EY helps clients create long-term value for all stakeholders. Enabled by data and technology, our services and solutions provide trust through assurance and help clients transform, grow and operate.

At EY, our purpose is building a better working world. The insights and services we provide help to create long-term value for clients, people and society, and to build trust in the capital markets.

Leaders can rewrite the future of health care value creation with new tools, treatments and operating models that focus on patient outcomes.

In brief

The future of health care value depends on harnessing the power of patients as consumers and achieving better stakeholder outcomes relative to health spending.

Health system collaboration in four areas of innovation, including health care technology, can transform the value of US health care.

Leaders need to build a long-term strategy rooted in tech disruption, novel drug therapies, consumer activation and value-based care (VBC).

The United States is at a turning point, with the future of health care industry “value” weighed down by poor health, rising costs for all stakeholders, negative consumer sentiment and continuing sector disruption.

Those investing in US health care for the long term, and those operating health care systems, need to develop strategies to improve the value in the US health care system. That value can be defined as improvement in health outcomes and experience, divided by spending.

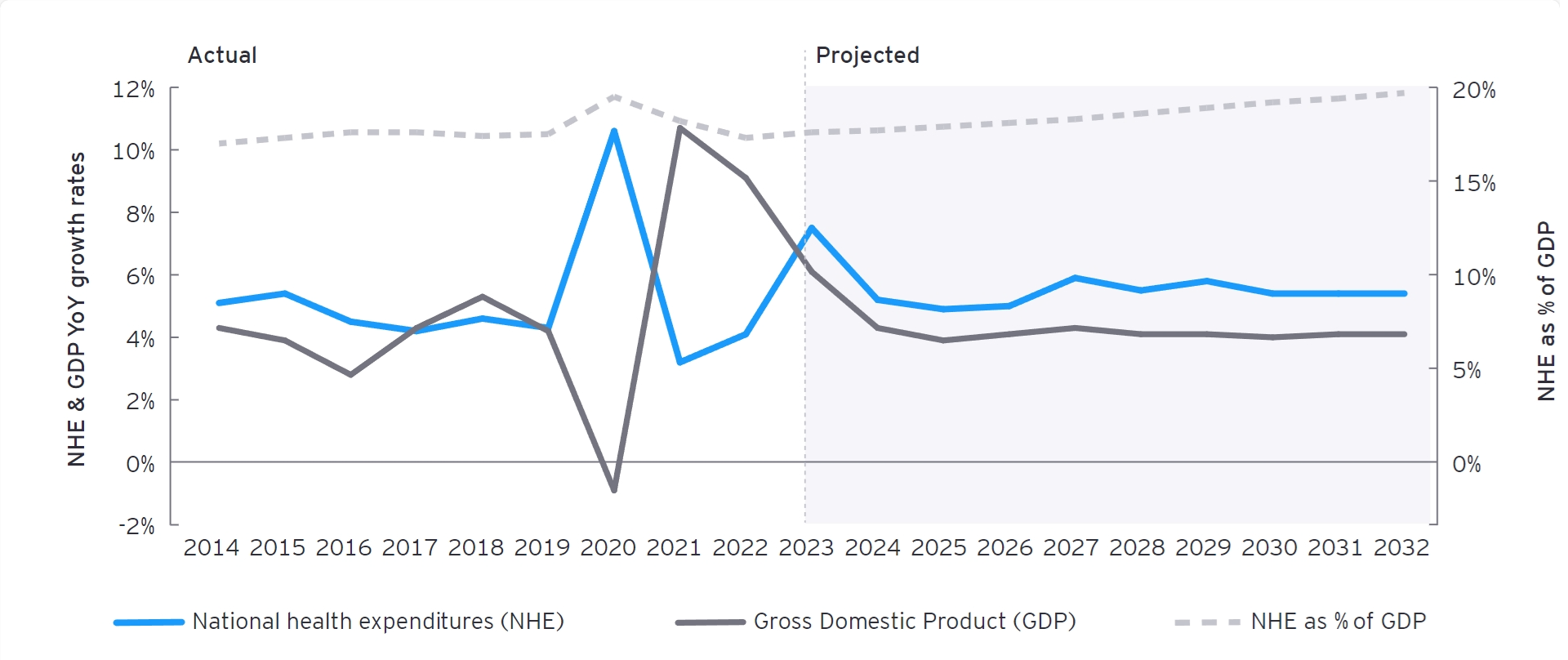

In the US health care ecosystem, improving the health status of individuals and populations has been a challenge despite spending the most per capita, according to a 2024 study by The Commonwealth Fund. National health expenditure (NHE) was 17.6% of GDP1 in 2023 (Figure 1). Yet a recent survey found that people in the US owe at least $220 billion in medical debt, with roughly 6% of adults owing more than $1,000 each.2 An aging population, fragmented purchasing of health services and significant health disparities along racial and socioeconomic lines are driving up NHE. There also are supply side challenges: workforce burnout, labor shortages and unionization are increasing providers’ costs and limiting access to care. Stakeholders across the industry are left asking how to constrain unsustainable cost growth while investing in innovation and disease prevention to create value that is not just financial. To tackle this challenge, leaders need to effect the difficult change needed to transform health care to create a prevention-oriented, proactive, individualized and futuristic health care system.

Figure 1: Health care spending growth projected to outpace GDP growth

Source: Centers for Medicare & Medicaid Services (CMS), Bureau of Economic Analysis (BEA), National Bureau of Economic Research (NBER). Health Affairs.

Figure 1 shows the projected annual growth rate for health care spending outpacing CDP growth between 2023 and 2032, with a dive in health cate spending in 2020, followed by a spike to 2023.

