EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

-

EY Family Enterprise Business Services is designed to help enterprising families grow larger, more valuable businesses that will last for generations. We can help you develop and implement a plan for growth, generational transition and shareholder liquidity.

Read more

On the lending side, balance sheet asset risk exposure, stemming from commercial real estate loan write-downs and deposit withdrawals, has impacted bank liquidity, tightened credit acceptance and curtailed lending activities. In turn, many alternative lenders face challenges with existing portfolio companies.

Businesses are facing internal capital challenges as well. Inflation and other supply chain factors have impacted gross margins and operating income, capital budgets have been slashed in the B2B market, and cap rates for real estate valuations have deteriorated. The fear of recession has also limited capital market access for many businesses.

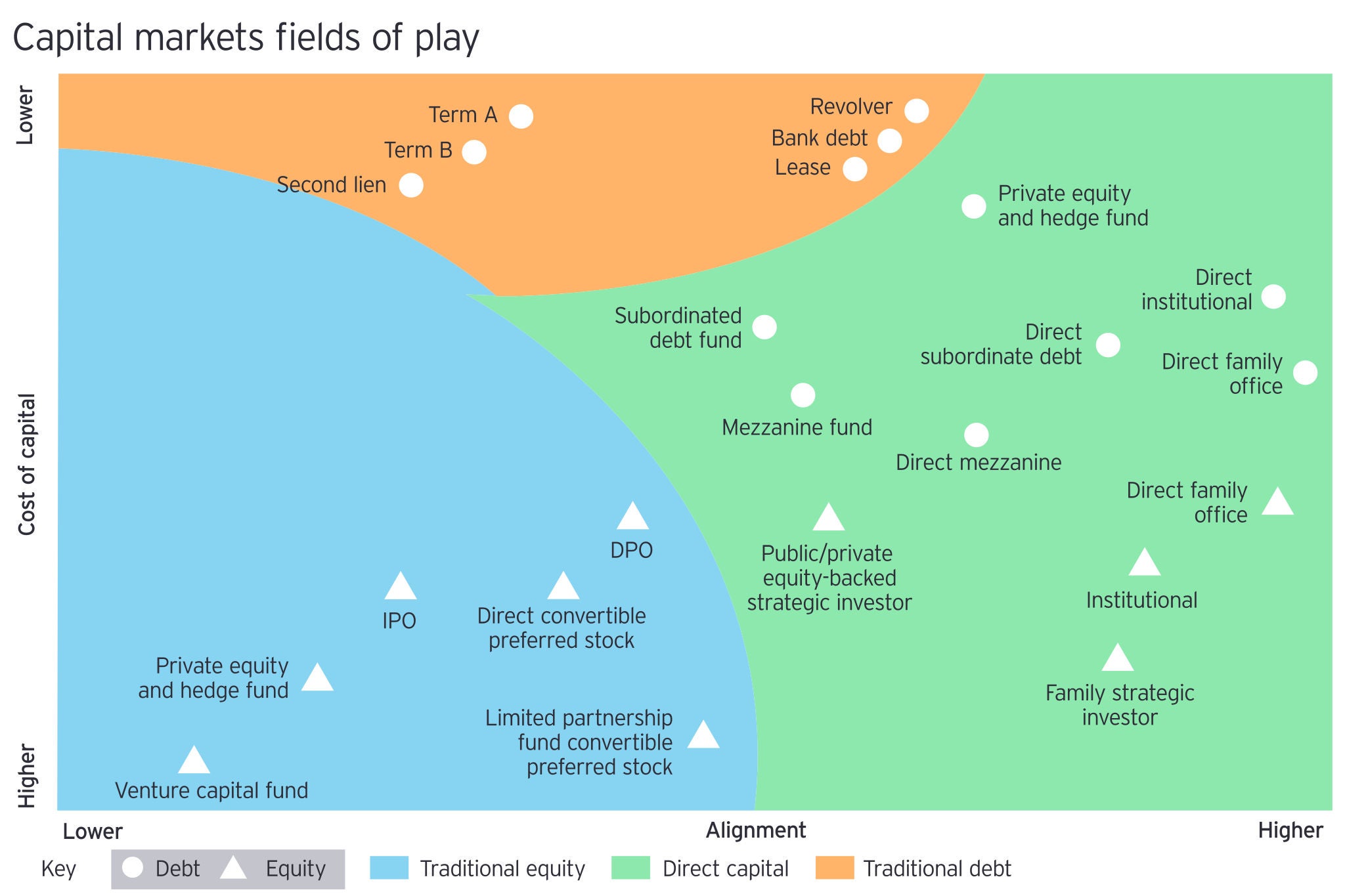

It’s clear that the rules of the game have shifted in today’s capital markets, so many family businesses are looking at how to re-evaluate their company capitalization plans. As part of that process, they need to better understand how the capital markets have changed, as well as how their business would be assessed by participants in the capital markets. In this way, they can better quantify their capital availability and more accurately calculate the cost of capital.

Here are some tools to consider before developing your capitalization plan:

- Business Value Range Analysis (VRA) calculation tools

- Credit Quality & Capacity Assessment data and analysis

- Capital Market/Credit Placement Assessment research

- Capital Market Qualification (CMQ) Scoring data and tools

- Capital Markets Trends (CMT) Assessment data

- Weighted Average Cost of Capital (WACC) Recalculation data

- Upgraded Financial Planning & Analysis (FP&A) Modeling tools

- Business Reinvestment & Capex ROIC Analysis Prioritization tools and processes

- Liquidity Profile & Enterprise Risk Forecasting data and tools