EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

-

Helping top leaders to achieve peak performance, professionally and personally, by providing insights and networking opportunities.

Read more

Volatility is now structural, not an environment of one-off disruptions that can be easily resolved and mitigated, said Adam S. Posen, President of the Peterson Institute for International Economics, who spoke virtually in a roundtable of COOs from market leaders across sectors organized by the EY Center for Executive Leadership (CEL). We see that disruption in trade policy, in which the map of global alliances is being redrawn, and in actual wars, in which longtime adversaries have rekindled their animosities — all while artificial intelligence upends our notions of what’s possible.

“Every time you think you’ve figured it out, something new pops up,” said Kristin Valente, EY Americas Chief Client Officer. “I think it’s a great time to be testing our scenario-planning skills. And as C-suite executives, we must think about our functions and remits but also how we’re collaborating with our peers in our organizations and ecosystems.”

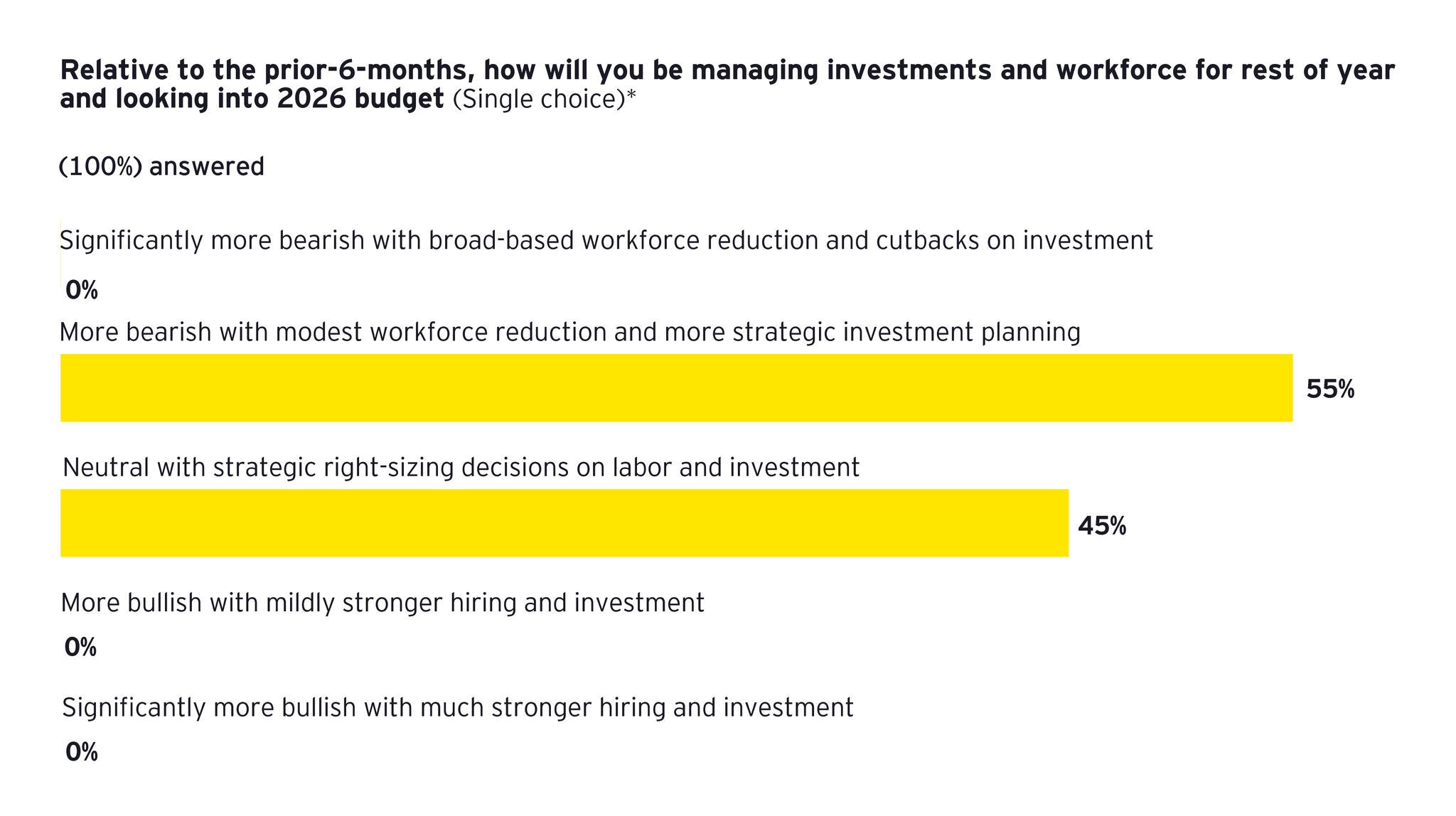

Echoing sentiment from other C-suite leaders, these COOs at the roundtable have a cloudy economic outlook, with 55% saying they were more bearish as they look toward the rest of the year and into 2026, citing modest workforce reductions and more strategic investment planning. The rest were feeling neutral, with strategic rightsizing decisions on labor and investments.

