EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Trending

-

Unlocking agentic value: a new investment discipline for the agentic era

01 Jun 2026 Consulting -

Jitendra Mohan, Sanjay Gajendra and Casey Morrison from the United States named EY World Entrepreneur Of The Year™ 2026

29 May 2026 Entrepreneurship -

How AI drove Daikin’s business transformation from complexity to agility

08 May 2026 Alliances

As gold demand surges, miners are leveraging high prices for growth while prioritizing ESG due to the metal's rising investment appeal.

In brief

- Price momentum has incentivized gold miners to invest in enhancing their asset base through exploration and M&A activities.

- Companies strive to adopt responsible gold mining practices, focusing on initiatives to improve their emissions profile and address social challenges.

- Miners are looking at economic extraction of lower grades and digitalization to drive long-term value.

This article is authored by Dean Braunsteiner, EY Canada Mining and Metals Assurance Leader.

In 2023, higher-than-usual gold prices incentivized gold companies to expand their resource base and make their operations more sustainable. Gold dominated commodity exploration budgets, and companies closed on large asset transactions with a renewed focus on organic and inorganic growth. Market momentum supported margins, while cost inflation headwinds raised overall AISC to surpass the previous highs.

The overall annual demand for gold increased 17% year over year to 4,699 t in 2022, reaching an 11-year high, with heavy central bank purchases, an uptick in retail investments and a slowdown in ETF outflows. However, demand for gold in the first nine months of 2023 decreased 3% year over year to 3,286 t, with a drop in investments due to large ETF outflows, yet above the three-year average demand over the same period in 2021.¹

Adoption of innovation in existing operations through digitalization and electrification initiatives is expected to drive cost and operational efficiency. The rising number of low-grade gold deposits makes it essential for gold miners to explore economically and environmentally friendly methods of metal extraction. Sustainable production profile is likely to further position gold as a preferred investment asset among investors even more than its existing safe haven characteristics.

Gold miners’ current focus

Profitability is propelling miners in the direction of aggressive M&A

Though the gold deal count dipped from 133 in 2021 to 118 in 2022, overall deal value increased 58% year over year to US$21.5b in 2022.² With slight moderation in inflation rates compared to the previous year and changes in interest rates in 2023, mid-cap gold miners are aiming to scale up and capitalize on operational synergies, banking on high gold prices and robust margins.

Major gold deals in 2023 included Pan American-Agnico Eagle’s acquisition of Yamana Gold with a cash and stock offer worth ~US$4.8b to expand its operations in Latin America and consolidate Yamana’s ownership of its Malartic, Québec operations.³

Annual average AISC surpassed all-time highs of 2012 to reach US$1,276/oz

Higher inflation than before the pandemic, along with supply disruptions, influenced mine-site costs such as labour, fuel and electricity over the past quarters. The average all-in sustaining costs (AISC) for gold increased 18% year over year to US$1,276/oz in 2022, surpassing the previous records of 2012.⁴

These costs further rose and averaged at US$1,337/oz in the first half of 2023 increasingly putting high-cost gold mines under operational stress of temporary closure or production cuts.⁵

On a regional basis, the Americas is expected to remain a high-cost region, with AISC to average at US$1,299/oz in 2023 due to rising labour and fuel costs.⁶

Gold is likely to dominate exploration, with 46% total budget allocation

Overall gold exploration budget in perspective is expected to reach US$5.9b in 2023, down 16% year over year from the nine-year highs of 2022, yet comprising 46% of the overall exploration budget.⁷

The major companies’ gold allocations are likely to total to US$2.9b, just above the juniors’ budget of US$2.3b, with both accounting for 87% of total gold allocations.⁸

Exploration activities in the year continue to be more focused towards mine site and last-stage projects compared to grassroot ones.

Regionally, Canada is expected to record the highest share of 23% of the total 2023 gold budget, amounting to US$1.4b, followed by Australia and Latin America.⁹

Central bank purchases registered 14% year-over-year growth to 800t in the first nine months of 2023, driving another notable year of net buying

Central bank purchases recorded 55-year highs, with 140%year-over-year growth to 1,082 t in 2022, primarily supported by emerging markets, including Turkey and China. Continuing the trend, central bank buying increased 14% year over year to 800 t in the first three quarters of 2023. However, investments declined 21% to 687 t year to date with ETF outflows.¹⁰

In terms of physical demand, jewelry consumption declined 3% to 2,090 t in 2022 due to high local prices of gold in markets like India and Turkey, and COVID-related lockdowns in China.¹¹

Jewelry demand remained flat in the first three quarters of 2023 compared to the same period in 2022, with persistent economic uncertainty and price pressures on consumers.

