EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Trending

Select your location

Local sites

As discussed in our previous EY alert dated 25 November 2022 (VAT deduction under the direct attribution method: important changes from 2023), mixed taxable persons are from 1 January 2023 required to submit an electronic notification in order to opt for the deduction of VAT according to the real use method. They are also required to provide certain information on how to exercise the right to deduct VAT.

This notification can be done in the updated e-604 application which is now accessible via MyMinfin.

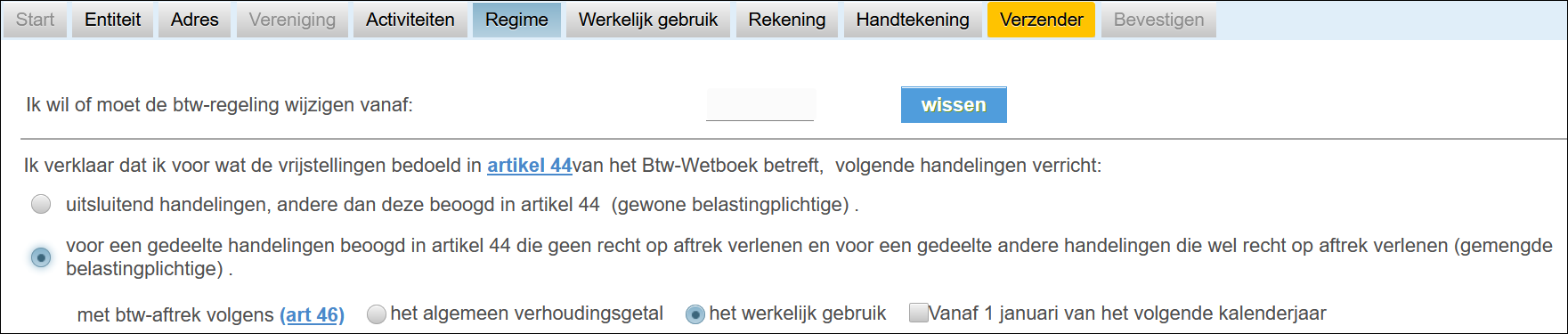

For taxable persons that were already applying the real use method on 31 December 2022, a declaration in the amending form e-604B must be completed and submitted before 1 July 2023. The date from which the real use VAT deduction method is applied must be entered under the new “Affectation réelle” or “Werkelijk gebruik” tab of the new e-604 form:

For taxable persons who do not yet apply this scheme, the e-notification should be done before the end of the first VAT declaration period (month or quarter) of the current calendar year or before the end of the first declaration period following the start or modification of the activity.

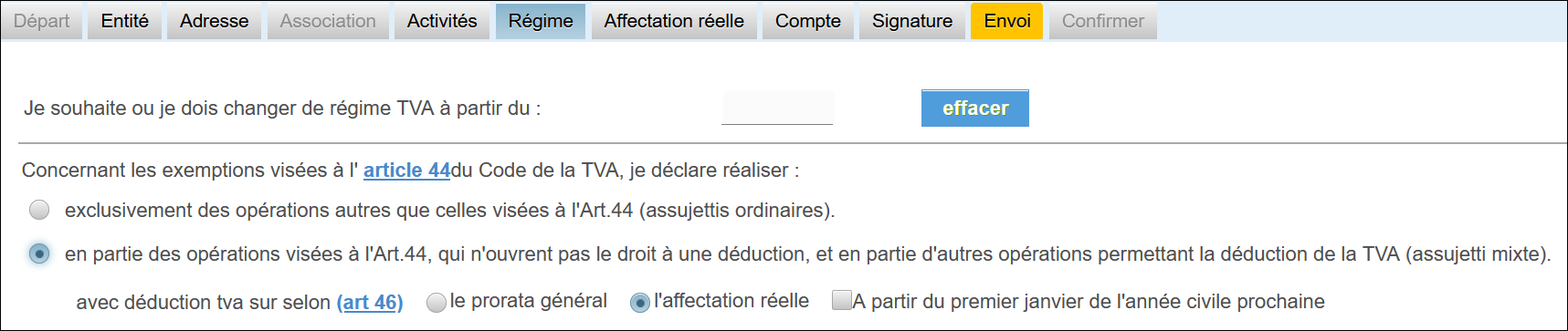

The notification can be made by completing the “Régime” or “Regime” tab of the new form e-604A (for mixed taxable persons starting their activity) or e-604B (other mixed taxable persons). Taxable persons are requested to indicate the date from which they wish to start or to change their VAT scheme and to indicate that they wish to opt for the real use method:

It is important to note that if the above deadlines have not been met, the real use method cannot be applied until 1st January of the following calendar year. Especially for taxable persons who wish to benefit from this regime for the first time as from 01/01/2023, actions will have to be taken very soon.

As regards the information that must be communicated in the periodic VAT return via Intervat, a tolerance has been foreseen for the 2023 deadlines.

If the taxable person is already applying the real use method on 31 December 2022, then these data must be reported when submitting the periodic VAT return for:

- the first quarter of 2024 (to be submitted by 20 April 2024) or;

- the month of May 2024 (to be submitted by 20 June 2024) at the latest.

For the taxable persons that want to start applying the real use method in the course of 2023, the data should be reported when submitting the periodic VAT return for:

- the first quarter of 2024 (to be submitted by 20 April 2024 at the latest) or;

- one of the first three months of 2024 (to be submitted by 20 February, 20 March, or 20 April 2024).

See also: