EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

-

The EY Digital Operations team uses technology to help oil, gas and chemicals businesses drive operational excellence and sustainable growth. Learn more.

Read more

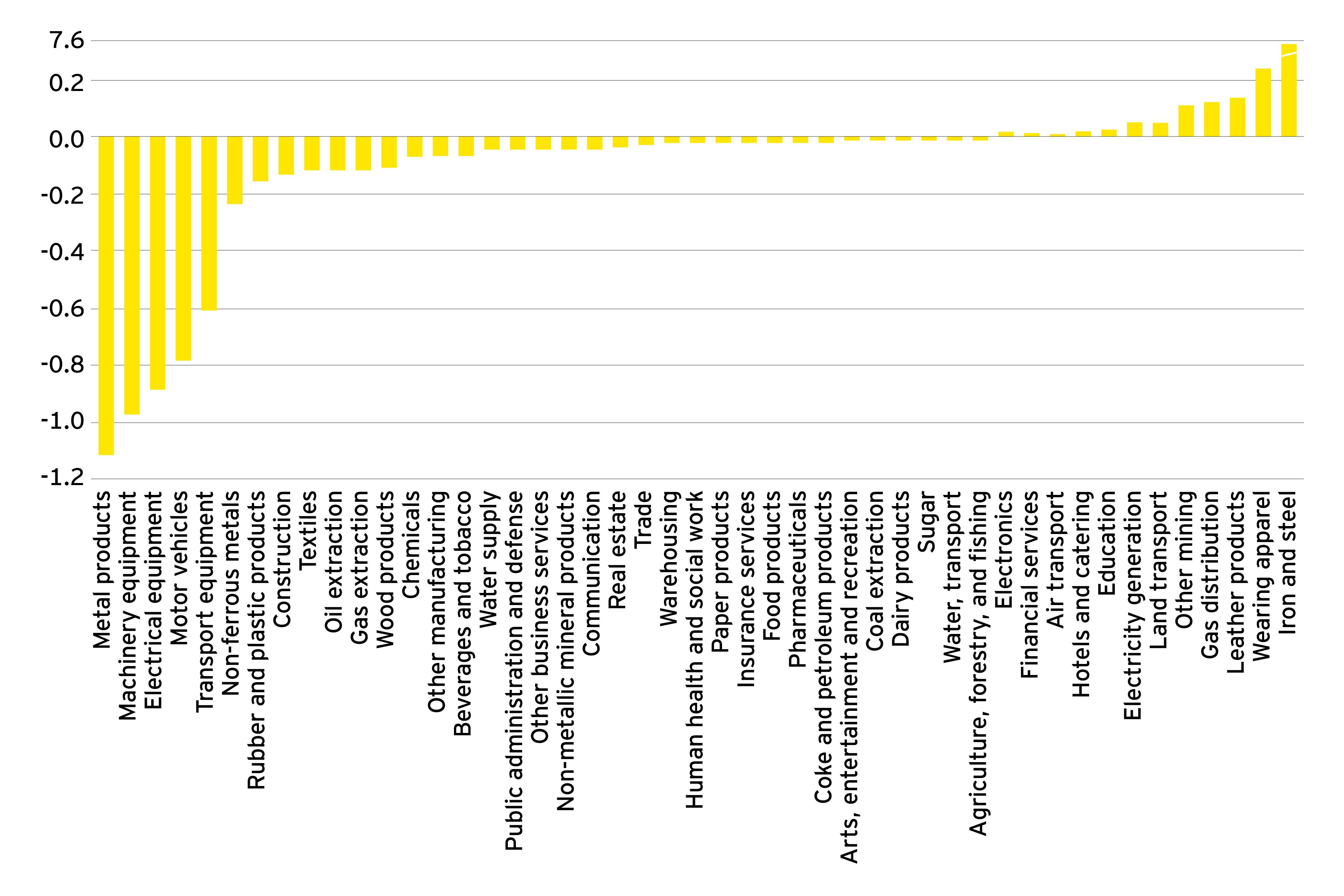

Steel or equipment as the critical input?

Steel, especially OCTG, is essential to the O&G sector. According to data from Rystad, an independent energy research company, spending on steel accounts for around 10% of upstream capital expenditures in the United States. EY economic modeling — calibrated to the models used by the U.S. Department of Commerce to justify Section 232 protection for domestic steel manufacturers initially in 2018 — finds that the costs of capital equipment for O&G extraction are expected to rise twice as much as the national average from the new steel tariffs.

By adding restrictions to the U.S. Department of Commerce model — one to account for the depreciation of capital stock across all sectors due to rising equipment prices with steel components and a second to limit the substitutability of equipment across sectors — the impacts are clear. On average, steel tariffs rose by about 19 percentage points, translating to a long-term rise of 5.6% in the costs of intermediate steel inputs for the O&G sector. However, the total impact on investment is only expected to be around -0.3%. What is driving the relatively optimistic result?

There are two explanations. First, the impact is felt most strongly by oilfield services equipment (OFS-E) manufacturers, not directly by the formal O&G sector. Second, the model assumes only steel tariffs have changed, but other factors remain the same; clearly this assumption does not reflect the current reality for O&G companies.

Looking at the channel of steel costs impacting O&G directly, the costs of O&G-specific capital goods increase by only about 0.1% more than expected, despite the imposition of the steel import duties. This is because steel comprises about 10% of the manufacturing costs of this equipment, a figure nearly matched by the manufacturing costs, and both combined are exceeded by labor costs. Consequently, the value of the underlying raw material is diluted through the manufacturing process so that steel eventually has a relatively small portion of the value captured in spending on “steel capital expenditures.”

This is not all good news for O&G, however. The EY model, which looks at the impact on output and activity in all sectors across the economy, shows a much greater impact on OFS-E and other manufacturers supplying the sector. The manufacturing of machinery, electrical equipment and metal products is expected to fall by approximately 1% compared to pre-tariff expectations.

Figure 1. Modeled impact of steel tariffs on output across US economic sectors (% change from baseline)