While technology demand for gold dropped 6% in 2022 and 9% in the first nine months of 2023, with trade restrictions, supply chain issues and dipping consumer demand amid a deteriorating global economic backdrop.¹²

Miners are advancing ESG reporting to increase transparency for primary and secondary investors

As gold gains popularity as an investment asset, miners are increasingly expected to enhance their ESG reporting practices. To avoid errors in sustainability reporting, miners actively track and analyze high-quality ESG data, with strong governance and controls to ensure appropriate signoffs.

Some miners have adopted ESG tracking solutions to collate and validate data digitally; for instance, Eldorado Gold has employed an ESG solution that helps the company log, approve and report datapoints in a manner relevant to various reporting frameworks.¹³

Next steps for miners to steer the transition

Adoption of responsible gold mining principles drives adherence to sustainable development goals

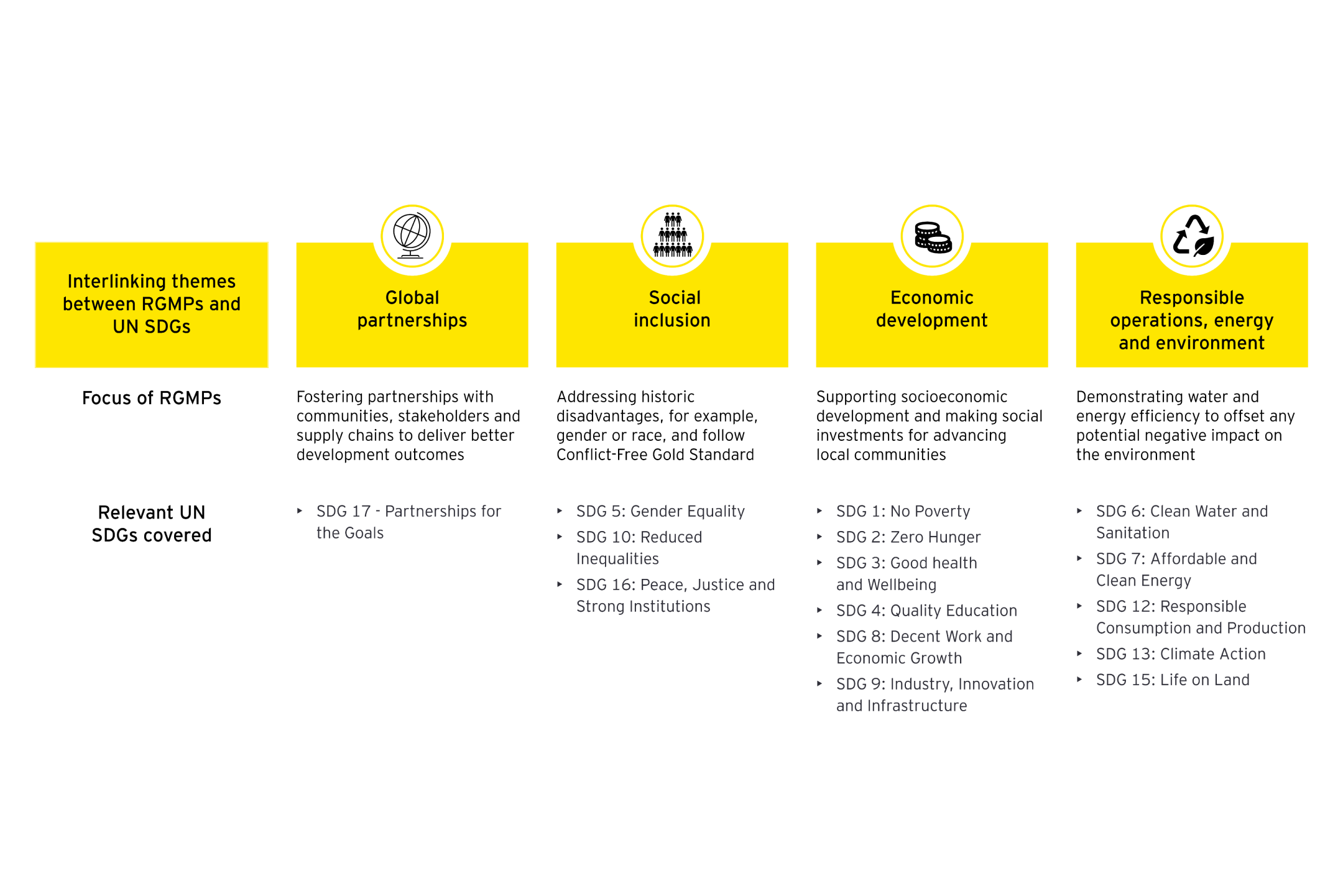

Gold companies that implement the World Gold Council’s Responsible Gold Mining Principles (RGMPs), indirectly contribute to a variety of the UN Sustainable Development Goals (UN SDGs) due to close interlinkage between the two standards.¹⁴

Source: EY Knowledge Analysis of World Gold Council Report

Major miners can work with local governments to formalize and improve the status of artisanal and small miners

Artisanal and small-scale gold mining occurs in more than 80 countries, sustains the livelihoods of 15m to 20m people and accounts for 20% of annual newly mined gold supply.¹⁵ Mismanagement of its coexistence with the mining ecosystem can significantly impact competitiveness in gold sector. Local governments play a pivotal role in determining the optimal interface between small and large miners and formalizing their status to improve existing social rights.