Health care leaders with a long-term outlook need to develop a long-term strategy rooted in four game-changing areas of innovation that could boost the value of their organizations and the US health care industry at large. These areas are technological disruption, novel drug therapies, consumer activation and value-based care (VBC). The value derived from these four areas of innovation is not only the result of measurable efficiencies and greater productivity, but also stems from greater health care access, better consumer experiences and improved clinical outcomes. Although the promise of these innovations is clear, the path to successful transformation is less certain because change will be tough in our existing system.

Health care stakeholders can begin to harness the potential value of these opportunities by asking the right questions:

Technology disruption: How can we harness health care technology, data, automation and digitally connected care to improve both internal processes and care delivery fit for the consumer?

Novel drug therapies: What can we do to foster breakthrough treatments and protocols that can transform condition management and eventually help doctors and patients pre-empt illness?

Consumer activation: Where can we implement better, more personalized experiences for the health care consumer to remove socially determined barriers, unlock self-management and ultimately drive higher value?

VBC: When do we begin the shift from fee-for-service to value-based care payment models to realign incentives that can improve care quality and efficiency and reduce costs?

A long-term strategy developed around these themes can lead to new opportunities to win customers, engage the clinical workforce, partner across the value chain in creative ways and ultimately deliver better value that can be a foundation for growth.

Below we delve deeper into how to think about the challenges and the opportunities surrounding each area of innovation, with real-world examples from the market and EY-Parthenon work.

Innovation 1: How will we harness technology to improve the future of health care?

The current health care system is built on legacy technology stacks, in-person engagement and manual workflows. Technological innovations can automate processes, deliver custom, digitally connected care experiences for patients and mine clinical data to inform efficient treatment. From upstream discovery of novel and enhanced protocols and decision support during diagnosis and treatment to simplification of administrative tasks that drive clinician burn-out, technology can fundamentally improve care outcomes, enable timely patient engagement and scale the health care workforce more effectively. Use cases include summarizing clinical notes, pre-populating responses to patient messages, detecting abnormalities in imaging, providing virtual triage and consultations, identifying novel risk factors in large population health data sets, applying algorithmic treatment rules, aiding drug discovery and monitoring disease progression via connected devices. Despite heath care technology’s clear promise, innovation adoption is uneven, and the impact on NHE is yet unclear.

Questions to help tackle technological disruption:

How can we secure investment for necessary digital infrastructure?

What steps can we take to build clinician trust in AI tools?

How can we work to ensure AI systems are reliable and unbiased?

Are there any opportunities to leverage our clinical experience or data to develop universally useful tools?

