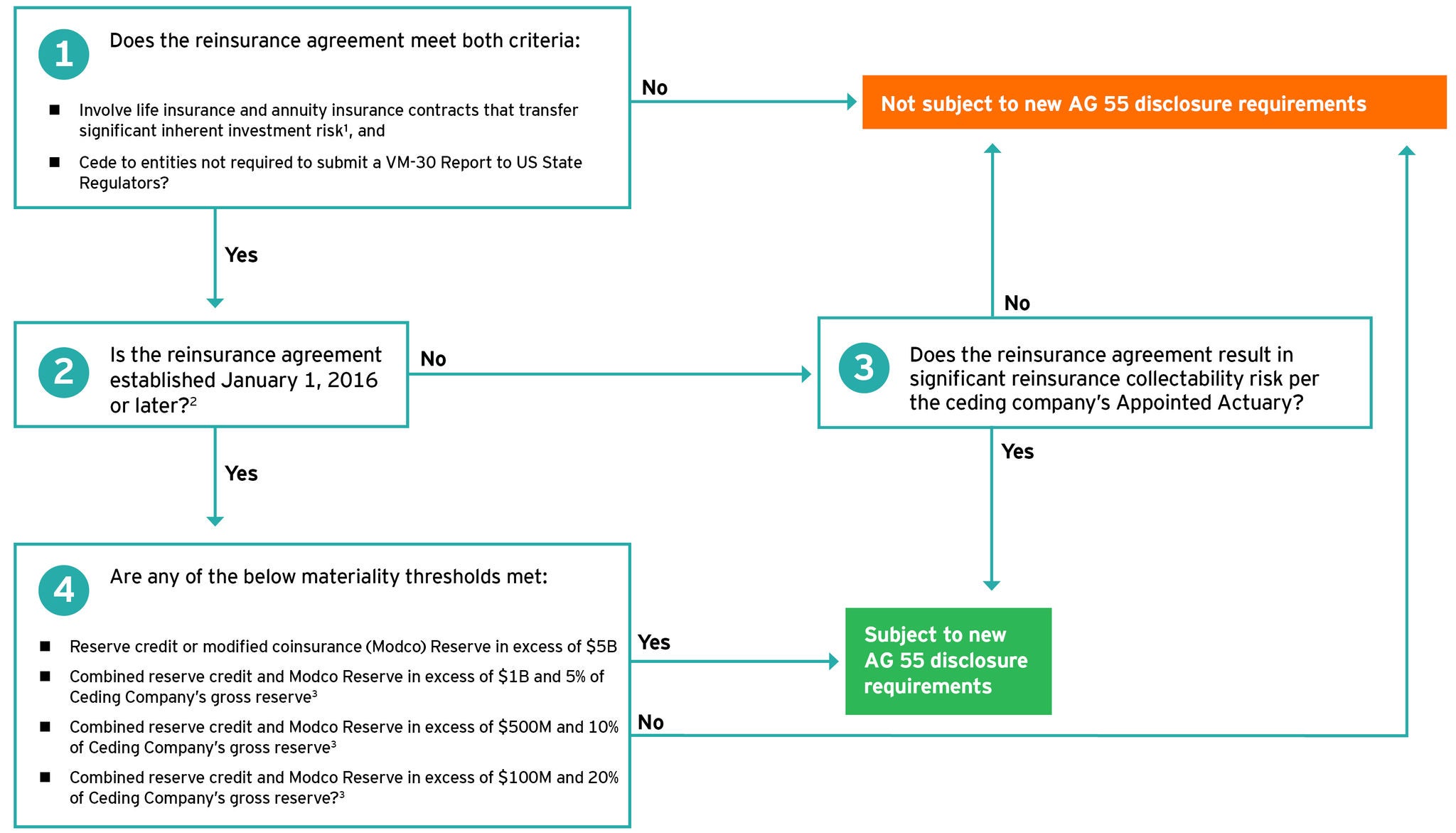

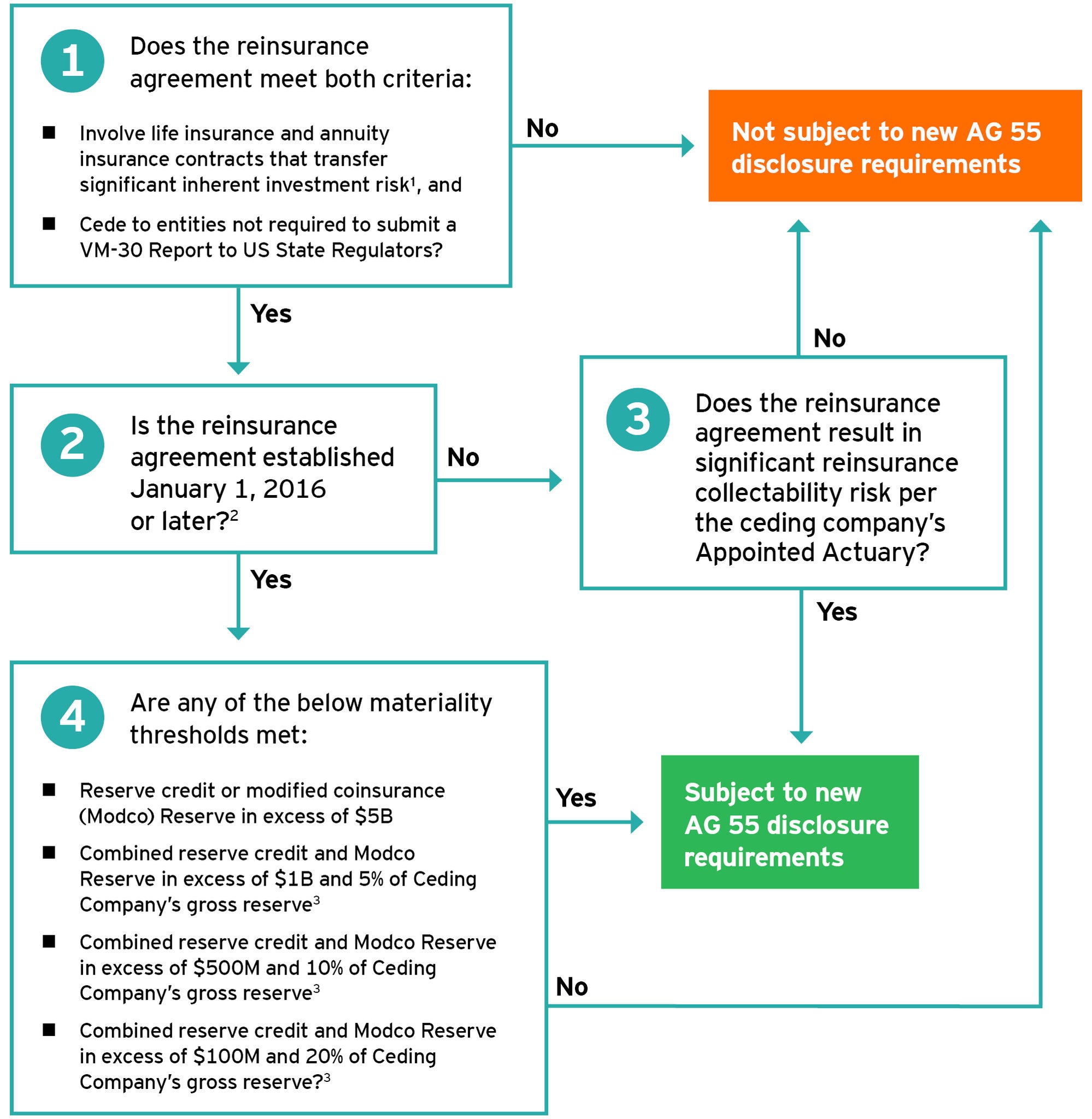

During the development of AG 55, regulators expressed an interest in minimizing additional work by US ceding insurers when there is immaterial risk. As a result, there are a variety of materiality thresholds allowing an exemption for potential in-scope transactions.

Incrementally, there are other exemptions allowed for certain agreements (e.g., non-affiliate transactions meeting certain criteria, primarily comprised of older businesses) effective in 2016 through 2019 if approval is obtained from the domestic regulator.

While the asset adequacy analysis may suggest reserves are understated, AG 55 does not require that additional reserves are posted; rather it is a disclosure-only requirement. Separately, the ceding insurer’s appointed actuary assesses whether additional reserves are necessary and clearly communicates that in the actuarial opinion filed with the domestic regulator.

Highlights of the asset adequacy analysis

While the extent of the asset adequacy analysis will depend on the associated risk of the transaction, cash flow testing (CFT) of the post-reinsurance reserve¹ is the base requirement under AG 55. CFT is an actuarial methodology used to evaluate an insurer’s ability to meet its future financial obligations using reasonable assumptions under moderately adverse conditions.

For lower-risk reinsurance transactions, there are other acceptable methodologies for asset adequacy analysis such as gross premium valuation or attribution analysis. While the guidance does not define lower-risk in this context, it is expected the appointed actuary will apply professional judgment relative to the requirements in AG 55. The appointed actuary determines the methodology to use based on the risk of the agreement, and that decision may require approval by the domestic regulator.

The asset adequacy analysis will assist regulators in better understanding when reinsurance transactions cause the post-reinsurance reserve to be less than the pre-reinsurance reserve². This may be the case when the assuming entity establishes reserves in a non-US regime.

A key component of the CFT is to determine the starting asset amount, which represents those assets included in the CFT scenarios at the beginning of the projection period. Generally, it is expected that a lower starting asset amount will result in a greater chance that the ending surplus in the projection is lower (or negative), which would likely result in an actuarial determination that recognition of additional reserves would be prudent. The starting asset amount is reduced by guideline-excluded assets. After some deliberation it was determined the guideline-excluded assets include non-admitted assets (even those permitted to be admitted by the ceding insurer’s domestic regulator), letters of credit and parental guarantees, among others identified in the guidance.

For year-end 2025, asset adequacy analysis will be aggregated by counterparty. However, for year-end 2026, cash flow testing should also be performed separately by significant product lines, similar to other existing actuarial aggregation standards.

Future implications of the new reinsurance regulatory requirements

There may be a significant effort needed in performing the CFT analysis required for certain ceded asset-intensive reinsurance transactions. As a result, insurance companies should immediately:

Educate actuarial, reinsurance and accounting personnel on the new requirements and key terms in AG 55.

- Evaluate existing ceded reinsurance transactions on whether they are in scope of AG 55 or if there is the potential to obtain a scope exemption, including in some cases through discussions with the domestic regulator.

- For those agreements in scope, evaluate for potential issues in performing the CFT analysis, such as data limitations from the reinsurer and the impact of guideline-excluded assets.

- Develop a strategy now to consider any blocks anticipated to be deficient in the analysis.

- Evaluate if certain reinsurance transactions are lower-risk with alternative approaches for asset adequacy analysis, such as attribution analysis.

- Consider the impact of the requirements on all new reinsurance transactions.

Finally, insurance companies should continue to monitor for additional developments from the NAIC related to asset adequacy analysis. This year, the NAIC is expected to adopt AG 55 templates to be used for the year-end 2025 filings. Additionally, as state insurance regulators evaluate the results of the year-end 2025 filings, there may be further changes to the AG 55 requirements that could expand the mandates for ceded reinsurance beyond a disclosure-only requirement.