EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Trending

-

Unlocking agentic value: a new investment discipline for the agentic era

01 Jun 2026 Consulting -

Jitendra Mohan, Sanjay Gajendra and Casey Morrison from the United States named EY World Entrepreneur Of The Year™ 2026

29 May 2026 Entrepreneurship -

How AI drove Daikin’s business transformation from complexity to agility

08 May 2026 Alliances

Press release

03 Mar 2026

|

New York, NY, United States

EY-Parthenon Consumer Sentiment Survey reveals growing financial strain among US consumers

As financial pressure rises, consumers are cutting back on discretionary spend, switching brands to save and favoring budget retailers

EY-Parthenon practice today released findings of its latest edition of the US Consumer Sentiment Survey, revealing a growing share of consumers who report that their personal finances are on the decline, with one in four indicating they feel worse off than one month ago.

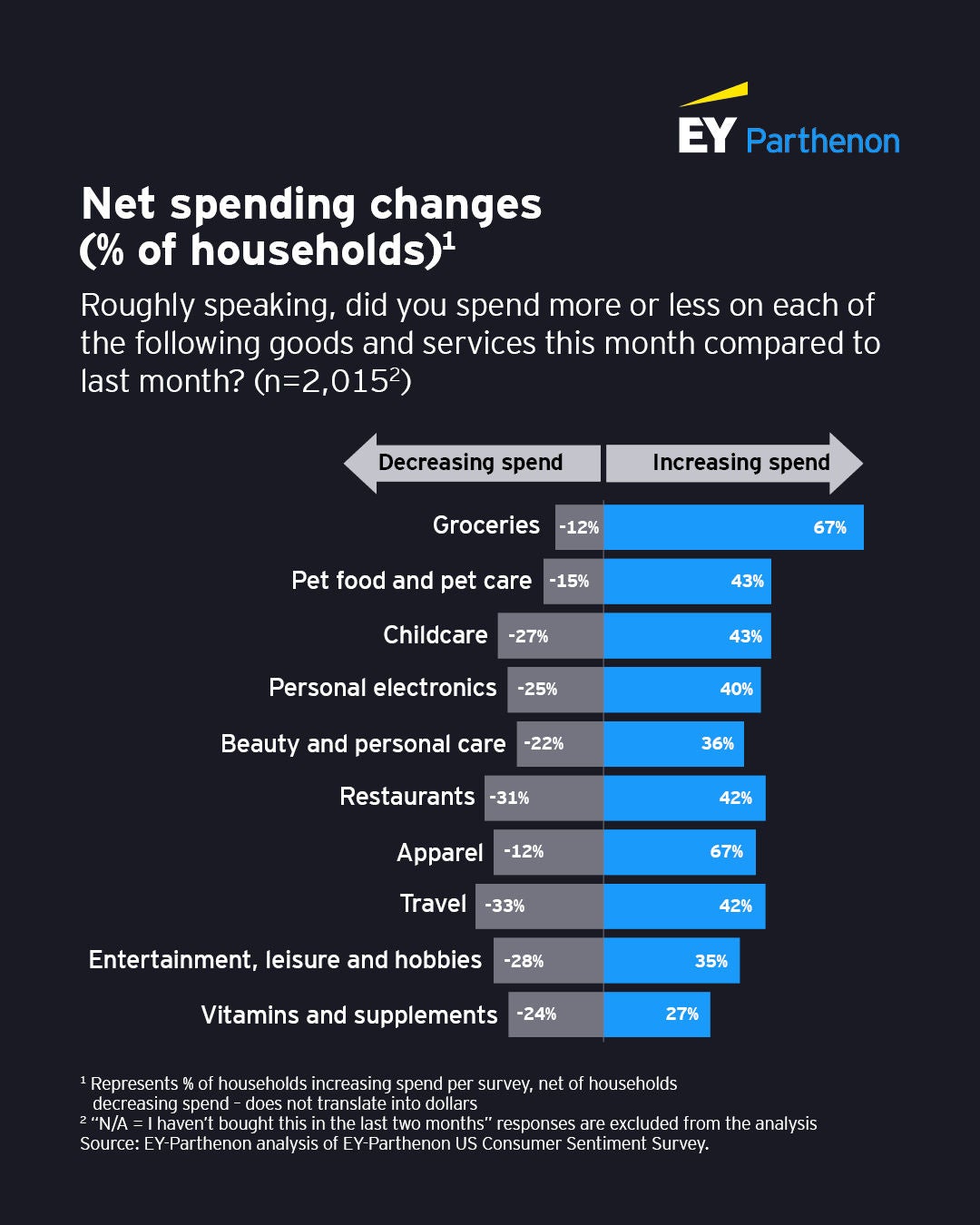

The bimonthly survey, which recorded responses from more than 2,000 US consumers in December 2025, underscores the impact of rising expenses — including groceries, housing and transportation — on shopping behavior and household budgets.