The challenges to health care technology adoption include:

Investment requirements: For all actors, implementing novel technologies requires a baseline investment in digital infrastructure, significant computing power, access to large datasets and talented professionals to install and operate complex systems. Securing investment dollars to pay for these technologies is difficult for many health care organizations already operating on slim margins. While administrative tools can be tied to productivity gains or ideal direct cost savings, clinical technology innovations often lack direct reimbursement.3 Providers may struggle to develop a clear business case before implementing these tools — or be forced to pass cost increases on to payers, patients, employers and other purchasers including the government. This can limit adoption speed and value for the system at large.

Trust: Clinician trust in artificial intelligence (AI) technology and concerns over data quality are significant barriers to adoption, as clinicians remain the primary arbiters of care decisions. Beyond the challenge of collecting the fragmented, unstructured and highly sensitive data necessary, significant concerns about accuracy and bias limit practical use. Many clinicians today have not been trained to use new tools and may not understand the flaws and biases inherent to these models. Working to ensure that AI systems are reliable, unbiased and integrated into clinical workflows is essential for widespread acceptance.

Regulation and liability: Novel technologies supporting care delivery lack a clear regulatory framework to define appropriate testing procedures, use cases and human intervention. Stakeholders and patient advocates are calling for more precise regulations to clarify the safety and liability of AI tools in support of adoption decisions. If AI applications are tied to patient care, they are subject to U.S. Food and Drug Administration (FDA) approval. As of mid-2022, the FDA had approved roughly 350 applications for “software-based medical devices.” Without greater oversight and inter agency coordination, few organizations will take the risk to rapidly embrace these technologies.

Solutions to health care technology adoption challenges:

Physician training and engagement: As more products are launched and their impact is studied, stakeholders must share knowledge of new tools’ limits and biases. Medical education and graduate medical training programs must begin to integrate novel care delivery modalities and train providers to evaluate the accuracy of AI-generated outputs. In the long term, training systems must adapt their core curriculum and testing to reflect the rapid advance of technology-enabled health care guidelines. To improve ease of adoption, product developers and practicing clinicians can collaborate to enhance and deploy the most useful and trusted tools, while building a business case based on increased clinician capacity and workforce retention.

Create products and tools: To generate additional returns on new health care technology innovation investment, organizations developing and implementing them must seek opportunities to collaborate with technology developers to reduce costs and create marketable tools and proprietary protocols. Partnering with established technology vendors and pursuing downstream product launches can help secure investment with a clear strategy to diversify revenue. Similarly, a goal to focus on products can help reprioritize the digital transformation necessary to build infrastructure and develop, launch and scale new tools within and across organizations.

Regulatory frameworks: The federal government will play a key role in supporting clinical health care technology adoption by developing appropriate governance and liability frameworks. Current regulations can be advanced and adapted to meet the needs of AI. For example, molecules discovered by AI would still require thorough clinical trials before entering the market. For clinical decision support, AI models could leverage current medical licensing and credentialing procedures to determine the appropriate level of decision-making allowable.

Example: One major health system, seeking to innovate carefully, chose to partner with an external firm accomplished in digital technology, cloud services and cybersecurity. The goal: to dive deeper into data, in a secure way, to tackle the most complex medical problems, provide care wherever the patient might be, drive cures and develop products to diversify revenue. The health system’s researchers, doctors and IT staff will use AI and cloud computing on the external data, permissioned to the external party.

Innovation 2: How will novel drug therapies impact the future of health care?

Therapeutic innovation can help the US health care system progress from remaining in a reactive state focused on managing existing illness, to a proactive stance that pre-empts disease.

Emerging medicinal products such as cell and gene therapies, biotherapeutics and other precision medicines are changing the US health care system. Specialty drugs, such as GLP-1 diabetes drugs, are already driving outsized spending growth, with more therapies to come. The advancement of these potentially curative therapies can transform how we treat many chronic illnesses, provide personalized treatment, significantly increase survival and quality of life and dramatically reduce utilization of costly traditional treatments and facility interventions. Despite the value associated with curative and breakthrough innovations, insurance coverage and access projections remain limited in the short term.4

Questions to consider regarding novel drug therapies:

How can we address the cost effectiveness of advanced therapies?

How can we grow patient and member loyalty to mitigate the impact of insurance switching?

How can we evolve our care model to incorporate breakthrough therapies and complement existing value propositions?

With whom can we collaborate to de-risk access to new therapies?

