Developing the next generation of finance leaders

Tom Hood, the AICPA’s Executive Vice President for Business Growth and Engagement, joined the network to address ongoing workforce pressures, including declining entry into the accounting profession and rising retirements. While AI is advancing, it will not address talent shortages in the near term, reinforcing the need to strengthen the profession’s pipeline.

To that end, the group discussed the critical need for finance professionals who bring the right mindset, skill set and sense of leadership, combining deep technical expertise with broader skills in analytics and technology and strategic communication. According to Hood, the AICPA is collaborating closely with both employers and academic institutions to accelerate upskilling, deploy more real-world accounting simulations and enhance workplace accounting programs to drive recruiting and retention.

Participants also described recruiting struggles and the need to expose teams to key drivers like data science and external perspectives. To address these concerns, savvy CAOs and controllers are creating skills matrices for their teams, leveraging learning and development opportunities and external speakers to help shift longstanding mindsets and measuring progress through practical outputs.

In addition, Hood also spoke to the rising regulatory complexity around CPA licensing at the state level. For instance, as of January 2026, nearly half of all states have eliminated or revised the once-universal requirement of 150 hours in college credit for those who seek to obtain a CPA license.1 While many see this effort to reform licensing as an impactful effort to stem the talent shortage, others are concerned about the inconsistencies in this growing patchwork of regulations. Calling state licensing issues yet another “structural barrier” to robust recruiting and retention, he noted that the AICPA is working with state authorities across the country to gain clarity and offer guidance.

Board service: raising the bar for readiness

As the discussion moved to the board priorities and service journey, Pat Niemann, EY Americas Center for Board Matters (CBM) Leader, highlighted how boards are intensifying their focus on capital strategy, technology oversight (especially AI and cyber), risk, talent and sustainability. For example, many boards are establishing tech committees to reduce audit committee overload and deepen technology governance. Boards also expect management to demonstrate agility, engage in robust scenario planning and enhance company readiness to proactively navigate uncertainty.

For prospective board candidates, either now or a few years from today, Marla Oates, Managing Director with Russell Reynolds Associates executive search firm and Dan Clifford, EY Americas CBM Board Network Leader, emphasized the importance of personal branding, building relationships with executive recruiters and leveraging nonprofit board service as a pathway to corporate board member roles. Additionally, utilizing your personal network, preparing your board bio and having open conversations with your leadership team about your board ambitions can lead to valuable opportunities that may arise through back-channel discussions.

According to Niemann, board service typically requires around 200 hours per year or roughly 10% of an executive’s time, though this varies by company, board focus and industry. Although it is crucial to weigh your bandwidth for board service, there are potential benefits it can unlock for you while in your current leadership role. For instance, board service can enhance your strategic communication capabilities and enterprise mindset and expand networking opportunities.