“Rising financial anxiety shows pressure is building beneath the surface,” said Mark Chambers, EY Americas Retail Sector Leader. “Reaching consumers long-term will require retailers to strike the balance between implementing cutting-edge technology and keeping human experience at the forefront. Retailers that emphasize value, convenience and affordability will be best positioned to maintain consumer loyalty in the months ahead.”

Key findings from the EY-Parthenon Consumer Sentiment Survey include:

- Financial strain is rising despite overall stability: One in four consumers feel they are worse off than one month ago, signaling mounting strain amid a still uncertain economic environment.

- Consumers prioritize essentials as discretionary spending declines: Cost-of-living concern remains elevated, particularly around groceries, which nearly 70% of respondents cite as a moderate or major concern. Discretionary categories, such as restaurants, entertainment, travel and apparel, are seeing broad pullbacks as consumers seek fast ways to reduce spending.

- Consumers across income levels are seeking value: Even high-income shoppers are paying attention to prices — primarily through shopping on sale, comparing prices and switching to private labels. In fact, 15% of consumers switched personal care brands to save money.

- Trends point to a widening gap in essential vs. discretionary spend: Consumers are more likely to switch brands or stores to save money on routine items, while they tend to stop or defer purchases entirely for more discretionary categories like apparel and footwear. Furthermore, everyday low price (EDLP) and budget retailers attracted disproportionate traffic gains in December, while higher-end and specialty retailers experienced flat or declining traffic.

“Consumers are selective, and value continues to dominate decision-making across all income levels,” said Will Auchincloss, EY-Parthenon Americas Retail Sector Leader. “These behaviors are sticking, and they will continue to shape the competitive landscape for retailers and brands well into 2026.”

“Consumers are increasingly selective, with everyday essential goods taking priority as households reassess where they can pull back,” Auchincloss added. “Squeezed budgets are pushing retailers to double down on value, pricing discipline and everyday relevance to win in 2026.”

Learn more about EY Consumer at https://www.ey.com/en_us/industries/retail

About EY

EY is building a better working world by creating new value for clients, people, society and the planet, while building trust in capital markets.

Enabled by data, AI and advanced technology, EY teams help clients shape the future with confidence and develop answers for the most pressing issues of today and tomorrow.

EY teams work across a full spectrum of services in assurance, consulting, tax, strategy and transactions. Fueled by sector insights, a globally connected multidisciplinary network and diverse ecosystem partners, EY teams can provide services in more than 150 countries and territories.

All in to shape the future with confidence.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. Information about how EY collects and uses personal data and a description of the rights individuals have under data protection legislation are available via ey.com/privacy. EY member firms do not practice law where prohibited by local laws. For more information about our organization, please visit ey.com.

About EY Consumer and Health

The rise of the empowered consumer, coupled with technology advancements and the emergence of digitally focused entrants, is changing every aspect of health and care delivery. To retain relevancy in today’s digitally focused, data-infused ecosystem, all participants in healthcare today must rethink their business practices, including capital strategy, partnering and the creation of patient-centric operating models.

The EY Consumer and Health architecture brings together a worldwide network of 34,000 professionals to build data-centric approaches to customer engagement and improved outcomes. We help our clients deliver on their strategic goals, design optimized operating models and form the right partnerships so they may thrive today and succeed in the health systems of tomorrow. We work across the ecosystem to understand the implications of today’s trends, proactively finding solutions to business issues and to seize the upside of disruption in this transformative age.

Methodology

Wave 3 of the EY-Parthenon US Consumer Sentiment Survey includes responses from 2,015 US consumers, reflecting a broad cross-section of the general population. Survey topics include personal financial confidence, spending and savings behavior, category-level spending trends, retail traffic, channel preferences, artificial intelligence (AI) usage and broader macroeconomic sentiment. The survey is conducted bimonthly.