Challenges to the wider use of drug therapy innovations include:

Cost-effectiveness: Plan sponsors and pharmacy benefit managers (PBMs) may not cover advanced therapies if the treatments fail to drive first-year savings.5 Similarly, purchasers will have concerns about the long-term curative efficacy of new treatments and the role of patient adherence, as both factors affect short- and long-term value realization. Resistance to raising premiums, limited ability to displace other immediate care delivery expenses, inability to manage adherence and failure to continue evidence generation can cause new therapies to be heavily managed through formulary and reimbursement restrictions or delays in patient access.6

Insurance switching: Churn across individual carriers and funding sources (e.g., commercial, Medicare, Medicaid) within patients’ lifetimes can create disincentives for payers to cover high-cost therapies with delayed or long-lived benefits. Those covering the initial cost may not benefit from downstream cost offsets. This challenge can limit access to innovation and lead to disparate coverage approaches such as pushing for significant discounts in early coverage or rationing.7

Comprehensive valuation: Assessments of the value and cost-effectiveness of breakthrough therapies may fail to fully measure potential efficiencies in treatment and societal benefits like productivity growth or reductions in spend on ancillary government programs. Purchasers may understate the benefit of new drugs based on limited value measurement. Similarly, players across the ecosystem may sense risk in adopting therapies that deprioritize or make obsolete traditional care, which has happened as anti-obesity medication reduces the appeal of bariatric surgery.8

Solutions to expand novel drug therapy uses:

Collective funding: Creating an incentive or model for all purchasers to fund and cover breakthrough therapies will be critical to avoiding issues arising from upfront payment, delayed benefits and insurance switching. Ensuring universal access will allow all payers to capture the downstream benefits and unburden the health system at large. Many options exist to remove insurer’s incentives to limit coverage for their independent risk pool, from savings transfers based on patient churn between plans, to alternative insurance vehicles for high-cost therapies, to mandated coverage.

Increasing real-world evidence collection: Transparent and ongoing generation of high-quality evidence can inform fair pricing and coverage decisions. Manufacturers, pharmacies, payers and providers can collaboratively fund studies on the treatment outcomes of new therapies in the field to inform cost and clinical effectiveness evaluations. By performing data analysis on cohorts treated with standard practices and measuring benefits on economic productivity, caregiver quality of life and other societal benefits, health care organizations can better capture the long-term impact of breakthrough therapies on downstream utilization and costs.

Outcomes-based pricing: Continuing to expand the use of value-based reimbursement for novel therapies can accelerate access while controlling risk for funding sources. Amortization and performance-based rebate models can help reduce upfront budget impact and improve treatments’ cost-effectiveness by rewarding longer term outcomes. Manufacturers, pharmacies, PBMs and employers will be incentivized to improve adherence and appropriate use. Similarly, by paying based on the clinical outcome, new pricing models reduce purchaser’s cost-effectiveness concerns.

Example: A new medication contracting company, which aggregates demand across major and independent health insurers, has set about improving affordability and access to costly, cutting-edge therapies. It seeks to help control pricing and provide niche drug evaluation and contracting experience that individual plans may lack. The hope is to accelerate value-based models that get new, curative medicine to people who might die without it, while also bringing greater efficiency to related negotiations and administration.

Our Healthcare Strategy Consulting teams help organizations develop digital, transaction and value strategies to build resilience and drive future growth.

Innovation 3: Why are activated consumers at the heart of the future of health care value?

Enormous opportunity exists to meet consumers’ expectations of convenience in the health care system, enhance patient experiences in seeking and receiving care and, critically, to empower them to choose high-value care.

Value for the consumer and the system arises when patients take preventive medicines, adhere to a care plan and choose lower-cost, higher-quality doctors and facilities. Consumer activation in this setting means empowering the patient to self-manage, and that is more likely when they have had a more positive experience.

Through consumer-focused tactics, the US system can democratize price and quality information, incentivize high value selection and bring experiences with the health care ecosystem in line with modern consumer expectations. In addition, data show deploying patient-centered care can improve the short- and long-term value of care, reduce catastrophic outcomes and minimize the impact of health disparities. Tactically, this can take the form of activation (the ability of patients to manage their own health), coordination and navigation services, and shared decision-making. While both consumer-focused tactics and patient-centered care support efficient decision-making by leveraging existing patient value drivers, the system at scale has been unable to deliver these interventions or measurably enhance consumer experience.

