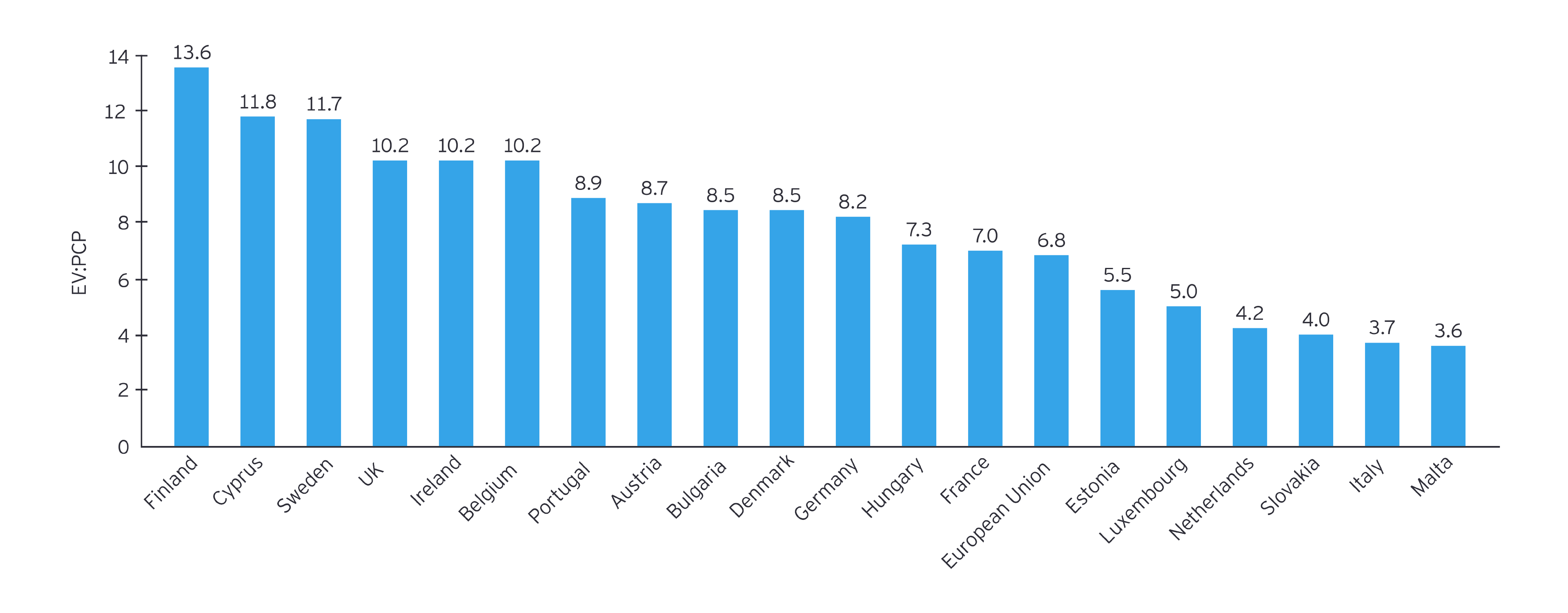

Alongside questions on the scale of public infrastructure, there is uncertainty surrounding future consumer behaviors and how this may guide the type of infrastructure required. We have just been through the first stage in the EV market evolution, with early adopters making up a small proportion of the vehicle market. We are now transitioning to the second stage, characterized by exponential growth in the sale of EVs and charge points. The final phase of market maturation, which we expect to arrive at well beyond 2035, will see high levels of consolidation of charging infrastructure players and commoditization of charging services.

Evidence suggests the market is unlikely to mature in this decade, though when we do enter the maturing market phase, price will play a more significant role in purchasing decisions. It is still unclear how the importance of other criteria will evolve in this nascent market and how this might vary by customer segment.

Changing consumer priorities and the shift from battery rant anxiety to charge anxiety, will also have an impact on the frequency, speed and location of charges. For example, EY-Parthenon Knowledge predicts ~220,000 public charge points in France by 2030. However, as adoption increases and consumer behaviors become more established, we see potential upside for rapid and destination charging.

France charge points split by private vs. public (#) and France public charge points split by destination vs. other public (#)