EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

UK Internal Controls

Under UK Government’s proposals, a reform of internal controls is happening. Here, we outline the implications for directors and companies.

Proposed changes to the UK Corporate Governance Code

The Financial Reporting Council has proposed revisions to the Code. What would they mean for you?

Read our summary (PDF).

The challenge for companies

Pressure is on companies to improve their internal controls and corporate governance from a range of stakeholders. Such companies face challenges from:

- UK Government: Weak internal controls and risk management were key factors in recent well-publicised company failures. This drove the Government to publish a consultation paper on ‘Restoring trust in audit and corporate governance.’

- Regulators: At a minimum, the Financial Reporting Council (FRC) intends to ‘raise the bar’ on internal controls, with revisions to the Corporate Governance Code.

- Directors: They may be required to certify the design and operating effectiveness of the internal controls framework.

- Investors: Many investors now view poor controls as a top risk when acquiring, partnering or investing.

Directors of most UK corporates (except US-listed companies) have never had to meet these pressures or formally attest to the effectiveness of their financial reporting controls. The questions they now need to ask are:

- What will be the level of assurance needed?

- How can we give the required assurance — effectively and efficiently?

- What are the resources and capabilities that we need?

- How do we bring people on the journey whilst making sure that they still focus on their roles and deliver value for stakeholders?

The outcomes and benefits of improving your internal controls

The reform presents an opportunity for businesses to enhance trust and confidence amongst a company’s investors and stakeholders in the longer term.

Many organisations have already moved quickly to enhance their internal controls and found value for their organisation from:

- Greater confidence: Directors and investors can be confident in controls compliance, including actions taken to prevent and detect material fraud.

- Improved efficiency: Organisations can achieve savings and efficiencies from standardising, automating, and enhancing their controls environment.

- Strengthen transformation: Organisations can maximise the success of any finance transformations and enterprise resource planning (ERP) implementations by simultaneously improving their controls.

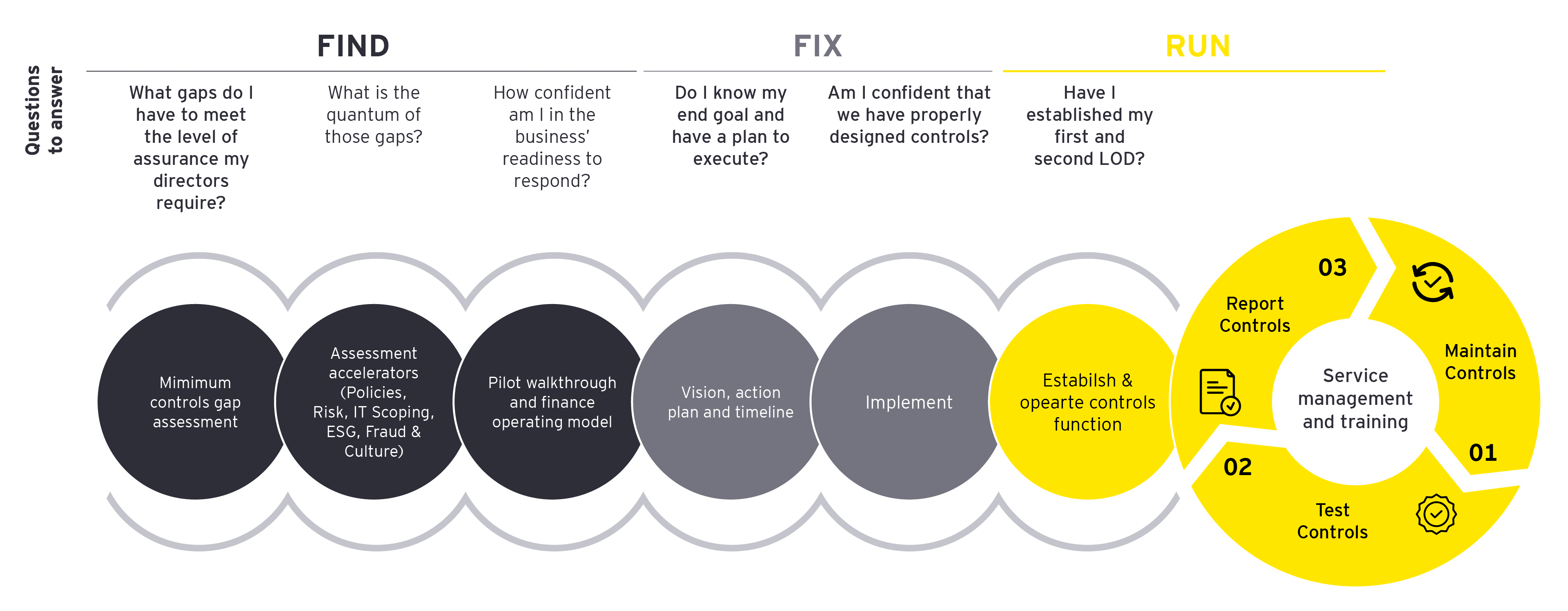

Your corporate reform journey

Organisations should look to smart and efficient ways of complying with possible new internal controls reforms. We recommend companies employ a three-step approach to meeting the requirements, whilst considering longer-term opportunities to transform their control environment.

There are several key considerations to start the journey to implementation, such as:

Our latest thinking

How to get on track with material controls declaration

Discover how listed companies are preparing for risk management and internal control changes of the UK Corporate Governance Code. Read more.

How enhanced financial controls lead to smarter decision-making

Our case study shows how a FTSE insurer strengthened their internal controls to mitigate risk, drive innovation and instil confidence in decision-making.

What NEDs should be asking about upcoming corporate reform

Read more about what NEDs should be asking about the upcoming corporate reform changes.

How internal controls could drive finance function transformation

Find out how to use internal controls as a driver for wider finance function transformation. Read more.

Direct to your inbox

Stay up to date with the latest news and insight

How EY can help

-

EY UK Corporate Governance team offers guidance and thought leadership on governance issues to assist clients and contribute to broader discussions.

Read more -

EY audit team can help you uncover controls that are not effectively designed and provide improvement recommendations. Learn more.

Read more -

Our skilled teams, operational efficiencies enabled by innovative technology and flexible global delivery service centers can help you manage financial crime risk in a cost-effective, sustainable way.

Read more -

Our Leadership and Culture services help organizations create and maintain thriving, inclusive workplaces where people can perform at their best.

Read more