Questions surrounding patient activation:

How can we incentivize high-value choices using cost sharing?

How can we improve the patient-provider relationship by engendering more trust?

How can we choose the right tools to address activation and navigation opportunities efficiently?

What payment incentives can encourage patient self-management?

The challenges to activating consumers are:

Unintended consequences of cost sharing: The rise of high-deductible health plans and the use of value-based insurance designs have demonstrated limited improvement in health care delivery value.10 High-deductible health plans have been shown to cause consumers to reduce their use of health care indiscriminately, leading to lowered preventive care and medication adherence, potentially exposing patients to risk of catastrophic exacerbation of a disease. Similarly, cost sharing designed to induce a focus on prevention has had mixed results with the current primary care delivery system designed to generate downstream service volume.11

Complexity of care decisions: Despite the significant increase in the availability of accurate clinical quality and transparent price data, only a small subset of patients uses this information actively today. Patients, particularly those with chronic conditions or severe diseases, face complex decisions about their care that they may not be equipped to make, even when armed with the right information to support high value selection. First, only 30%-40% of health care dollars are spent on planned services.12 Second, patients may struggle to make decisions because of low health literacy, their diagnosis or accompanying health-related social needs. Finally, physicians, a trusted guide in the care journey, may not have the time or training to engage patients in shared decision-making or provide strong guidance on downstream care cost and quality.

Implementation costs: Providing quality and cost information, effective care coordination and supporting patient activation requires capital and human resource investment by health care entities. Data collection and reporting consume significant organizational resources, while care coordination requires staffing and health care technology investment to provide more seamless patient experiences. Activation approaches rely heavily on clinician assisted coaching and require significant time to help patients acquire the necessary skills to self-manage. Staffing shortages and volume-based reimbursement models create opportunity costs if care delivery organizations prioritize patient activation.

Solutions to help activate consumers:

Payment incentives: Paying for value will enable clinicians to invest time in building trusted relationships and coaching patients to achieve activation and self-management. Quality-based payment can help leading care delivery organizations differentiate themselves and attract well-informed patients. By valuing improvements in health outcomes and reductions in low-value care expenditures, health organizations will create incentives to transform care delivery from transactional provider visits to long-term, trusted relationships. Structured across engagement channels, these incentives can help mitigate disparities in access/resources across populations.

Personalized engagement and tools: Health care organizations can incorporate behavioral analysis of social profiles and willingness to change to focus efforts on patients who are likely to increase activation and health ownership. This will help ensure efficient allocation of resources to those most likely to benefit and subsequently drive high value care decisions. Similarly, health care organizations should focus on increasing their array of resources and tools (e.g., informational resources, community affiliations, remote patient monitoring, digital therapeutics and tools with a strong personalized feedback loop) to match patients’ unique barriers and to help keep healthy behaviors and health status top of mind.

New care models: Organizations can offer more convenient virtual and at-home care to improve patients' experiences and remove barriers to access. Initial returns on hospital-at-home programs show improvements in total cost of care and patient satisfaction, while patient surveys suggest a majority of patients would prefer to schedule virtual care follow up and use at-home urgent care for low-acuity needs.13 Health care systems can drive activation by expanding convenient care options that meet patients where they are while improving navigation and data sharing across settings.

Example: An urgent care chain focused on a specific patient population sought to improve growth and efficiency following its COVID-19 pandemic expansion and the launch of a new segment. Working with the EY-Parthenon team to develop a transformation roadmap, the business identified $40m in opportunities to both enhance revenue and lift margins. The chain invested in marketing technology to better reach its unique patient population and communicate its value proposition for them specifically. Health care technology investment also helped the business improve labor management.

Innovation 4: How do we use value-based care to catalyze the future of health care?

