EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

-

Explore the EY Americas Metals & Mining Center of Excellence — your gateway to innovation, expertise & sustainability in the evolving metals & mining sector.

Read more

With global trade dynamics continuing their shift, metals and minerals organizations around the world are entering a period defined by tariff uncertainty and driven by geopolitical tensions, changing policies and the need for an economic recalibration.

Businesses can expect rising costs, continued supply chain disruption and shifting market conditions, demanding that companies remain alert, plan ahead and be ready to jump on change. EY recently hosted a tax webcast with metals and minerals sector leaders from across Canada, the US, Mexico and Chile to discuss the implications of uncertainty and how changing dynamics may impact future landscapes as businesses anticipate what comes next.

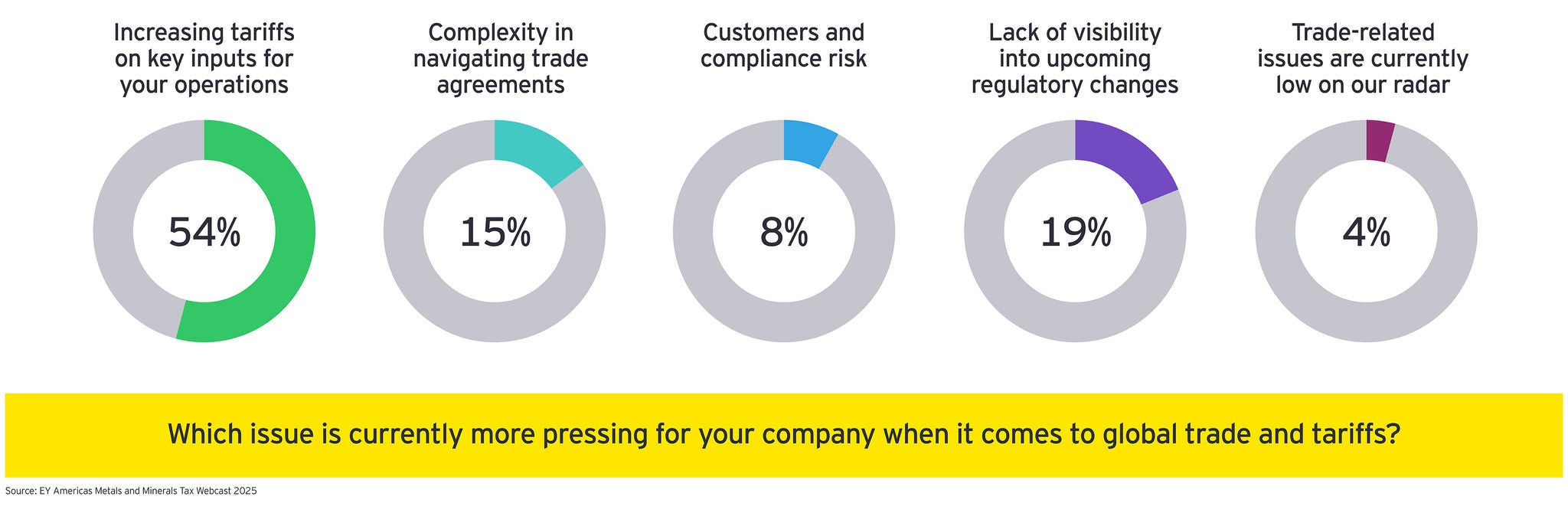

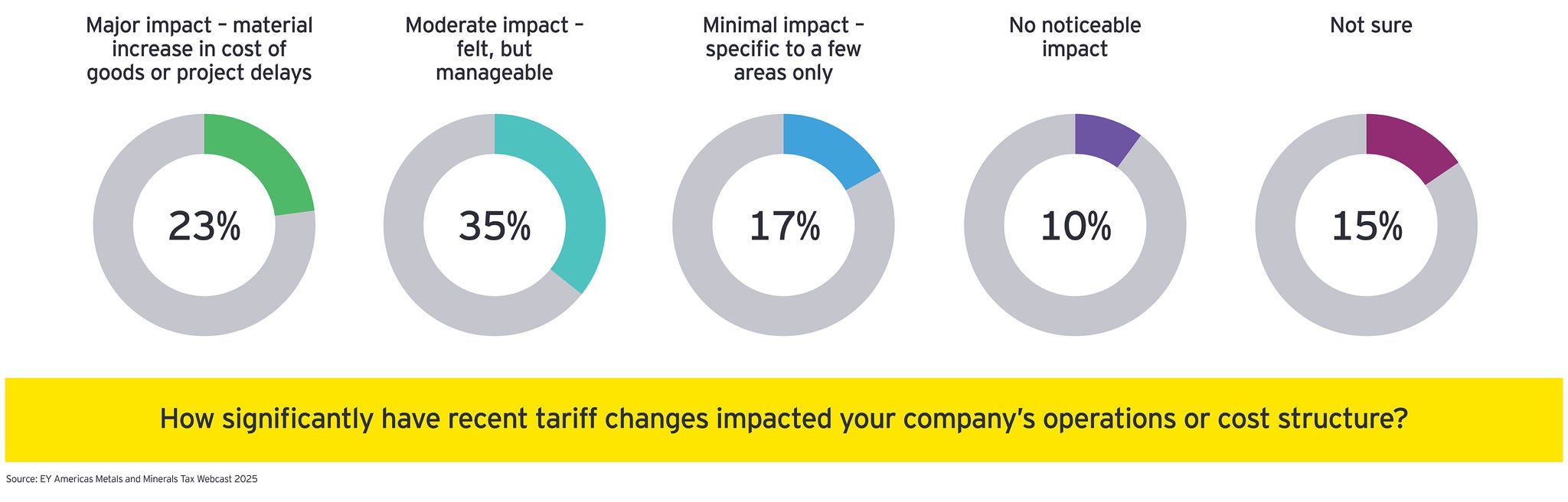

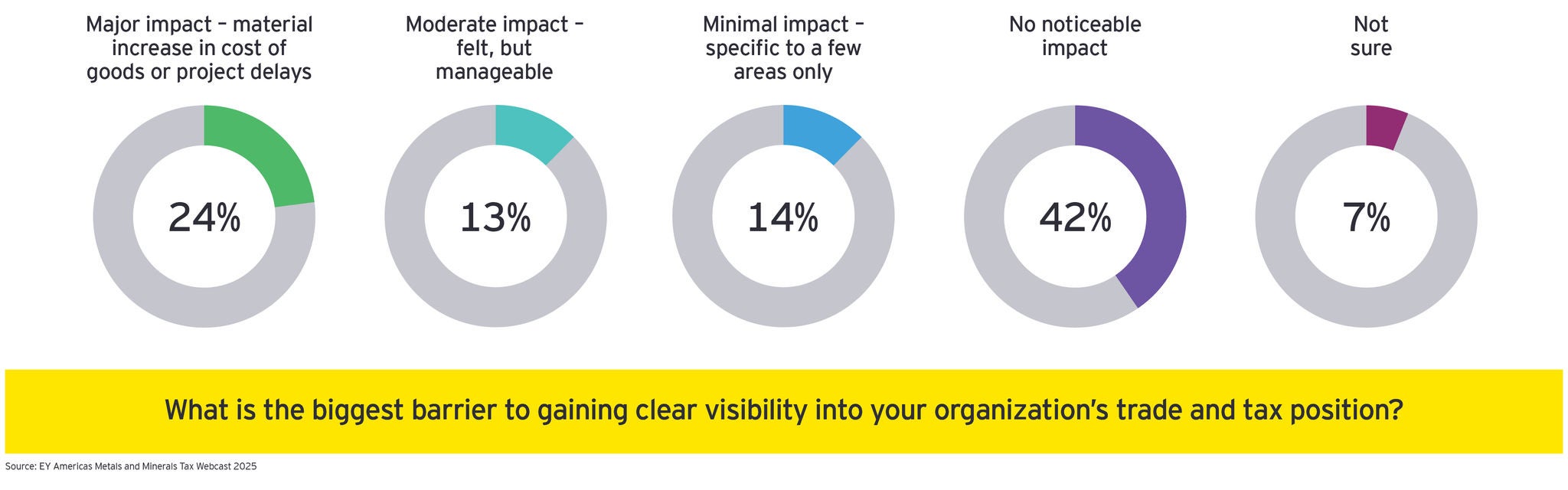

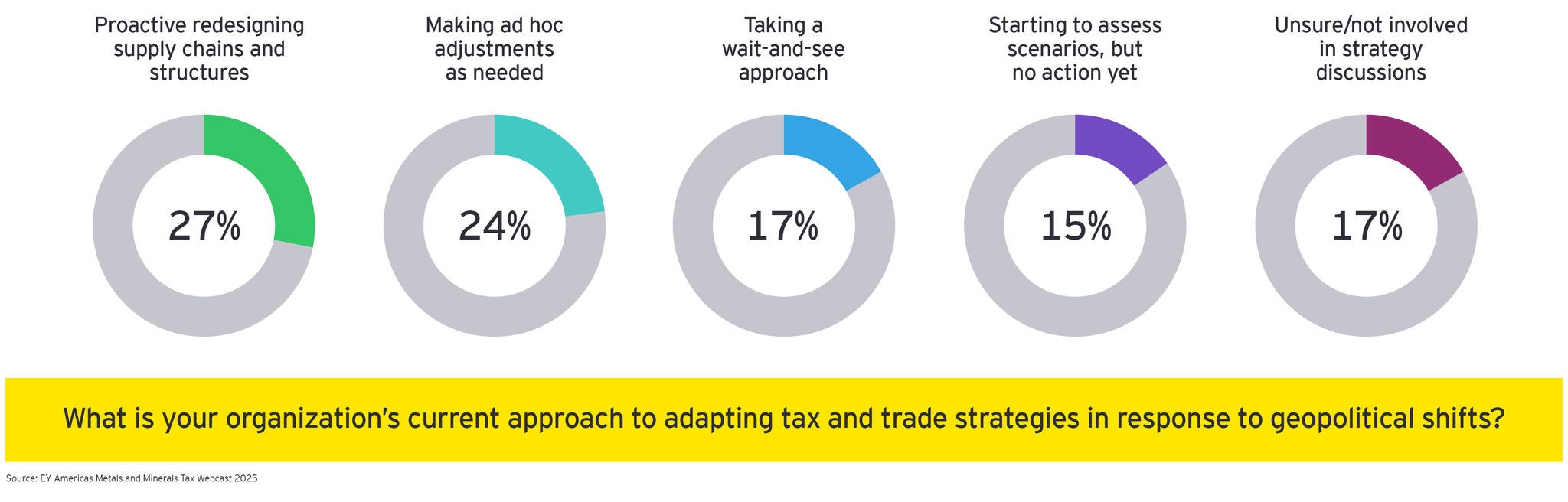

While not entirely unforeseen, the insights shared were compelling. When polled, many — if not most — attendees indicated plans were already underway to respond to volatility and limit risk exposure. But as governments around the world continue to deploy new policies, trade barriers and import taxes, it is clear that navigating continual change will require agility, foresight and a deep understanding of domestic and international trade frameworks.

Exactly where the webcast dialogue began. Moderated by EY Americas Metals and Mining Tax Leader Greg Matlock, the session kicked off a discussion focused on three topics: the current tariff and trade landscape and what EY leaders in the three regions have observed happening in recent months, the latest developments in trade and tariff policies and the potential impact that evolving and contributing factors taking place in these regions could have Americas-wide.