Sector highlights

M&A activity over the last three months compared with the same period last year showed significant growth in the deal value across these sectors.

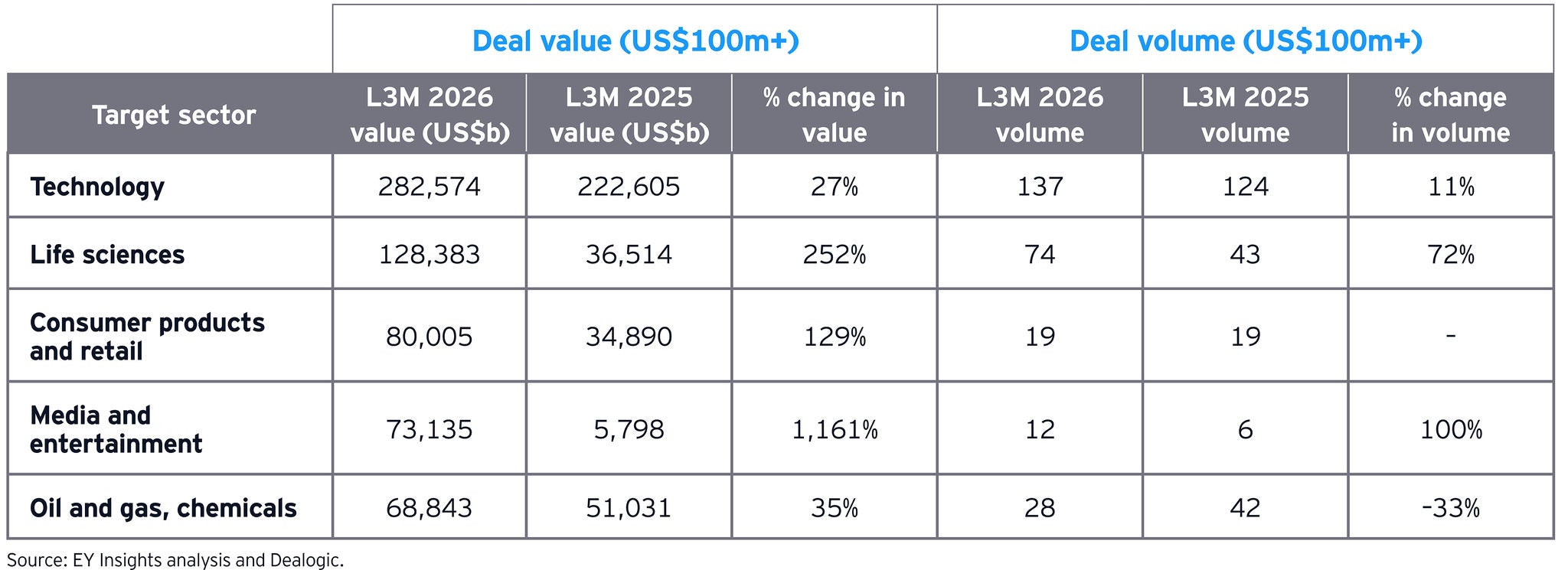

Technology

M&A activity strengthened over the period, with deal values up 27% and volumes rising 11%, reflecting continuous confidence in long-term digital infrastructure investments. Capital concentrated around frontier AI models, compute-intensive platforms and facilitating infrastructure as buyers prioritized securing capacity and scalability. Transactions highlighted a shift toward vertically integrated ecosystems.

Life sciences

M&A accelerated sharply, with deal values up 252% and volumes rising 72%, reflecting a decisive rebound in strategic activity. Buyers focused on scaling differentiated platforms across therapeutics, MedTech and biosimilars, prioritizing assets with clinically de-risked profiles. The momentum was driven by pipeline reinforcement ahead of patent cliffs, access to scalable manufacturing and delivery platforms, and the use of strategic partnerships to improve research and development (R&D) productivity and the speed to market.

Consumer products and retail

The sector saw deal values surge 129%, while volumes remained flat, indicating a concentration of capital into fewer deals that investors felt the most confident about. Activity focused on scale creation, category consolidation and premium brand platforms with strong unit economics. Strategic buyers targeted assets that expand margin accretive adjacencies, strengthen supply chain control and enhance the global distribution reach.

Media and entertainment

The sector registered a significant surge in deal value, increasing by 1,161%, with volumes doubling, reflecting a sharp reacceleration in dealmaking. Activity centered on scale creation in content and rights ownership, portfolio simplification and platforms with recurring cash flows. Buyers targeted assets that unlock valuation re-rating, strengthen the global reach, and improve monetization of high-quality catalogs through technology and data-driven distribution.

Oil, gas and chemicals

M&A activity in the sector became more selective, with deal values up 35% despite a 33% decline in volumes, reflecting a focus on fewer larger consolidation plays. Activity centered on consolidation with the same production region fleet and infrastructure enhancement and selective portfolio pruning. Buyers focused on capital discipline, boosting shareholder returns, and positioning portfolios toward low-cost but high-return assets.

Looking ahead

The US M&A environment is expected to remain active, underpinned by a reopening of deal confidence, continued strategic urgency and ample capital seeking deployment. The global M&A value is estimated to reach ~US$3.8t¹ by the end of 2026, supported by corporate growth strategies and continued private equity exit needs.

However, geopolitical risk remains a defining headwind for 2026, with energy price volatility, trade friction and conflict-related uncertainty complicating underwriting assumptions and extending deal timelines, particularly in energy-intensive, industrial and cross-border transactions.

The EY-Parthenon CEO Outlook Survey reinforces this sentiment, highlighting that geopolitical risk has become the most significant near-term concern for global CEOs, with more than half (56%) identifying it as a key threat to their business. However, CEOs are not retreating from growth initiatives but are tightening their investment discipline, prioritizing profitability and financial resilience. Against this backdrop, 2026 is likely to be shaped by a combination of sustained large cap momentum, selective reopening of mid-market activity, and continued strength in technology (specifically AI, data and cybersecurity) and industrial sectors.