EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

The Belgian customs authorities have gradually updated the timeline of the Multi-Annual Strategic Plan (“MASP”), including a.o. new go-live dates for the digitalization of the export, import and transit processes. As a result, export declarations can no longer be lodged in PLDA and for import declarations PLDA will be phased out. Additionally, the fifth phase of NCTS will be implemented with a big bang in January 2025.

This shift may have significant consequences for customs brokers & businesses engaged in export and/or import activities. Businesses are affected as they bear the ultimate responsibility for the accuracy & completeness of the declarations submitted on their behalf, for which new data elements may have to be provided to the customs authorities.

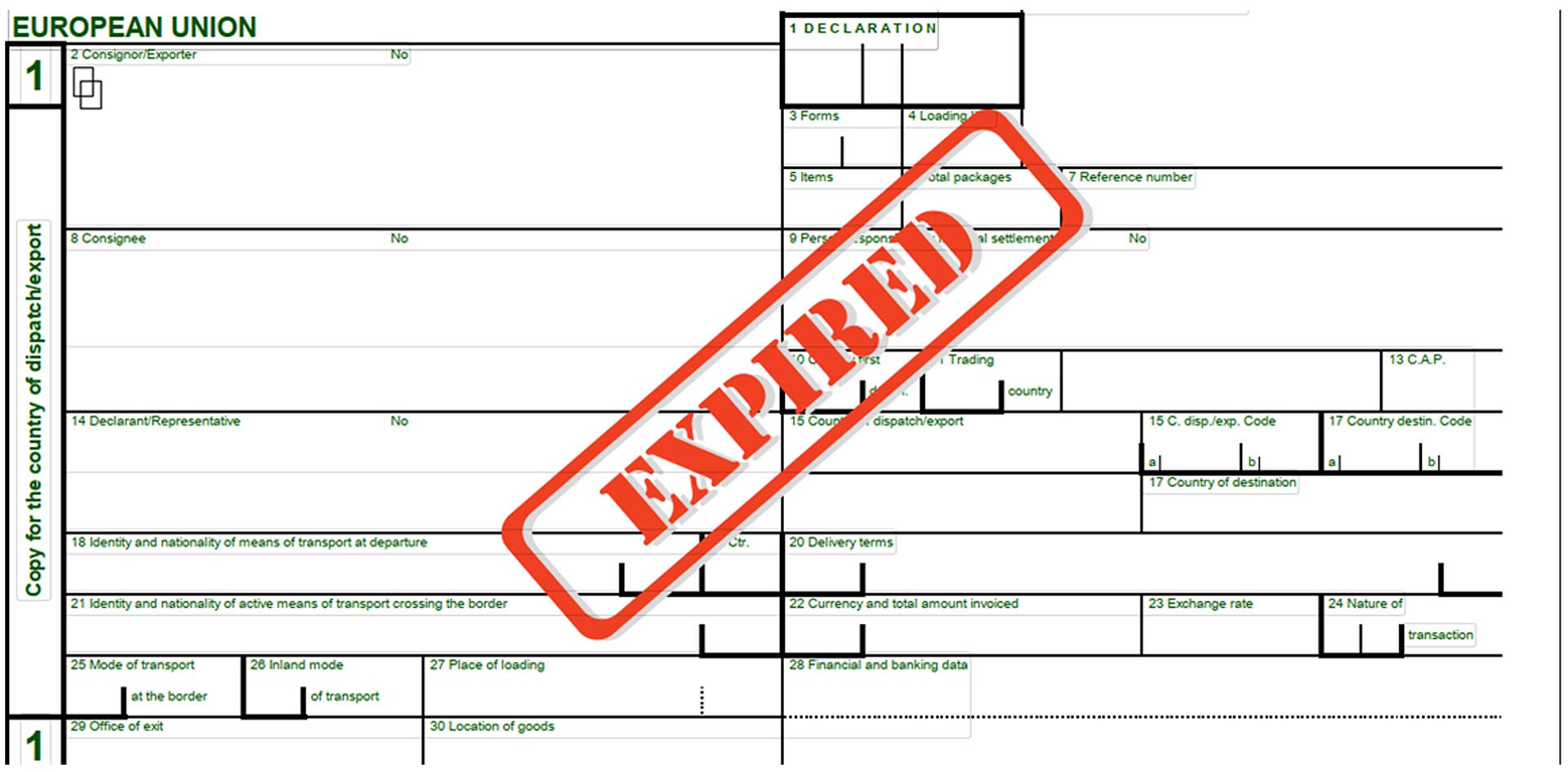

Also, from a VAT perspective the impact is significant. All future import & export customs declarations will be made fully electronically. As a result, the new customs import/export declarations will no longer be provided in official paper- or PDF-format. The previously known Single Administrative Document (“SAD”), as underlying formal proof for your import VAT recovery or to substantiate your VAT exemption for export of goods, will fully disappear.

- Are you fully informed about the implications of the recent changes on your customs & VAT operations and how to address them effectively?

- Are you aware that new data elements may have to be provided?

- If you import/export in other EU Member States, are you aware of the local MASP timeline?

- If you receive(d) monthly consolidated PLDA reports, are you aware that you might no longer receive them in the same format going forward?

- Without a formal export document (SAD), have you considered which alternative documentation you would have available to prove your VAT exemption for exports of goods? Have you validated whether that documentation would effectively be sufficient from the local VAT authorities’ perspective in the Member State of export?

- Have you already done a review whether the exporter of record for customs and accordingly for VAT purposes (i.e. the party applying the VAT exemption for export) is correctly captured in the new boxes of the electronic export declarations, to avoid discussions on the application of the VAT exemption upon a VAT audit?

- Without a formal import document (SAD), have you considered which alternative documentation you would have to prove the validity of your import VAT deduction & any self-assessed import VAT figures in your VAT returns? Have you validated whether that documentation would effectively be sufficient from the local VAT authorities’ perspective in the Member State of import?

- Are you aware that in some countries (e.g. Belgium) you might be required to setup specific access to online portals to gather the correct monthly import data overviews for VAT reporting purposes?

In addition to the aforementioned points, there are further impacts on your operations that need to be considered. To address these, we will be organizing a webinar on customs digitalization in early 2025. An official invitation with all the details will be sent out soon. This webinar will cover important updates and provide valuable insights into how digitalization can affect your customs operations.

In the meantime, we would be happy to set up a call to discuss the impact on your indirect tax operations. We can support you to avoid any adverse indirect tax consequences & secure your import VAT recovery and/or export VAT exemptions.

At the beginning of 2025 the Global Trade team will organize a webinar regarding this topic. Stay tuned and visit our EY webcasts | EY - Belgium page to register.