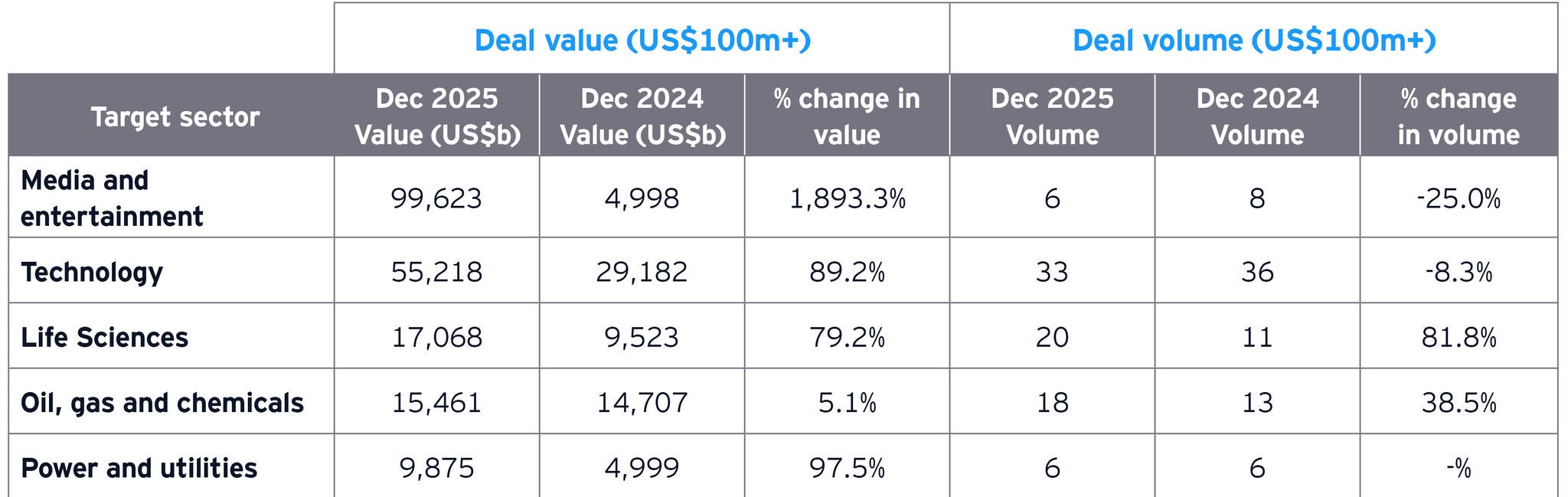

Sector highlights

M&A market activity in December reveals a blend of high-value transactions across sectors:

Media and entertainment

Deal activity reflected a lower transaction count (down 25% YoY) but a pronounced increase in aggregate deal value (up 1,893% YoY), primarily driven by a single large transaction (US$82b). Strategic buyers prioritized content ownership and direct-to-consumer scale, alongside portfolio simplification through spin-offs and split-offs. The month also reflected continued interest in evergreen IP and branded content with long monetization runways.

Technology

Tech M&A recorded a strong jump in deal value (up 89% YoY) alongside a mild softening in M&A activity (down 8% YoY) on account of fewer but higher value (US$1b+) deals. Key drivers included accelerating AI adoption across industries, demand for scalable data architectures and continued consolidation to secure critical IP and talent in high-growth technology segments.

Life sciences

The sector posted robust gains in deal value (up 79% YoY) as well as a surge in deal volume (up 82% YoY). Strategic buyers concentrated on strengthening late-stage pipelines, expanding specialty disease portfolios and securing differentiated biologics manufacturing capabilities. Private equity (PE) participation remained selective, targeting medical technology platforms with stable cash flows.

Oil, gas & chemicals

The sector experienced a marginal uptick in deal value (up 5% YoY) and a healthy expansion in deal activity (up 39% YoY), mainly driven by continued consolidation across upstream and midstream assets. Strategic acquirers prioritized scale in core producing regions, integration of midstream infrastructure and upgrading the portfolio to improve capital efficiency.

Power and utilities

Growth in deal value nearly doubled in the sector (up 98% YoY) while M&A activity remained flat, anchored by investments across renewable generation, next-gen energy technologies and grid-scale assets. Key drivers included accelerating decarbonization mandates, rising power demand from data centers and electrification and growing investor appetite for scalable, tech-enabled energy infrastructure with long-term cash flows.

Looking ahead

The US M&A landscape was initially expected to maintain its momentum, supported by favorable macro conditions, abundant corporate and PE capital, and strategic imperatives to consolidate in high-growth sectors. However, escalating geopolitical tensions are increasing risks and contributing to oil price volatility, which may dampen cross-boarder deal sentiment, particularly in the energy and industrial sectors. In this evolving environment, dealmakers will likely need to account for heightened regulatory scrutiny, especially in strategic technologies, energy supply chains and defense-linked industries.

PE firms are entering 2026 with record-high dry powder, exceeding US$3.2t globally, including over US$1.1t allocated for buyout transactions, which will serve as a strong tailwind for M&A activity.

Large-cap momentum and AI-driven investment theses are likely to persist, while midmarket activity gradually reopens as valuation gaps narrow. Sectors such as technology (AI, data infrastructure, cybersecurity) and life sciences (Medtech, services) are expected to remain active, with carve-outs and portfolio reshaping continuing to drive M&A trends.