Sector highlights

M&A activity in the last three months, compared with the same period last year, showed significant growth in the deal value across most of the following sectors.

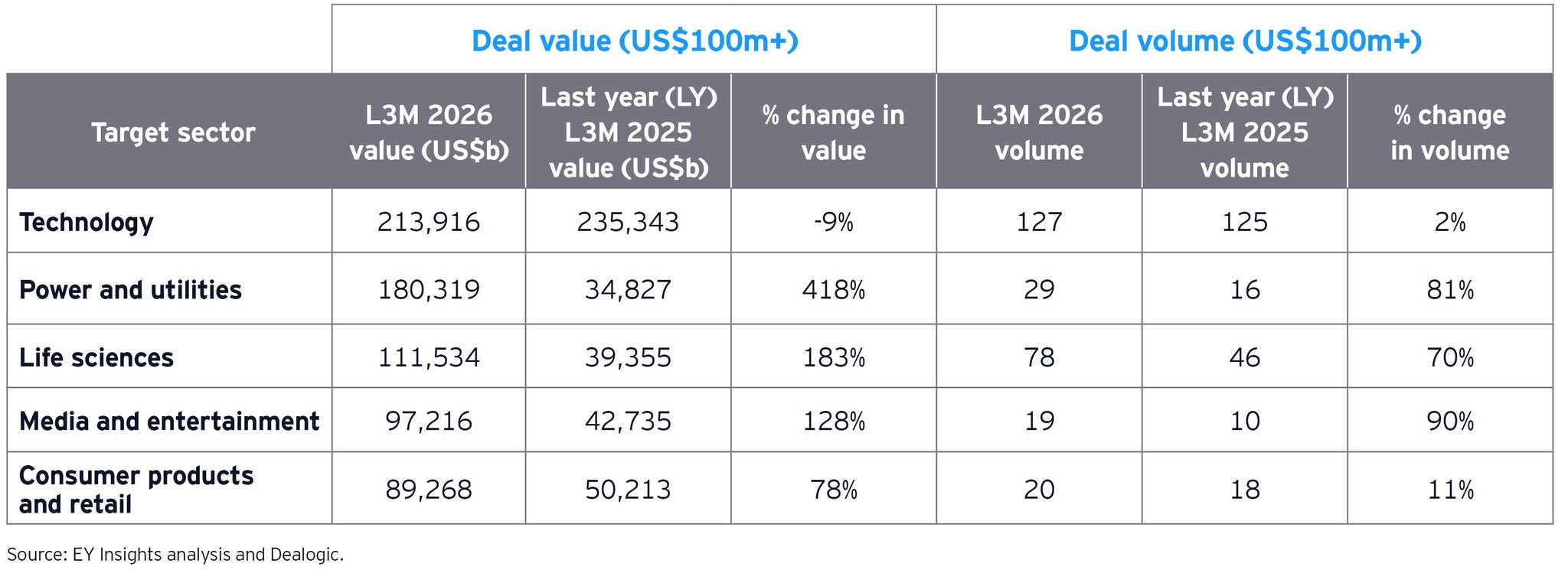

Power and utilities

M&A deal values surged 418%, largely skewed by one acquisition (including debt), which materially lifted the aggregate value in the period. Volumes also rose 81%, pointing to a broader pickup in activity. Buyers focused on scaled regulated utility platforms, dispatchable generation and integrated power infrastructure linked to rising data center and electrification demand.

Life sciences

The M&A momentum continued, with deal values up 183% and volumes rising 70%, reflecting sustained strong strategic activity. The M&A activity reflected stronger interest in platform-enabling technologies that improve delivery, manufacturing efficiency and modality control. Buyers prioritized differentiated therapeutic platforms, clinically de-risked pipeline assets and commercial-stage products.

Media and entertainment

M&A accelerated sharply, with deal values up 128% and volumes rising 90%, driven by strong strategic activity across content, rights and live entertainment assets. Activity pointed to growing interest in unlocking value through simpler capital structures and renewed public market repositioning. Buyers focused on scaled music and entertainment businesses; recurring revenue assets; and platforms with stronger monetization, distribution and customer cross-selling potential.

Consumer products and retail

M&A activity in the sector remained healthy, with deal values up 78% and volumes rising 11%, reflecting continued interest in scaled assets with stronger margin potential. Buyers targeted category leadership, specialty ingredients, premium brands and multichannel distribution platforms, while also pursuing carve-outs and lighter operating models that sharpen the portfolio focus and improve monetization.

Technology

M&A activity was broadly stable by volume, with deal activity up 2%, indicating continued strategic interest alongside more selective capital deployment. Activity pointed to a stronger push toward vertical integration, capacity control and adjacency expansion in data center and electrification-linked ecosystems. Buyers concentrated on AI-enabling infrastructure, proprietary data assets and workflow platforms that deepen enterprise embedment.

Looking ahead

The US M&A market is expected to remain active, with ~8% growth forecast in the 2026 deal volume for transactions over $100m, supported by demand for AI-ready capabilities, stronger market positioning and ongoing portfolio reshaping. Corporate M&A is projected to lead this recovery as strategic buyers continue to use acquisitions and divestitures to accelerate access to technology, talent and operating capabilities.

At the same time, the backdrop for deal execution has become more complex. Evolving inflation dynamics, geopolitical uncertainty and ongoing supply-side pressures are introducing greater variability into capital allocation decisions, financing conditions and cross-border transactions. However, rather than slowing activity, these forces are reinforcing a more disciplined approach. Organizations are using M&A not as an opportunistic lever but as a deliberate tool to reshape portfolios, build scale and access differentiated capabilities. This is evident in the continued focus on horizontal integration, portfolio rationalization, and targeted investments in platform-driven and technology-enabled assets across sectors.

While confidence is improving, it remains selective and uneven, with continued strength in large-cap strategic transactions alongside a more measured recovery in mid-market activity.

Overall, 2026 appears set to be a year of resilient but disciplined dealmaking. Large strategic transactions and tech-driven investment themes are likely to remain active, alongside the growing momentum in FinTech, data, pharmaceuticals and industrials.

In this environment, outcomes will increasingly depend on disciplined execution, including a clear deal thesis definition, robust capital allocation and early integration planning to ensure value realization.