Large gold companies can help small miners by facilitating their access to markets, enhancing social development, providing training and improving health and safety practices. For example, B2Gold proactively manages exposure to small miners in Mali, the Philippines and Colombia with site-level initiatives being pursued including regular monitoring and reporting activities and environmental impacts, purchasing and processing ore extracted by small-scale miners outside mining areas to diminish mercury use (Philippines) and considering small miners interests during closure planning.¹⁶

Gold companies can reduce their climate change impact and move towards carbon neutrality

Though the gold industry’s carbon footprint accounts for approximately 0.4% of global annual emissions, miners can adopt multiple cost-efficient pathways to manage their overall sustainability profile.¹⁷

For example, Canadian gold miner Mayfair Gold purchased carbon offsets for 738 t CO2 equivalent (CO2e) GHG emissions produced, thereby making its Fenn-Gib gold exploration project carbon neutral.¹⁸

Unlocking gold’s decarbonization potential will amplify its role as a safe haven asset, hedge, portfolio diversifier and a store of value amid market stress.

Green financing gains popularity in the gold sector

Despite persisting geopolitical and economic uncertainty, global issuance of green, social, sustainability and sustainability-linked (GSSS) bonds outperformed the 26% year-over-year drop in the broader fixed-income market, reaching US$877b in 2022.¹⁹

Miners are increasingly supporting green bonds and other sustainability-linked securities amid a proliferation of funds dedicated to ESG goals. For instance, Anglo American issued a €745m sustainability-linked bond, tied to its performance on emissions reductions, job creation and abstraction of fresh water.²⁰

What will drive business resilience beyond?

Modern networks and integrated digital systems have the potential to unlock efficiency along the value chain

Gold miners currently employ technologies such as the Internet of Things (IoT), sensors, autonomous vehicles, drones and digital twins to enhance safety, ease mine prospecting and establish predictive mechanisms. Adoption of upcoming modern and sophisticated digital tools can improve the ability to monitor processes and key performance indicators, create a virtual physical world and support decentralized decisions.

Recently, Gold Fields deployed a comprehensive digital platform provided by ABB at its Granny Smith mine to unify planning, maintenance and production, improve productivity and streamline data flow to enable timely decision-making.²¹

Miners can also optimize the use of autonomous vehicles with efficient network systems. A good example is Agnico Eagle’s Detour Lake and Kittila mines, where the company has implemented a 5G wireless network to increase connectivity and safety.²²

Transition towards grid connectivity and renewables can reduce emission intensity of power used in production by 35% by 2030²³

Miners are employing renewable energy sources to power mine sites and reduce GHG emissions to combat climate change. Gold companies have commissioned direct wind and solar facilities at their operations. For example, commissioning of the new 16 megawatt (MW) solar plant and additional battery storage infrastructure at Barrick Gold's Kibali mine is expected to raise overall renewable electricity supply to the mine from 81% to 85%.²⁴

In addition to the adoption of renewables, underground mines can benefit from the electrification of their fleets to enhance working conditions by reducing noise, heat and pollution levels. Further, electric vehicles unlock long-term cost benefits for miners, with carbon taxes being levied across jurisdictions.

With average grades slipping towards 1 g/t, economic extraction of lower-grade ore to be a potential differentiator

The average head grades at the world’s primary gold operations stood at 1.35 g/t in 2021, down 8% from the 10-year peak of 1.46 g/t in 2017, primarily due to rising prices and the depletion of higher-grade reserves at mature mines.²⁵ These low-grade materials translate into high costs for miners. Miners can leverage heap leaching, which can reduce recovery costs for low-grade ores due to lower energy and water requirements.

Summary

The outlook for gold over the short term is expected to be impacted by diverse factors. Geopolitical uncertainty can spur safe-haven demand, while areas with economic stability are likely to support wealth-driven purchases.

With higher gold prices, miners will continue to close M&A deals, engage in exploration activities and advance toward net-zero targets. Employment of low-cost methods of extraction and adoption of sustainable innovations will help gold companies drive competitiveness in the long term.

Related articles