Health care systems that shift from fee-for-service to value-based care models can improve care quality and reduce costs. Value-based payment models compensate providers based on quality and financial outcomes for a population. The goal is to create incentives for better outcomes and reduce costs without encouraging more costly services.14 Performance in two-sided risk models has demonstrated savings, with the Centers for Medicare and Medicaid (CMS) citing more than $2.1b in net savings from the Medicare Shared Savings Program (MSSP) in 2023.15 In addition, studies of value-based payment arrangements in Medicare Advantage indicate improved performance across quality and efficiency metrics, EY-Parthenon analysis shows.

Prioritizing prevention and patient management can build patient trust and reduce case volume growth pressures on providers. Despite the significant potential to improve cost, quality and experience, adoption of downside risk models has only reached roughly 29% of payments across lines of business.16

Questions to ask when setting up VBC:

How can we build a business case to invest in VBC transformation?

What financial strategies can support VBC adoption?

How can we improve data sharing and integration with our partners for VBC?

What standard models and metrics can facilitate VBC adoption?

The challenges to VBC adoption are:

Complexity of implementation: Transitioning from fee-for-service to value-based care involves significant changes in clinical workflows, administrative operations and analytics requirements. Many providers find the process complex, resource-intensive and at odds with their traditional value chain built to capture acute care volume. Similarly, current models may not appropriately adjust payment and measurement thresholds to meet the needs of safety net and rural providers with limited resources.

Financial constraints: Providers are hesitant to assume the investment requirements and financial risk associated with VBC models, particularly if they lack experience with risk management or do not have the necessary infrastructure to support these models. For new adopters, there are upfront investments required to build population health analytics, achieve sufficient primary care scale and coordinate care effectively. All players must traverse a financial J-curve as their performance matures, but even those with significant experience are still subject to patient churn, population variation in utilization and underlying pressures on cost to deliver care.17

Integration and interoperability: Historically adversarial relationships between payers and providers, and a lack of robust data sharing and integration, has limited VBC. Many organizations struggle to define risk-sharing terms with appropriate protections, develop joint operating models that meaningfully improve patient management and execute data sharing agreements that support coordinated care.

Solutions to expand VBC adoption:

Standardization: The government, payers and providers must align on common models and metrics across lines of business to facilitate widespread adoption of VBC. Only through standardization can players reduce the burden of managing multiple alternative payment arrangements and mitigate the complexity of the administrative and clinical implementation. Similarly, by scaling standard models with proven methods of success, the system can proactively minimize performance risk for cautious organizations.

Collaboration: Payers and providers must develop innovative partnerships to share capabilities and capitalize on the unique advantages of verticalization. Payers can play a key role in reducing upfront investment by sharing responsibility for administrative tasks and analytics while providers focus on the monumental task of transforming legacy practice patterns and engaging directly with patients to manage health. Shared accountability through partnerships and joint ventures presents opportunities for organizations once at odds to find financial success competing on value through shared operations.

Patient continuity: While VBC has penetrated furthest in the Medicare markets, commercial and Medicaid adoption have remained low given the limitations of preventive care in driving in-year savings. Improving customer experience, deepening trusted relationships with managing clinicians and maintaining longitudinal responsibility for patients’ medical costs can improve the return on investment (ROI) in VBC capabilities. These goals can be mutually reinforcing as success in VBC can enable superior product pricing and therefore greater market share growth and retention.

Example: The EY-Parthenon team helped a large regional health system redesign existing payer-provider risk sharing agreements and align its operations to improve the partnership’s financial performance. By re-evaluating existing data sharing agreements, the partnership enhanced its ability to identify and manage high-risk patients as well as affiliated providers. The EY-Parthenon team helped design a risk-bearing clinical model and charted the course for implementation to redirect profitability and performance.

The future of health care in the US — improved health outcomes, lower costs and more positive consumer sentiment — will depend on how organizations address four key areas of innovation impacting “value.” Technological innovations can improve care outcomes and efficiency, but adoption is hindered by investment, trust and regulatory issues. Novel drug therapies offer potential cures but face cost-effectiveness and insurance challenges. Patient activation can enhance care experiences, but cost-sharing and decision complexity are barriers. VBC payment models can drive quality improvement and cost reduction, but implementation complexity and financial constraints limit adoption. Although challenges to progress are many, better questions are likely to help leading organizations collaborate within the health care ecosystem and ultimately improve value.

Health care leaders need to gear up for growth through health care M&A, investment, divestment and transformation as the sector and market evolve rapidly.