Juan Uro, EY Americas Leader for the CEL, noted that these results were identical to those from recent roundtables of Fortune 250 CFOs, CIOs and CAOs. “The sentiment you’re echoing is uncertainty for the second half, and you end up being a little more conservative,” he said.

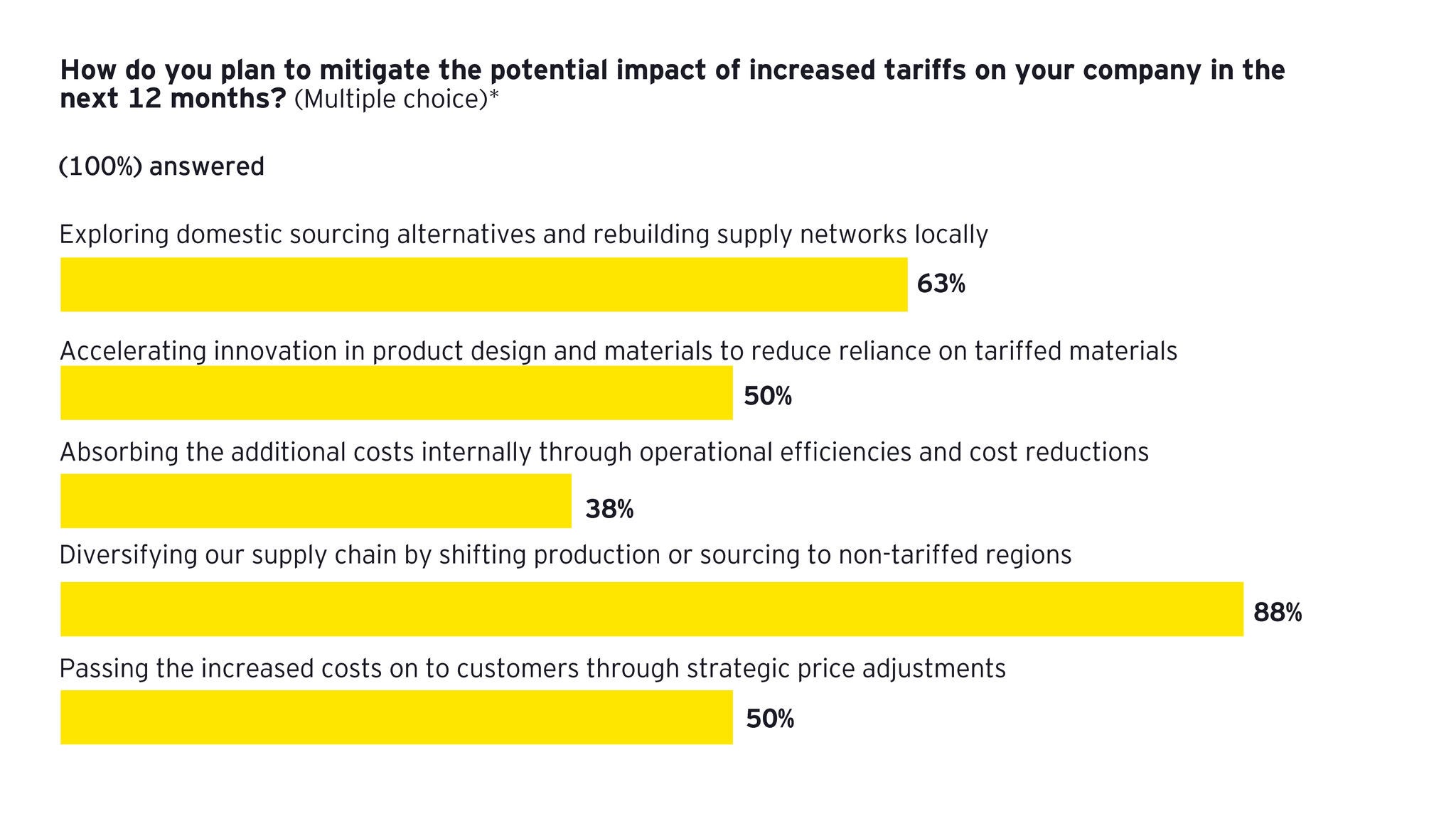

How do you tackle what’s next in a world that, in many respects, is attempting to unwind many of the dominant economic schools of thought that executives have followed their whole careers? Today, virtually every CEO in a recent EY survey is concerned about tariff impacts and trade policies — and meanwhile, weather disruptions and cybersecurity risks are taking tolls on supply chains in the tens of billions of dollars, while emerging technologies such as AI add another complex layer of disruption. Here is how supply chain leaders are assessing today to prepare for tomorrow in areas such as borders and tariffs, geopolitics, and AI.