AI in finance: a practical approach

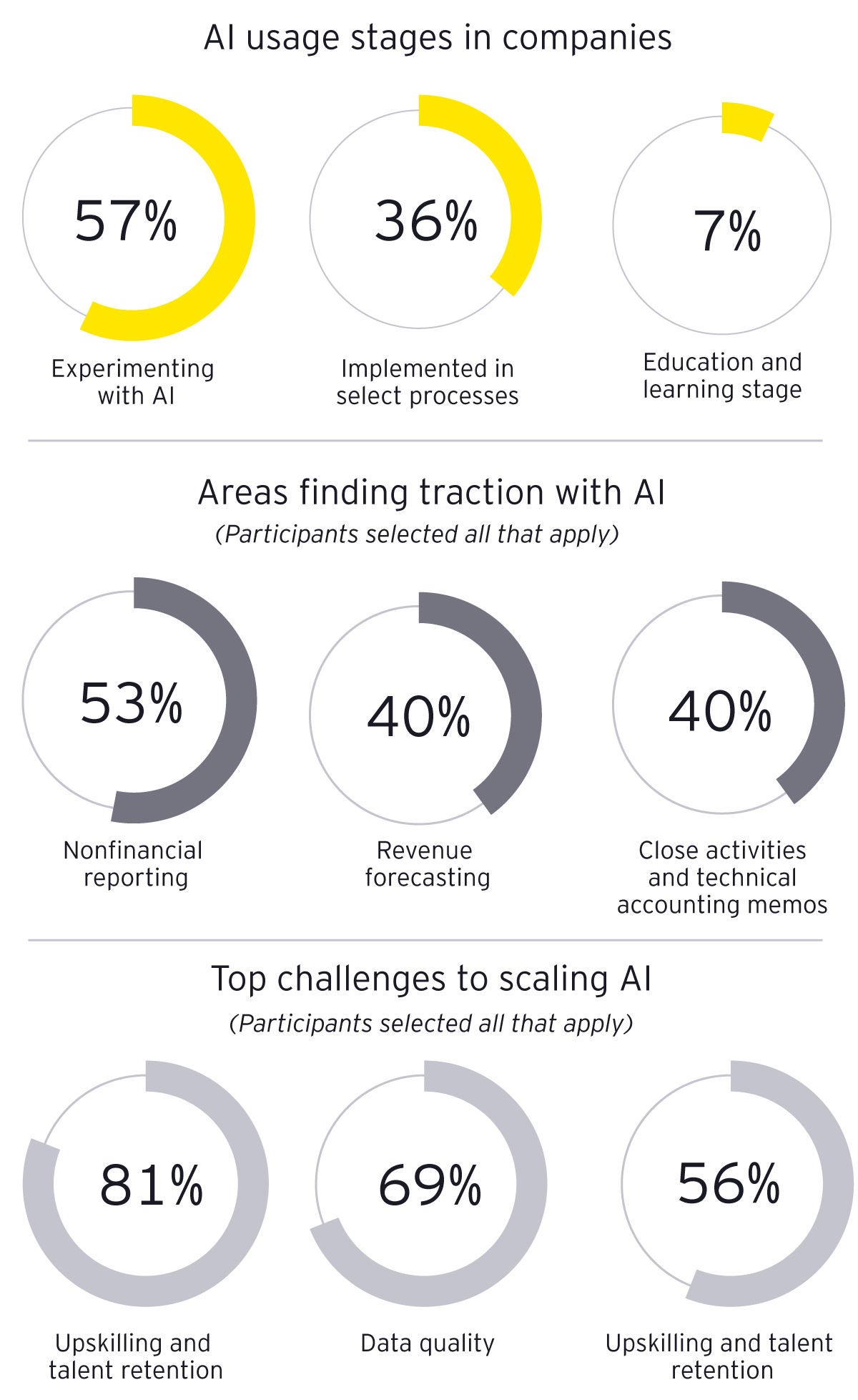

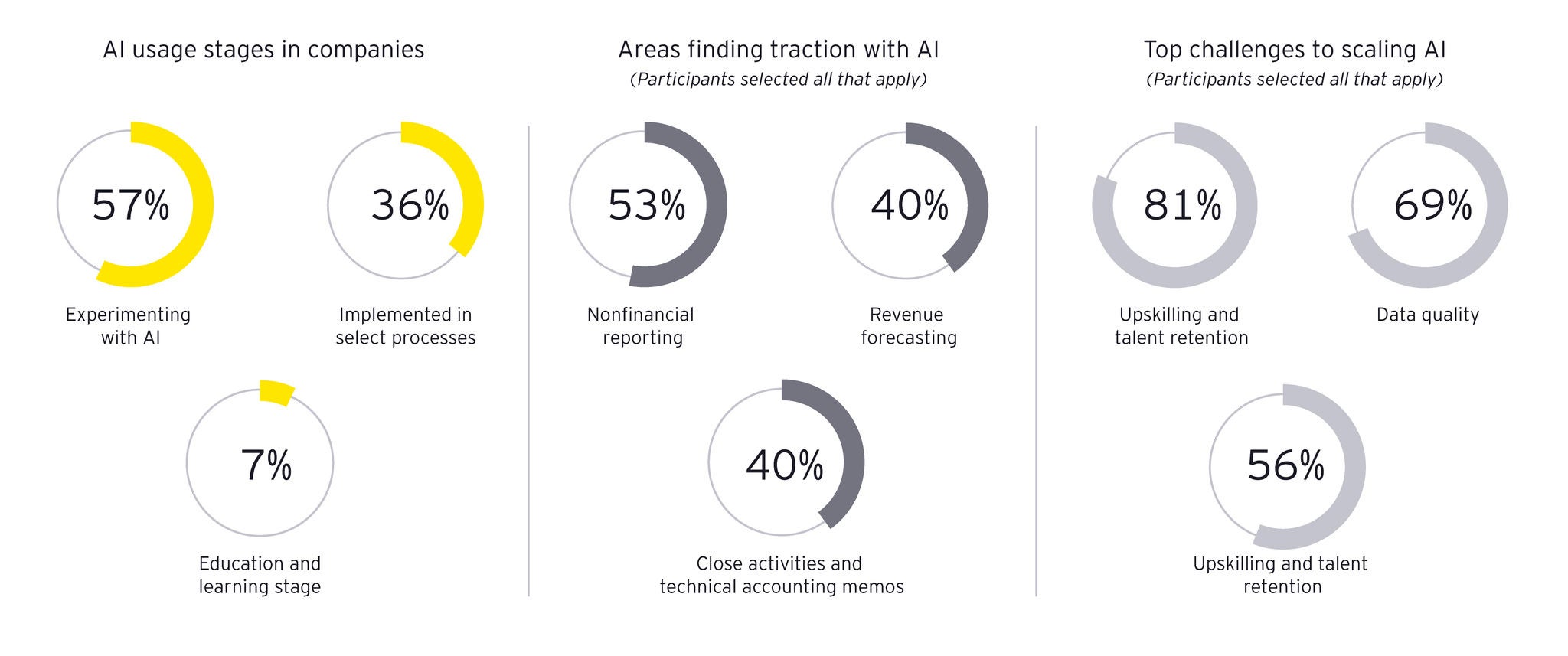

To kick off our discussion on the implications of AI, the group discussed some of the logistical implications of AI, including the need for explicit consent, robust guardrails and human oversight. These principles are especially crucial in sensitive environments like audit and client service. With that in mind, several participants spoke about their organization’s risk tolerance around AI, with some companies embracing the technology and others remaining cautious due to legal and compliance considerations. Participants also agreed that while AI does offer important gains in productivity for audit and finance, it must complement, not replace, professional judgment, keeping a “humans in the loop” focus at the forefront.